Bloomberg

Bloomberg

(Bloomberg) — The biggest tech companies are gearing up to spend even more on artificial intelligence than investors had anticipated, and money managers increasingly fear that whatever happens, credit markets will get hit.

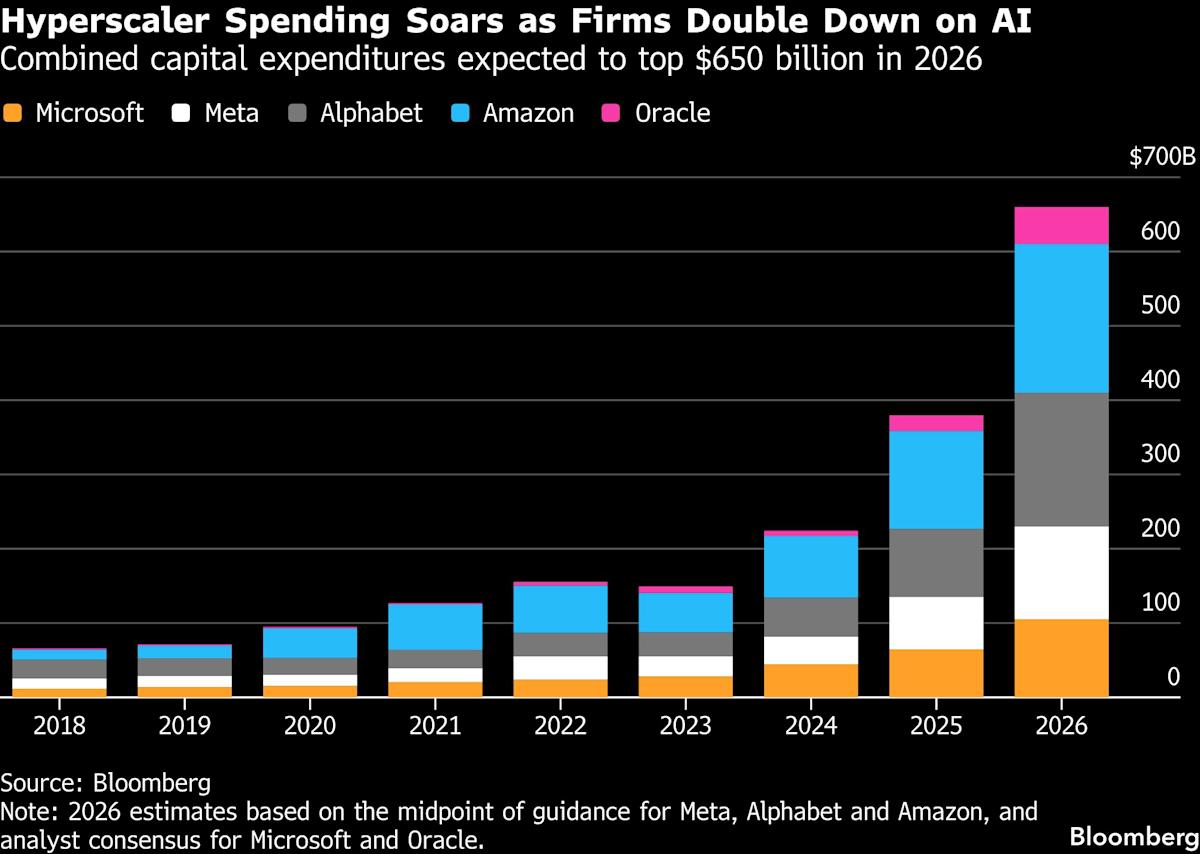

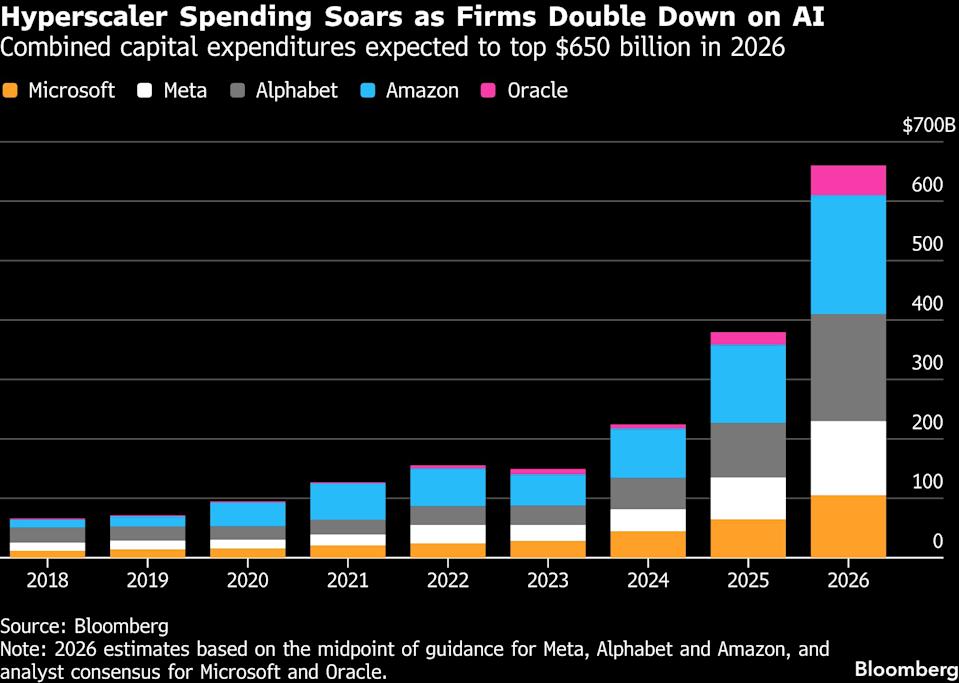

Microsoft Corp., Oracle Corp. and other “hyperscalers” are in an arms race to invest in AI and beat competitors in a technology that could change vast parts of the economy. Google parent Alphabet Inc. said it’s poised to spend as much as $185 billion on data centers this year, more than it has invested in the past three years combined. Amazon.com Inc. promised an even bigger outlay: $200 billion.

Most Read from Bloomberg

A chunk of those investments will come from the high-grade corporate bond market, potentially resulting in more debt sales this year than investors had expected. But the more tech companies borrow, the greater the potential pressure on bond valuations. The securities are already expensive by historical standards, trading at close to their tightest spreads since the late 1990s.

“The AI spending bonanza is finding buyers today but leaves little upside and even less room for error,” said Alexander Morris, chief executive officer and co-founder of F/m Investments. “There is no asset class that can’t and won’t spoil.”

Those fears weighed on tech companies’ notes this week, which broadly weakened relative to Treasuries, including most of the $25 billion of debt that Oracle sold on Monday. In the broader market, high-grade corporate bond yield spreads edged about 0.02 percentage point wider this week.

Beyond supply and demand, intensifying worries around AI’s power to disrupt have sparked tremors in the market. As companies like Anthropic PBC release a steady stream of tools targeting professional services from finance to software development, investors are starting to price in the threat AI poses to entire businesses.

Software companies have seen their leveraged loan prices drop about 4% this year through Thursday, according to Bloomberg index data, amid fears that AI will leave many software products obsolete.

Publicly traded lenders known as business development companies also have extensive exposure to software, with the industry accounting for more than 20% of portfolios on average, according to a note from Barclays. A BDC equity index fell 4.6% this week.

