Canada’s inflation ticked a bit higher in October, with the Consumer Price Index (CPI) rising 2.2% YoY, slightly above what markets expected, after a 2.4% increase in September. On a monthly basis, prices were up 0.2%, as forecast.

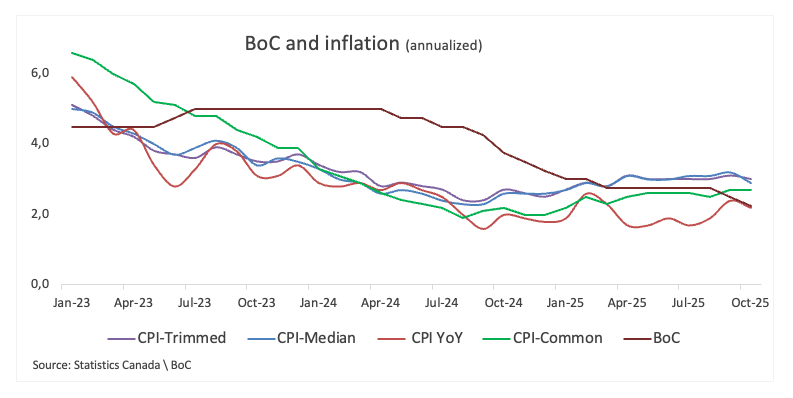

The Bank of Canada’s (BoC) preferred core measure, which strips out the more volatile items like food and energy, rose 2.9% over the past year and gained 0.6% compared to the prior month.

Looking at the BoC’s other key inflation gauges, Common CPI came in at 2.7%, Trimmed CPI at 3.0%, and Median CPI at 2.9%. Together, they show that underlying price pressures are still fairly sticky.

According to the press release: “The all-items CPI decelerated largely due to gasoline prices, which fell at a faster pace year over year in October (-9.4%) compared with September (-4.1%). Excluding gasoline, the CPI rose 2.6% in October, matching the increase in September. Slower growth in grocery prices further contributed to the deceleration in the CPI in October, which was moderated by higher prices for cellular phone plans.”

Market reaction

The Canadian Dollar (CAD) loses impulse on Monday, prompting USD/CAD to trade with decent gains around the 1.4030-1.4040 band in the wake of the release of Canadian inflation data.

Canadian Dollar Price Today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the strongest against the Australian Dollar.

USDEURGBPJPYCADAUDNZDCHFUSD0.22%-0.11%0.20%0.07%0.38%0.25%0.21%EUR-0.22%-0.34%0.00%-0.15%0.15%0.03%-0.01%GBP0.11%0.34%0.31%0.18%0.49%0.36%0.32%JPY-0.20%0.00%-0.31%-0.14%0.17%0.04%0.00%CAD-0.07%0.15%-0.18%0.14%0.31%0.18%0.15%AUD-0.38%-0.15%-0.49%-0.17%-0.31%-0.12%-0.17%NZD-0.25%-0.03%-0.36%-0.04%-0.18%0.12%-0.04%CHF-0.21%0.01%-0.32%0.00%-0.15%0.17%0.04%

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Canadian Dollar from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent CAD (base)/USD (quote).

This section below was published as a preview of the Canadian inflation report for October at 09:00 GMT.

Canadian inflation is expected to edge lower in October.The core CPI is still seen well above the BoC’s 2% goal.The Canadian Dollar managed to regain some composure this month.

All eyes will be on Monday’s inflation report, as Statistics Canada releases October’s CPI figures. The data will give the Bank of Canada (BoC) a much-needed update on price pressures ahead of its December 10 meeting, where policymakers are widely expected to keep rates steady at 2.25%.

Economists see headline inflation rising 2.1% YoY in October, nearing the BoC’s target after September’s 2.4% reading. On a monthly basis, prices are expected to edge up 0.2%. The bank will also closely monitor its preferred core measure, which experienced a 2.8% YoY increase in September, following a 2.6% increase in August.

Analysts remain uneasy after last month’s inflation pickup, and the risk of US tariffs feeding into domestic prices is adding another layer of uncertainty. For now, both markets and the Bank of Canada appear poised to exercise caution.

What can we expect from Canada’s inflation rate?

The Bank of Canada cut its benchmark rate by 25 bps to 2.25% in October, a move that largely matched what markets were expecting.

At that meeting, Governor Tiff Macklem struck a cautiously optimistic tone. He said policy is now providing “some stimulus” as the economy loses momentum, and although consumption is likely to cool, he stressed that one soft data point wouldn’t be enough to shift the bank’s broader view. Still, he didn’t completely dismiss the possibility of two negative quarters. He also warned that equity valuations look “stretched”, hinting at growing unease beneath the surface.

Senior Deputy Governor Carolyn Rogers echoed that vigilance, noting the Canadian Dollar is still doing its job as a shock absorber and pointing to widening regional contrasts in the housing market. Both she and Macklem acknowledged that financial-stability risks have become part of the conversation again.

For markets, Monday’s headline CPI number will be the first thing they latch onto. But inside the BoC, the spotlight will be on the details, especially the Trimmed, Median, and Common core measures. The first two remain stuck above 3%, a level that continues to worry policymakers, while the Common measure has drifted higher as well, still comfortably above the bank’s target.

When is the Canada CPI data due, and how could it affect USD/CAD?

Markets will be dialled in on Monday at 13:30 GMT, when Statistics Canada releases October’s inflation numbers. Traders are on edge about the possibility that price pressures remain stubborn, keeping the uptrend firmly intact.

A hotter-than-expected print would fuel worries that tariff-driven costs are finally making their way to consumers. That kind of signal would likely push the Bank of Canada into a more cautious stance, at least in the near term. It could also give the Canadian Dollar (CAD) a bit of short-term support, as investors brace for a policy path that hinges increasingly on how trade tensions evolve.

Pablo Piovano, Senior Analyst at FXStreet, notes that the Canadian Dollar has managed to appreciate since its lows earlier this month, prompting USD/CAD to slip back toward the key 1.4000 region. Meanwhile, further gains appear likely while above the key 200-day SMA near 1.3930.

Piovano indicates that the resurgence of a bullish tone could motivate spot to confront the November ceiling at 1.4140 (November 5), ahead of the April top at 1.4414 (April 1).

On the flip side, Piovano points out that a key support lines up at the 200-day SMA at 1.3929, prior to the October floor at 1.3887 (October 29). The loss of this region could spark a potential move toward the September valley at 1.3726 (September 17), seconded by the July trough at 1.3556 (July 3).

“In addition, momentum indicators remain constructive: the Relative Strength Index (RSI) lingers near the 53 level, while the Average Directional Index (ADX) eases toward 25, suggesting a still firm trend,” he says.

(This story has been updated on November 17 at 10:46 GMT due to a last-minute change in the consensus to say that headline inflation is expected to rise 2.1% YoY and to edge up 0.2% MoM in October, not 2.3% and 0.1% respectively, as previously estimated.)

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it.

Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.