So why are prices so high? In many communities, the answer is straightforward: There is no longer meaningful competition in health care markets.

Across the country, many health care markets have consolidated into a handful of dominant firms. In Massachusetts, two systems — Mass General Brigham and Beth Israel Lahey Health — control a large proportion of inpatient beds, and the trend extends far beyond hospitals. Insurers are consolidating into a small number of dominant firms. Private equity firms are acquiring physician practices, and large corporations are housing insurers, pharmacies, and clinics under one roof. Both vertical (combining entities that provide different types of services such as insurers and hospitals) and horizontal (combining organizations with similar services) consolidation has become a defining feature of the US health care system. While these arrangements can theoretically deliver efficiency, they often lead to fewer choices and higher prices — costs that ultimately fall on patients.

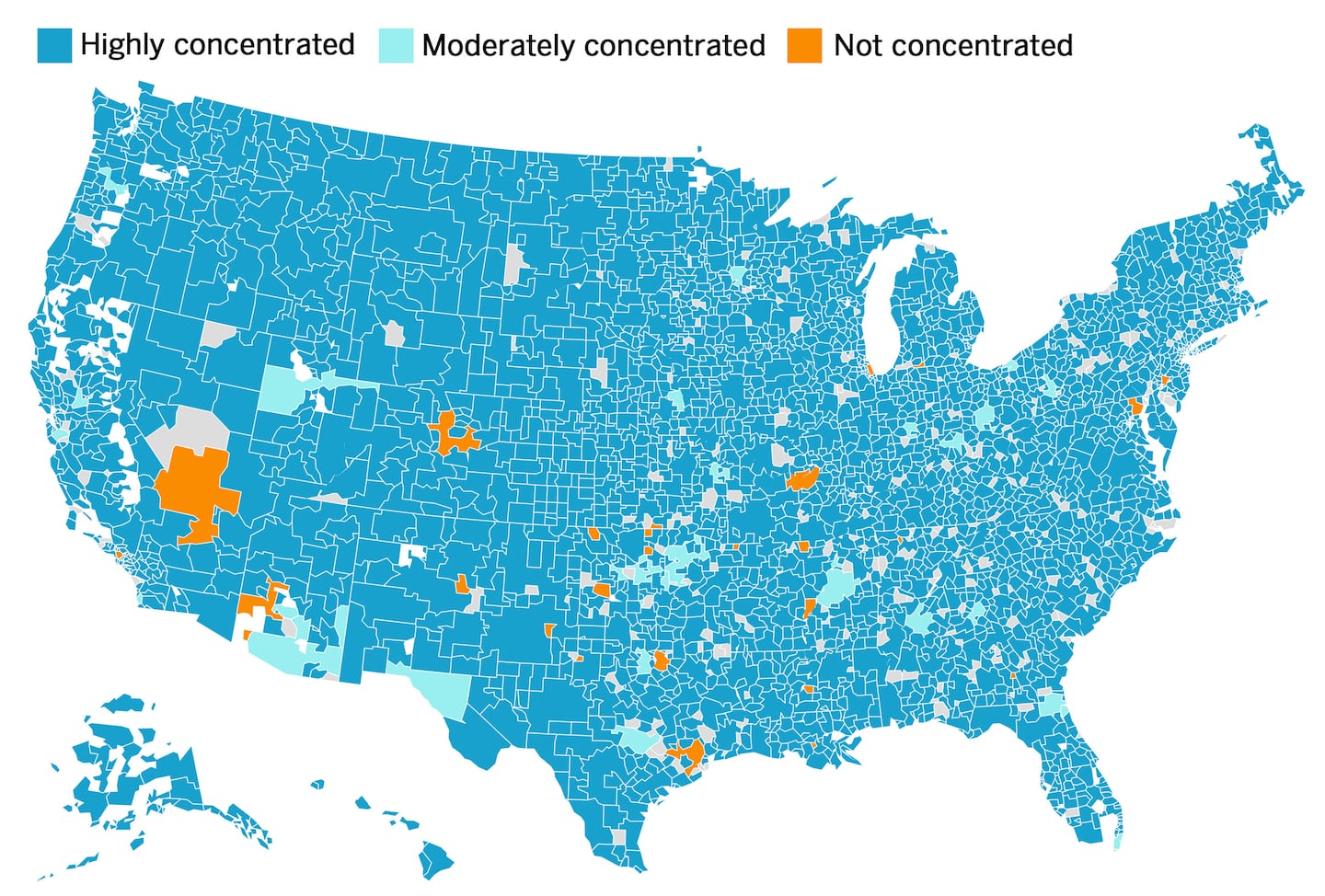

How concentrated is the hospital market near you?