Story Continues

In the high-grade and high-yield bond markets, software companies are comparatively less represented, accounting for around 3% of each, according to Barclays. Still, one factor that makes corporate bonds vulnerable to rising risks is valuations, which remain high even with recent weakening.

The average US high-grade corporate bond spread was 0.75 percentage point at Thursday’s close, according to Bloomberg index data.

“Tight valuations make credit susceptible to potential disruption,” Barclays strategists Brad Rogoff and Dominique Toublan wrote in a Friday note.

JPMorgan Chase & Co. in November forecast about $400 billion of high-grade US bond sales from the technology, media and telecom sector this year. But that figure could climb as companies’ spending plans increase.

For all the concerns around looming supply, it’s likely that, for now, current demand for investment-grade bonds is even greater. Money has been chasing deals this year even though spreads remain near their tightest in decades.

High-grade technicals — market parlance for the balance between supply and demand as revealed by data like dealer inventories and the cash balances of credit funds — have remained robust despite record-setting issuance in the US and across the globe. Funds that invest in high-grade bonds saw $6.44 billion of inflows in the week ended Feb. 4, according to LSEG Lipper, the biggest inflow in over five years.

But as these tech giants ramp up their spending plans and sell more debt to fund their AI projects, technicals should continue to weaken, according to Nathaniel Rosenbaum, head of US credit strategy at JPMorgan.

Prone to Shocks

New issues over the past 10 days have underperformed the JPMorgan US Liquid Index by 4 basis points, the largest such underperformance since October, Rosenbaum wrote in a note Friday. That’s even as dealer inventories remain near record lows.

“To the extent issuance picks back up again over the remainder of the month, as we believe it will, there is room for further technical weakness ahead,” Rosenbaum wrote.

It’s possible that investors could swoop in and buy bonds as they become cheaper, shifting from either money market funds or mortgage bonds that have generated big gains, said Andrzej Skiba, head of US fixed income at RBC Global Asset Management’s BlueBay Fixed Income, during a Bloomberg TV interview on Friday.

