On Monday, the markets were trying to work out what the war meant for shares, energy prices and the world economy. By Tuesday it was clear that they did not like what they were seeing.

Gas and oil prices, which were already on the rise, headed further into territory which – if sustained – indicate a nasty hit to prices and inflation.

Shares, having not done too much on Monday, when the US S&P 500 even finished higher, have now turned significantly downwards, with European markets seeing the biggest falls since the aftermath of US president Donald Trump’s “Liberation Day” announcement on tariffs last April.

Much now depends not only on how the war spreads, but also on how long it lasts. If the war is over in a few weeks, then the wider economic impact will be limited. But if it drags on, then the economic damage will be a lot more serious. If, for example, oil and liquefied natural gas (LNG) could not move through the Strait of Hormuz for a prolonged period – or there is serious damage to oil and gas infrastructure in the Gulf region – then the impact on international inflation and growth would be significant.

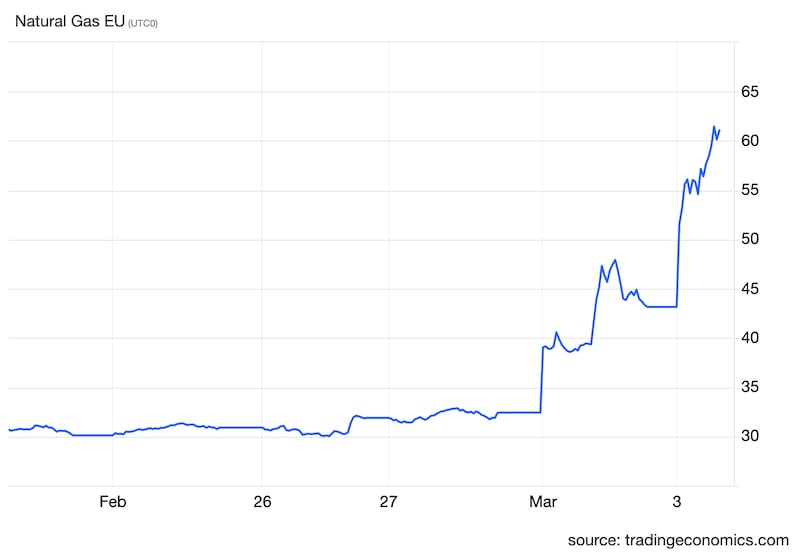

Gas EUR/MWh

EUR/MWh

Gas prices are one of the most vital indicators to watch. LNG from the Gulf tends to head east to countries such as China and India, with Italy the largest European buyer. However, world shortages increase bidding for what is available and lead to a general increase in prices. And as a key fuel in generating electricity and fuelling businesses, gas has a significant economic impact – its price rise was responsible, for example, for some of the inflationary surge following the Russian invasion of Ukraine. Then European prices peaked briefly at more than $300 per megawatt hour, but for the second half of 2022 generally remained well over $100.

Now warning signs are flashing again as prices have risen by 85 per cent-plus over the past couple of days and on Tuesday midmorning were around $60 per megawatt hour. An Iranian attack on the Qatari Ras Laffan production facility on Monday – leading to a halt in output – together with the inability to ship LNG through the Strait of Hormuz, has rattled nerves. Qatar is the leading supplier in the region, accounting for 20 per cent of world supply, and while LNG is responsible for only about 7 to 8 per cent of world gas production, these supplies are still vital in a tight market.