This is a map of the 3,436 hospital service areas across the United States. An HSA is a local health care market where residents get most of their hospital care. The colors indicate if a hospital market is not concentrated (competitive), moderately concentrated, or highly concentrated (noncompetitive).

The data was calculated using the 2024 American Hospital Association Annual Survey, which provides hospital to 10,000 (monopoly). An HHI below 1,000 indicates a not concentrated hospital market, 1,000-1,800 is a moderately concentrated one, and above 1,800 is a highly concentrated one.CREDIT: Information Futures Lab/Brown University DATA SOURCES: Dartmouth Atlas of Healthcare, American Hospital Association/Credit: Information Futures Lab/Brown University DATA SOURCES: Healthcare Quality and Outcomes Lab, Harvard T.H Chan School and Center for Health System Sustainability, Brown University School of Public Health

The data was calculated using the 2024 American Hospital Association Annual Survey, which provides hospital to 10,000 (monopoly). An HHI below 1,000 indicates a not concentrated hospital market, 1,000-1,800 is a moderately concentrated one, and above 1,800 is a highly concentrated one.CREDIT: Information Futures Lab/Brown University DATA SOURCES: Dartmouth Atlas of Healthcare, American Hospital Association/Credit: Information Futures Lab/Brown University DATA SOURCES: Healthcare Quality and Outcomes Lab, Harvard T.H Chan School and Center for Health System Sustainability, Brown University School of Public Health

As competition erodes and prices rise, those costs are passed on to patients through higher premiums and out-of-pocket spending. In 2025, the typical American family of four was projected to pay close to $35,000 for health care — often reflecting the high price of care in markets with not enough competition.

To be clear, not every merger is harmful. In some cases, consolidation can lead to better care coordination, fewer unnecessary services, and lower administrative costs. But in other cases, mergers that promise “integration” end up delivering higher prices, fewer choices for patients, and potentially even lower quality of care. If health systems seek the benefits of consolidation, these health systems should be able to demonstrate with clear evidence that the merger will actually improve quality or reduce costs.

This situation reflects a series of policy choices that allowed health care markets to consolidate with little resistance. For years, antitrust enforcement in health care was weak, and regulators often treated nonprofit hospitals as “mission-driven” institutions exempt from normal market scrutiny. Policy makers, believing that larger systems would deliver better care at lower cost, encouraged consolidation. Too often, they were wrong — and prices rose instead.

Insurance markets followed a similar path. Lax oversight allowed insurers to grow larger without becoming better or more innovative, making it harder for new plans or alternative insurance designs to compete, ultimately leaving consumers with fewer choices. Some have argued that large insurers are needed to counterbalance large health systems. But that is not always the case. Two monopolies do not automatically create competition; they can instead entrench market positions.

If policy makers are serious about controlling health care spending, confronting high prices that are driven by a lack of competition must be a priority.

First, prior to major health care merger approvals, regulators should consistently demand comprehensive data analysis on the impact of the merger on prices, quality, and access. Too often these days the approvals are based on general financial projections or vague promises of integration.

Second, antitrust enforcement must go beyond reviewing new deals. In markets that are already highly concentrated, regulators should be willing to challenge past mergers that have demonstrably harmed consumers.

Third, where markets have become effectively monopolistic, policy makers should consider structural remedies, including divestitures or, when necessary, breaking up dominant systems to restore competition. Preventing consolidation would have been preferable, but in many cases that opportunity has passed.

Finally, nonprofit status should not confer special treatment from scrutiny around marketplace competition. Hospitals and insurers that behave like profit-maximizing firms should face a much higher bar for demonstrating community benefit, fair pricing, and transparency. Organizations that no longer meet that standard should not retain special protections.

Defenders of consolidation argue that scale is essential for stability. Some scale can help — but many health systems are well beyond that point. As experts have often noted, economies of scale can quickly turn into bureaucracy that dampen innovation and efficiency. Competition remains the most reliable engine for improving quality and controlling costs, and restoring it in health care is not about ideology. It is about fixing markets when they no longer work, giving people more choices, and easing the unsustainable burden that high health care prices continue to place on American families.