Still, the confluence of tech’s borrowing binge, tight spreads and rising credit risks tied to AI make for a potentially precarious environment for investors — and one easily prone to shocks.

“It doesn’t take too many adverse events to create a selloff and for the prices to collapse,” said Ali Meli, founder and CIO of Monachil Capital Partners. “While credit markets may appear very liquid when the markets are good, the buyers can quickly disappear.”

WATCH: This week’s guests include JPMorgan Asset Management’s Oksana Aronov, Doubleline Capital’s Deputy Chief Investment Officer Jeff Sherman, Oaktree Capital Management’s Danielle Poli, RBC Global Asset MGMT. Head of BlueBay Andrzej SkibaJPMorgan Asset Management’s Oksana Aronov, Doubleline Capital’s Deputy Chief Investment Officer Jeff Sherman, Oaktree Capital Management’s Danielle Poli, RBC Global Asset MGMT. Head of BlueBay Andrzej Skiba

Click here for a podcast with H.I.G. on distressed opportunities amid the biggest loan slump in years

Week In Review

Global bond issuance has reached $1 trillion in record time as borrowers seize soaring demand to lock in relatively cheap costs. Tech companies in particular are expected to make up a larger share of supply as quarterly results get released and firms emerge from earnings blackouts.

Foreign investors bought American corporate bonds at the fastest monthly pace in nearly three years in January, as stable yields and lower hedging costs boosted the appeal of US credit, JPMorgan Chase & Co. data shows.

However, BlackRock Inc.’s Rick Rieder said he’s reducing exposure to US investment-grade and high-yield bonds while increasing holdings of emerging-market debt, citing favorable valuations and a soft dollar.

Prison-food vendor TKC Holdings Inc. is seeking to raise more than $2 billion to refinance expensive debt, a deal likely to test appetite from investors who’ve historically shunned the for-profit prisons industry.

Bank of America Corp. priced a $7 billion sale of investment-grade bonds, adding to a flurry of offerings by major Wall Street banks.

Goldman Sachs Group Inc. is readying a revised $3.75 billion financing — now likely to include a junk bond offering — to support chemical maker Arclin Inc.’s acquisition of DuPont de Nemours’ Aramids business.

Banks are preparing to sell $3.75 billion in debt to back Stonepeak Partners’ acquisition of a majority stake in BP Plc’s Castrol division.

A Cipher Mining Inc. subsidiary is seeking to raise $2 billion in the US junk bond market to help fund construction of a data center tied to Amazon.com Inc.

Bankers are working on debt packages of around €2.5 billion ($2.9 billion) to back a potential acquisition of Continental AG’s industrial ContiTech unit.

Norinchukin Bank is discussing a capital injection into a joint venture that said its estimated loss from debt linked to First Brands Group has ballooned to almost $1 billion.

Thoma Bravo raised the stakes in the fight between private equity firms and their lenders, by deploying a loan provision to help smoke out creditor rebellions before they even begin.

Private equity owned Multi-Color Corp. won court approval to start tapping a $250 million Chapter 11 loan, defeating a challenge from rival lenders that floated a competing financing.

Lenders to bankrupt restaurant operator FAT Brands Inc. want the chief executive officer suspended without pay over a recent stock sale for its Twin Peaks dining chain, deepening a battle for control of the company as it attempts to restructure.

Nearly 18 months after lenders to Pluralsight took over the educational-software business, some of them are booking fresh losses on their investments.

Nine Energy Service Inc., a Houston-based oil field vendor, filed for Chapter 11 bankruptcy as it struggled with high leverage and a shrinking business amid a slowdown in drilling programs.

Hong Kong’s largest developer Sun Hung Kai Properties Ltd. is seeking a loan of at least HK$5 billion ($640 million), returning to the market after skipping its annual refinancing last year.

On the Move

Eric Beinstein, head of US credit strategy at JPMorgan Chase & Co., is retiring after 40 years at the firm. US high-grade credit strategist Nathaniel Rosenbaum will be taking over as head, Beinstein wrote in his daily note on Wednesday.

Miguel Picache, the head of Citigroup Inc.’s private placement business, is retiring after nearly 25 years with the bank. The veteran banker will pursue other interests and spend time in the Philippines, he said in a LinkedIn post.

Fortress Investment Group managing directors Morgan McClure and Andrew Robbins, who served on the board of formerly bankrupt Red Lobster after a firm-led takeover of the chain, are set to leave both the board and Fortress.

UniCredit SpA has hired close to 20 investment bankers from Banco Santander SA’s former Polish unit as it seeks growth in the country. The recruitment focused on executives specializing in equity and debt underwriting as well as deal advisory.

–With assistance from Scarlet Fu, James Crombie, Michael Gambale, Brian Smith and Gerson Freitas Jr..

Most Read from Bloomberg Businessweek

©2026 Bloomberg L.P.