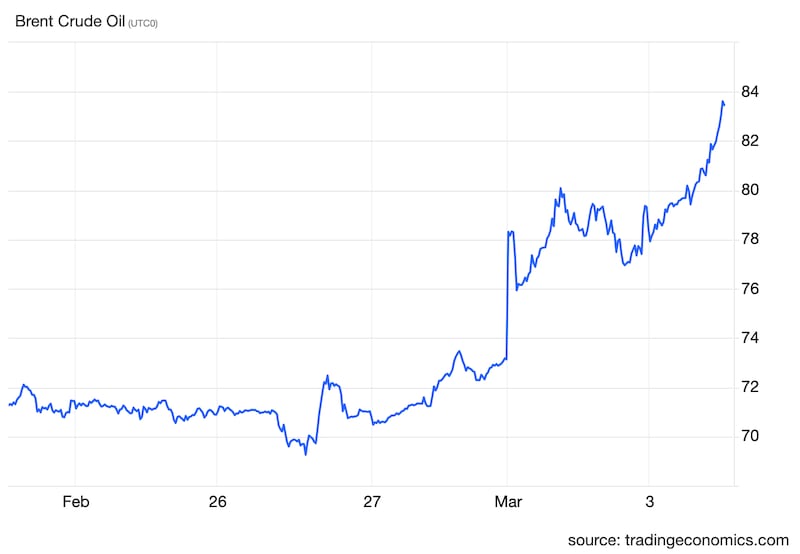

Oil $ per barrel

$ per barrel

Oil prices are also on the rise again and as we know can feed through quickly to petrol and heating oil. Brent crude, the key international measure, was trading on Tuesday morning at about $80 per barrel, up about 14 per cent since last week. Analysts believe it could top $100 soon enough if the conflict drags on. International oil stocks could be released to remove some of the immediate pressure but again a lengthy disruption could mean trouble.

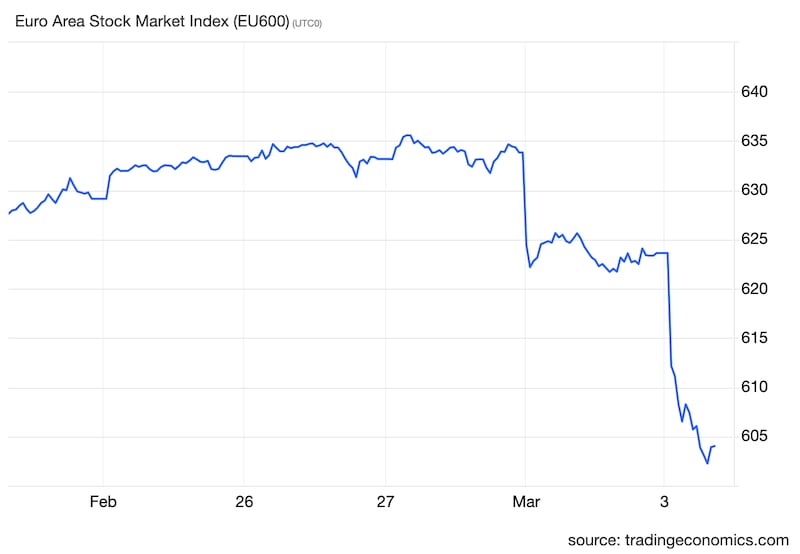

Stocks

Stock markets are being hit on Tuesday by the energy scares and by general signs that the conflict is spreading across the region, with implications for shipping, air transport and, of course, the region itself. The key reason is straightforward – higher energy prices hit many companies and are also a cost to countries who are net importers. They threaten both higher inflation and lower growth – so-called stagflation as it has been called in the past. Of course a quickish end to the conflict would remove these fears, but nobody knows how this will play out. Most of the big European markets are down a hefty 3 per cent-plus on Tuesday morning, as reflected in the drop on the Stoxx Europe 600 index which measures the fortunes of the biggest European players. In Dublin the Iseq index was trading close to 3 per cent lower.

Meanwhile, government bond prices are also falling due to fears about the inflation outlook, pushing longer-term interest rates higher. A prolonged war would lead to fears of a period similar to that which followed the invasion of Ukraine, when equity and bond prices were both falling – hitting pension funds – and interest rates were rising, hitting borrowers. We are not there yet, but the outlook for 2026 is now a lot more nervous.