Never miss an important update on your stock portfolio and cut through the noise. Over 7 million investors trust Simply Wall St to stay informed where it matters for FREE.

Micron Technology (NasdaqGS:MU) is acquiring Powerchip Semiconductor Manufacturing Co.’s Taichung P5 site in Taiwan to expand DRAM capacity.

The company is launching new cleanroom projects at the site and across Taiwan to support advanced DRAM and high bandwidth memory production.

These moves are aimed at addressing AI driven demand for memory and current supply constraints in next generation products.

Micron, a major producer of DRAM, NAND, and high bandwidth memory used in data centers and AI infrastructure, is tying its manufacturing footprint more tightly to long term AI demand. The acquisition of a large, existing site in Taichung, paired with new cleanroom projects, places more of Micron’s physical capacity buildout in Taiwan alongside its U.S. and broader Asia presence.

For investors, this kind of physical expansion is less about quarter to quarter numbers and more about where Micron wants to sit in the AI hardware supply chain. The scale of new cleanroom investments and DRAM focused buildout could influence the company’s capital intensity, product mix, and exposure to AI memory cycles as those facilities come online.

Stay updated on the most important news stories for Micron Technology by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Micron Technology.

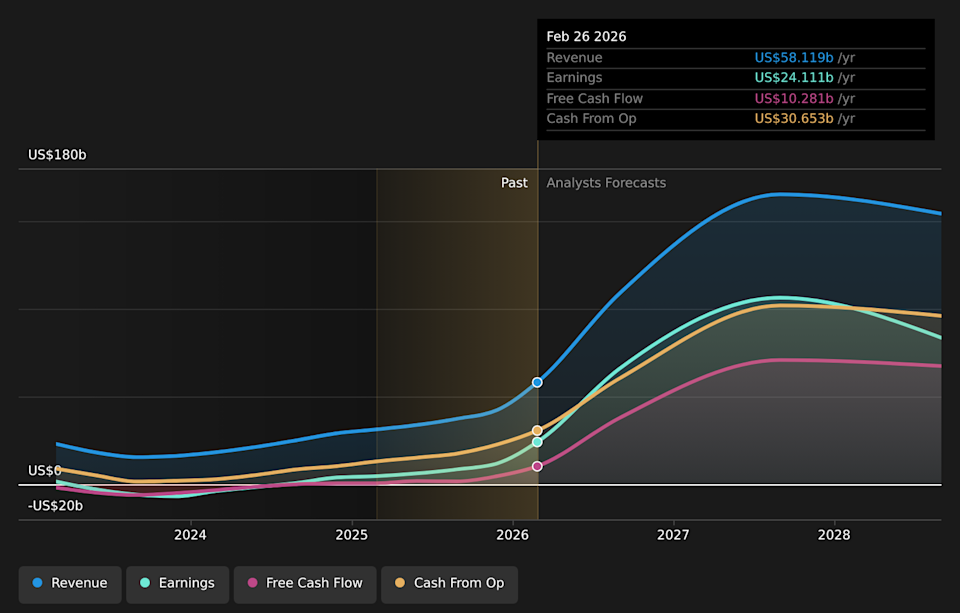

NasdaqGS:MU Earnings & Revenue Growth as at Apr 2026

NasdaqGS:MU Earnings & Revenue Growth as at Apr 2026

We’ve flagged 2 risks for Micron Technology. See which could impact your investment.

Micron’s purchase of Powerchip’s Taichung P5 site, alongside new cleanroom projects, pushes its AI-focused DRAM capacity deeper into Taiwan, where rivals like Samsung and SK Hynix also have large memory operations. For you as an investor, this is about Micron trying to secure enough 300mm wafer and cleanroom space to support products such as high-bandwidth memory and advanced data-center DRAM that are tied directly to AI servers. The retrofit schedule, with shipments expected from fiscal 2028, means current AI strength is being used to justify capacity that will matter years from now, not just for the next couple of quarters. At the same time, Micron is already committing more than US$25b of capex in fiscal 2026 and retiring long-dated debt, so adding another large physical site tightens the link between its future returns and how well AI memory demand holds up once this new capacity is ready.

The P5 acquisition and Taiwan cleanroom plans support the existing narrative that Micron is leaning into AI and data-center demand by prioritizing high value DRAM and HBM capacity, backed by long-term customer agreements.

This news also sharpens one of the narrative’s concerns, which is heavy, ongoing investment in fabs and advanced nodes that could pressure free cash flow if memory pricing or utilization soften.

The narrative focuses heavily on demand and competition but does not fully incorporate site specific concentration in Taiwan alongside large US projects, which introduces location and execution risk tied to these particular campuses.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Micron Technology to help decide what it’s worth to you.

⚠️ Large, long lead time DRAM projects in Taiwan and Tongluo could come online into a cooler memory cycle, increasing the risk of oversupply or weaker pricing versus expectations.

⚠️ Concentrating more AI-centric capacity in Taiwan adds geopolitical and operational risk on top of existing exposure, especially with Samsung and SK Hynix competing aggressively in similar product tiers.

🎁 Securing an existing P5 site and adding cleanroom space gives Micron a clearer path to scale DRAM and HBM volumes for AI workloads at the point where current sold out capacity and multi year contracts indicate tight supply.

🎁 Aligning future wafer and cleanroom capacity with long term AI demand, while also retiring higher coupon debt, can support Micron’s goal of pairing growth in premium memory products with a balance sheet that can handle industry cycles.

From here, watch how Micron sequences spending on the P5 retrofit and Tongluo expansion against its US and Japan projects, and whether management links that capex directly to additional long term HBM and DRAM contracts. Monitor commentary on when these Taiwan facilities are expected to reach meaningful output and how that timing lines up with supply plans from Samsung and SK Hynix. It is also worth tracking any updates on Micron’s total capex envelope beyond fiscal 2026, because that will show whether the company is leaning further into AI related builds or pacing investment to protect free cash flow.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Micron Technology, head to the community page for Micron Technology to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include MU.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com