Weekend Reading – Will AI Replace Financial Advisors?

Welcome to a new Weekend Reading edition about AI, replacing financial advisors. A take on that in a bit.

Here are some recent posts in case you missed them:

During my vacation in Belize, I wondered what the best asset allocation is entering retirement.

The Best Asset Allocation Entering Retirement

I just posted our latest montly dividend income update – a projected income forecast for the year.

February 2026 Dividend Income Update

Weekend Reading – Will AI Replace Financial Advisors?

Headlining this Weekend Reading theme is this post from Ben Carlson: Will AI Replace Financial Advisors?

To a point – would be my answer.

Like Ben, including what I wrote about just a few months ago on the rise of FinFluencers, AI is going to provide more financial planning tools to the personal finance toolbox.

This is a win.

Weekend Reading – The Rise of Finfluencers

DIY investors who are keen to learn how to save, invest and mind their taxes over time, may or may not use a financial planner let alone a fee-only planner anyhow. They would much prefer to improve on their own using lower-cost self-directed solutions and arguably on their own terms without the biases to grow a client base or assets under management charging 0.5%-1% (or more).

There is also a win for the wealth manager or wealth management firm in that they can automate more tools for their wealthy clients.

As Ben wrote: “There doesn’t necessarily have to a zero-sum game with winners and losers.”

Back to the subject of Finfluencers for a moment, in my letter to OSC (Ontario Securities Commission) staff notice related to guidance on how securities laws apply to the activities of social media financial influencers (finfluencers) and to registrants and issuers who work with them – I can share my thoughts on AI and this subject in the following way.

(A letter that I took time to write but never got a reply or even a simple acknowledgement, unfortunately.)

Here is part of that letter from December 2025:

“In many cases, finfluencers offer a form of accessibility, trend-sharing, general information and in some cases when the individual is diligent, valuable financial education that traditional channels have simply failed to provide.

Some finfluencers have achieved financial independence themselves, at an earlier age than most, offering proof that self-directed investing in Canada can be very successful when approached thoughtfully.

While some finfluencers are democratizing access to financial information—sharing information and progress in this regard comes with trade-offs and risks to safeguard against. This can be especially true when a few ‘bad apples’ may ruin the progress of a well-intentioned bunch.

Investors must be encouraged to think critically, cross-reference any notion of advice with reputable sources, and, when necessary, consult credentialed professionals for tailored, personalized decision-making.

In my opinion, the key is not to avoid finfluencer content entirely, but to consume it as part of a broader, more holistic financial education strategy while maintaining appropriate skepticism about sources, motivations, and the limitations of accessing information from anywhere, anytime in our modern age.

Ultimately, Canadian investors will be far better served where there is a broader menu of tools and solutions that vary in scale and cost for everyone without the reliance of just a professional community of folks that may or may not put client needs first – rather, they focus on the business they operate in or the business mandates they serve.”

I welcome your thoughts on AI, FinFluencers and again, anything else on this site. I read everything. 🙂

Weekend Reading – Beyond Will AI Replace Financial Advisors?

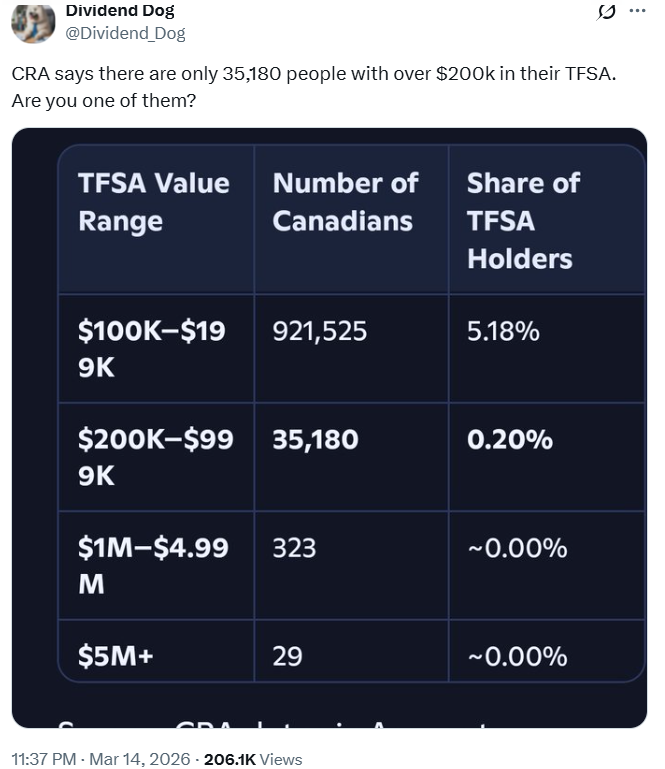

How much do you have in your TFSA?

CRA says you’re in the top percentile if you have more than $200,000 in your account.

Thanks to @Dividend_Dog for this. Source: https://x.com/Dividend_Dog/status/2033024884209586302

Is tipping culture out of whack? Might be.

The default option for a recent dinner I went out for was starting at 20%.

From the article:

“Lingering frustration among those polled is increasingly shaping consumer behaviour:

89 per cent resent businesses that prompt for tips they feel are unwarranted.

41 per cent actively avoid businesses known for aggressive tip prompts.

79 per cent enter their own tip amount rather than selecting a suggested percentage.

89 per cent believe tip percentages have become too high.”

And finally, since I’m getting excited for golf season – here is a great swing tip/drill.

I hit balls from time to time by keeping a golf glove tucked under my left armpit like Grand Slam Winner Rory McIlory does above.

Why?

It helps keep my arms, specifically my left arm “connected” to my body.

I have used this drill over the years with 7-irons at the range with about 30-40 balls. I swing at about 50-75%. I figure if this drill is good enough for Rory McIlroy then it’s good enough for me…!

Have a great weekend avoiding high tips (!), or working on your golf swing, and I look forward to your comments.

Mark

My name is Mark Seed – the founder, editor and owner of My Own Advisor. As my own DIY financial advisor, I’ve reached financial independence. Now, I share my lessons learned for free on this site. Join the newsletter read by thousands every week.