The start of a new financial year can be the right time to review your finances and put important money matters in order.

Adhil Shetty, CEO, Bankbazaar.com told ET Wealth Online the start of a financial year is when the basics need to be put in place, because these decisions tend to shape how the rest of the year plays out.

“When core financial decisions are addressed upfront, whether it is choosing the right tax regime, ensuring adequate term and health insurance, or setting up long-term investments, the rest of the year tends to unfold with fewer reactive adjustments. This early clarity improves cash flow visibility and reduces the need for last-minute corrections,” says Shetty.

Here are some of the key financial tasks you should consider completing early in the new financial year (FY 26-27) to stay financially organised and prepared.

Also read: New income tax rules from April 1, 2026: From HRA relief to new ITR deadlines, key changes explained

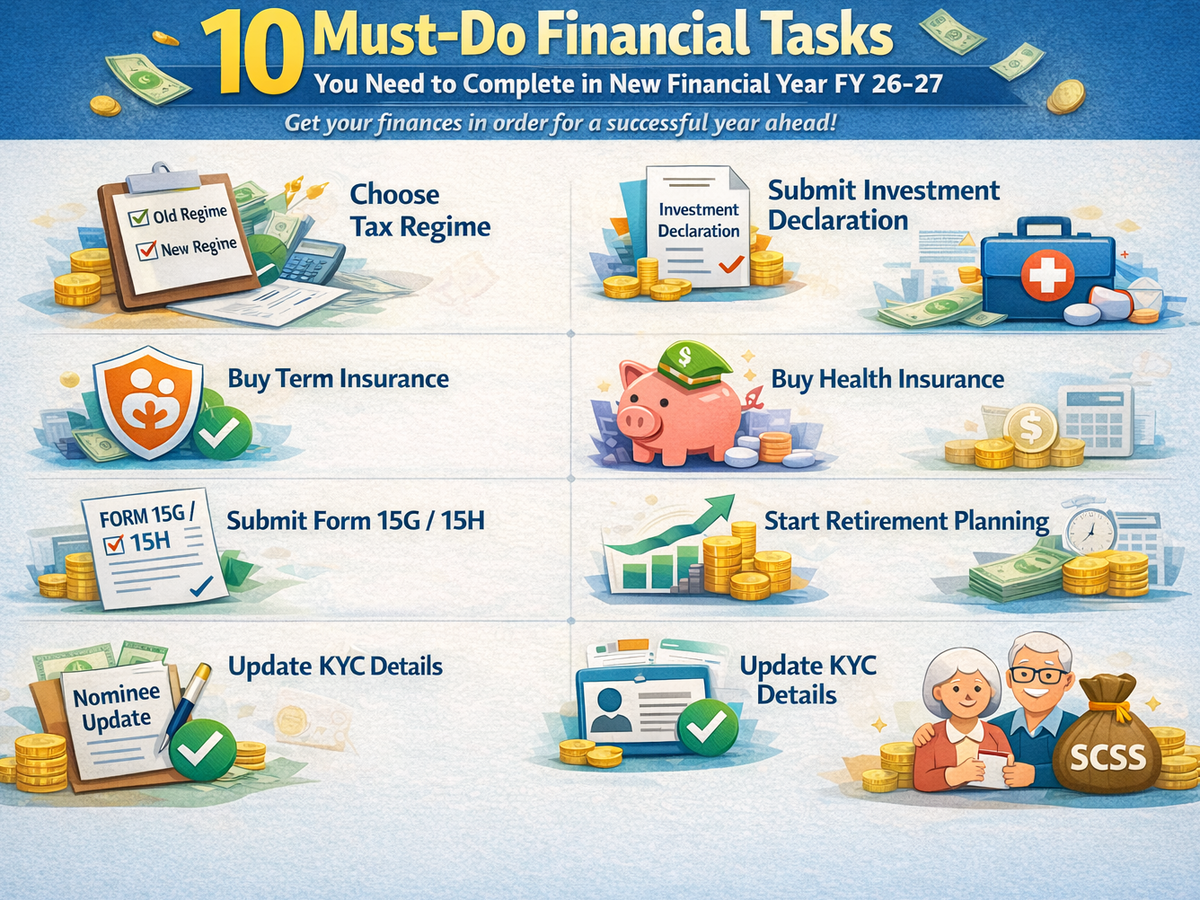

At the start of the financial year 26-27, inform your employer whether you want to opt for the old or the new tax regime. This helps the payroll team calculate the correct TDS from your salary.

If you don’t declare, many employers may pick the new tax regime as a default option for you.2. Investment declaration in old or new tax regimeIf you plan to claim income tax deductions, submit your investment declaration form online or offline early in the financial year.

If you follow the old tax regime, your declaration may include details of investments like Public Provident Fund (PPF), Equity Linked Savings Scheme (ELSS), insurance premiums, home loan principal and interest payments, etc.

If you follow the new tax regime, you can take tax benefit on the let-out property.

Timely declaration ensures lower monthly TDS and smoother tax planning.

A term insurance policy protects your family financially if something happens to you. Buying it early in life usually means lower premiums and better coverage options.

If you already have a term insurance plan, make sure you have adequate coverage. If the coverage is not adequate, you may increase it, or you may also buy a separate plan for it.

4. Buy health insuranceHealth insurance is essential to manage rising medical costs. It also helps you avoid financial stress during medical emergencies. So, don’t delay and buy it soon in the beginning of the new financial year.

If you already have an existing health insurance plan, make sure that you have adequate coverage of it. If it is not adequate, try to increase it, or buy a separate policy. If you have a corporate plan provided by your employer, you still need to buy a separate plan as the corporate plan can end once you leave your job.

5. Submit Form 15G, 15H for new financial yearFor individuals whose income is below the taxable limit, the submission of Form 15G or 15H to avoid TDS on the interest income is necessary.

These forms need to be submitted every financial year to banks or financial institutions.

Senior citizens usually use Form 15H, while others eligible use Form 15G.

The beginning of the financial year is a good time to plan your retirement. Start setting aside money regularly to invest in long-term investment options. An early start in your life can help you achieve your retirement goals with ease.7. Start STP transfer if your retirement is a few years awayRebalancing your portfolio is necessary if your retirement is a few years away. A good initiative can be to shift the equity portion of your portfolio to hybrid, fixed income or debt investments. If your investments are in equity mutual funds, you can shift them to hybrid or debt funds through a Systematic Transfer Plan (STP).8. KYC updateTo ensure your details are correct in your investments or bank accounts, ensure your Electronic KYC (e-KYC) details are updated with the correct address and the ID proof.9. Update nomination detailsUpdate nominee details in your investments, insurance policies, bank accounts, etc, right away if your family’s circumstances have changed. Verify that the nominee’s information is accurately entered into your investments and bank accounts.

10. Invest in senior citizen schemesIf you are turning 60 years of old, you can invest in schemes specifically designed for senior citizens. Senior citizens enjoy higher interest rates on fixed deposit schemes offered by different banks and small finance banks.

They can also invest in Senior Citizen Savings Scheme (SCSS) that offers an interest rate of 8.2%. Senior citizens enjoy a higher exemption limit of Rs 1 lakh for TDS on the FD interest income.