KUALA LUMPUR (Jan 28): Many Malaysians may spend decades working yet still reach retirement without meaningful financial security, according to the latest report by the PNB Research Institute (PNBRI). The report warns that relying on traditional poverty-alleviation measures and subsidies is no longer sufficient as the country rapidly ages.

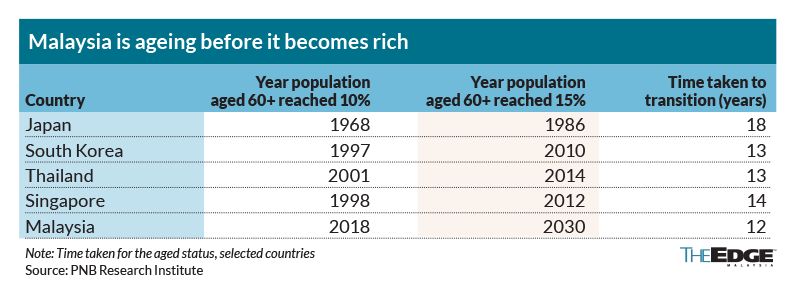

Malaysia is ageing before becoming a high-income nation, leaving households with weaker incomes, limited savings, high debts, and thinner financial buffers compared with wealthier peers like Japan, South Korea and Singapore.

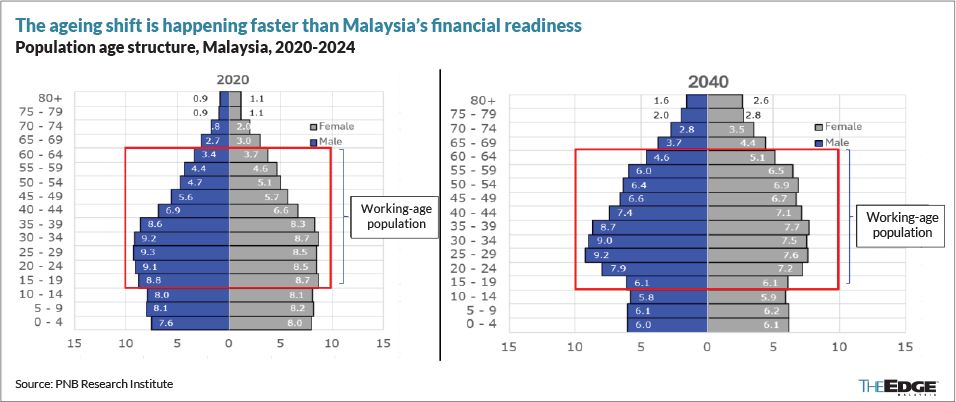

Malaysia has already crossed the “ageing society” threshold, with the share of the population aged 65 and above surpassing 7% in 2022 and rising to 7.7% by 2024. This proportion is projected to double to about 14% by 2040, marking the country’s transition into an “aged nation” within just over two decades.

By 2040, one in seven Malaysians will be aged 65 or older, yet many younger and middle-aged workers are already struggling to accumulate assets or build long-term financial stability.

The report shows that stagnant wages and income inequality make it hard for Malaysians to build wealth. Real wages for young graduates have barely grown in 20 years, while the richest 10% control nearly 60% of wealth. About half of EPF contributors have less than RM10,000 in savings, enough for only three months of retirement. Nearly 60% of workers earn under RM4,000 a month, and the gap between high- and low-income households remains large, with the bottom 20% holding less than 6% of national income and the top 20% capturing about 41%.

PNBRI calls for a shift in policy focus from alleviating poverty to ensuring economic security. Rather than simply providing income transfers or subsidies, the government should promote lifetime financial stability through three pillars.

The first is capability – equipping individuals with not just employable skills, but financial literacy, lifelong learning, and pathways to higher-paying, asset-building opportunities.

“In Malaysia, capability has not translated into mobility. Despite record educational attainment, real wage growth for young workers has stalled, underemployment remains high and skill mismatches persist. In an economy where the median young graduate earns between RM2,500 and RM3,000 per month, asset accumulation becomes difficult when entry-level homes in major urban centres are priced at approximately six to seven times the annual median income,” it said.

Capability gaps are also reflected in the decoupling of skills, productivity and wages, where productivity growth has outpaced wage growth since the 2000s, weakening the link between work and long-term wealth building.

Fragmented learning ecosystems — spanning technical and vocational training, higher education and employer-based training — further limit mobility, while informal, gig and contract workers often lack access to contributory systems such as retirement savings and social insurance.

The second pillar is ownership – enabling broader access to productive assets, including savings schemes, co-investment funds for housing, and employee ownership programmes.

The report cited international examples such as matched savings schemes — including Singapore’s Child Development Accounts and the Individual Development Accounts piloted in the United States — which demonstrate how government top-ups can accelerate asset accumulation among low- and middle-income families.

It also pointed to co-investment funds for first-home buyers, such as the UK’s Help-to-Buy Equity Loan and shared-equity models in Australia, which help reduce leverage risks while broadening access to property ownership.

Employee ownership schemes, which originated in the US and are gaining traction in the UK, were also highlighted as being associated with higher worker productivity, stronger firm loyalty and improved retirement preparedness.

Meanwhile, incentives that reward long-term savings and capital formation — including tax-advantaged retirement accounts and time-locked savings schemes — have proven effective in encouraging sustained asset accumulation, particularly among middle-income households, it added.

PNBRI said a truly economically secure system combines all three, capability — ability to create value, ownership — ability to keep and grow assets and resilience — ability to protect assets over time.

Building resilience means moving from fragmented protection to a system that supports households across shocks, life stages, and insecure work.

Key measures recommended include:

Universal and portable social protection, especially for gig and informal workers;

Emergency savings schemes to prevent financial distress;

Better integration of data across savings, insurance, and fiscal systems for targeted support;

Climate adaptation funds and risk-sharing to protect low-income households; and

Strong public services (healthcare, education, childcare, transport) to reduce costs and help families save, take risks, and build assets

“The challenge is not only protecting older Malaysians,” the report noted. “It is also ensuring that younger and middle-aged workers can convert their demographic advantage into real economic security, supported by broader asset ownership rather than higher consumption.”

PNBRI qualified that its research introduces the idea of three “engines” for an economically secure state but does not provide a full development model or social contract. The tools discussed — like wealth-building programmes, micro-equity platforms, and social protection — need more research, testing and public discussion.

The main contribution is conceptual: it frames a way for Malaysia to think about development where individuals are active builders of economic security, not just passive participants in welfare.