Palantir and Nvidia are each posting huge results.

Palantir Technologies (PLTR +5.37%) and Nvidia (NVDA +2.50%) are two of the biggest names in artificial intelligence (AI). One plays in the software realm while the other is on the hardware side. Both of these companies are making huge profits right now from the AI boom, but which one makes for the better investment?

I think each has a solid case for why it could be the ultimate winner, but only one can emerge as the best.

Image source: Getty Images.

Software revenue is longer lasting

Nvidia makes graphics processing units (GPUs), which are used in data centers globally to train and run AI models. This makes it the ultimate pick-and-shovel play for the AI gold rush. The company is making a ton of money right now from the GPUs it sells, and as data center construction expands, it will grow alongside that.

However, at some point in time, there will be enough computing capacity for AI. When this will occur is anyone’s guess, and it may not be until after 2030. When we hit that point, Nvidia’s growth will significantly slow, and a large chunk of its business will come from replacing burned-out or outdated GPUs, which can still be a great business, but just not one that’s growing as rapidly as it is now.

Today’s Change

(2.50%) $4.63

Current Price

$190.04

Key Data Points

Market Cap

$4.5T

Day’s Range

$183.95 – $193.66

52wk Range

$86.62 – $212.19

Volume

196M

Avg Vol

183M

Gross Margin

70.05%

Dividend Yield

0.02%

Palantir makes AI-powered data analytics software that helps its users make the most well-informed choices. This software was originally developed for use by governments in military and intelligence applications, but it eventually found widespread adoption in commercial markets as well.

Software is a much longer-lasting revenue stream. As long as another product doesn’t take its place and Palanitr can maintain a subscription service, it will provide perpetual revenue. Just look at Microsoft and its Office platform: That has been a cash cow since it was launched, and Palantir’s software could be the same.

This gives the edge to Palantir in terms of a business model, but there’s more to an investment than just that.

Palantir’s growth slightly edges out Nvidia’s

While we’re still waiting on Nvidia’s fourth-quarter results (due on Feb. 25), Palantir released its report the other day. It showed that revenue rose 70% year over year to $1.4 billion. And it’s doing so in a profitable manner, delivering a strong 43% margin.

Today’s Change

(5.37%) $7.30

Current Price

$143.20

Key Data Points

Market Cap

$324B

Day’s Range

$134.80 – $145.87

52wk Range

$66.12 – $207.52

Volume

2M

Avg Vol

46M

Gross Margin

82.37%

Nvidia typically reports a profit margin in the mid-50% range, so it’s slightly ahead in terms of profitability, but that’s just nitpicking. For the fourth quarter, Wall Street analysts expect 67% growth — and the company is known to outperform expectations, so seeing 70% growth, in line with Palantir’s, is entirely possible.

Both companies are growing at a blistering pace, so giving the edge to either in this comparison isn’t appropriate.

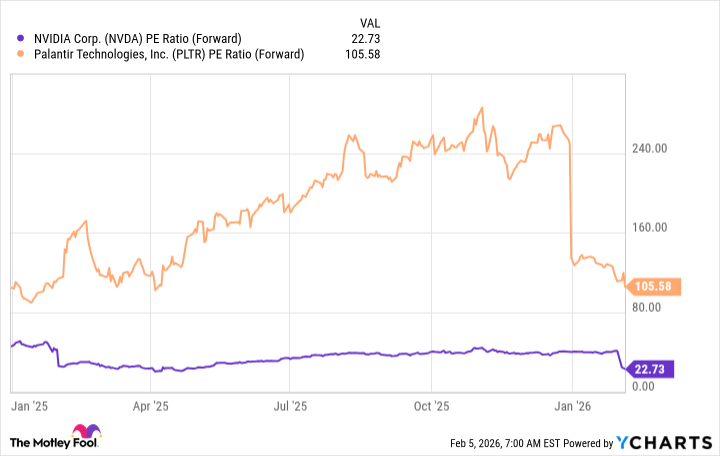

Nvidia’s stock is far cheaper than Palantir’s

Lastly, we need to look at valuation. Palantir’s stock is incredibly expensive; there’s no way around that. If you value each company using forward earnings, Nvidia trades at a huge discount.

NVDA PE Ratio (Forward) data by YCharts; PE = price to earnings.

At 106 times forward earnings versus 23 times, Palantir’s earnings projections would have to rise 360% to be at the same valuation as Nvidia’s. That means you must pay a huge premium to own Palantir’s stock over Nvidia’s.

Part of that premium is absolutely deserved due to Palantir’s software business model. However, I think having to pay over four times the cost to own Palantir’s stock versus Nvidia’s is absurd.

Nvidia is still the best stock to buy today, and I think it’s primed to have a huge 2026 as AI spending surges. The market is oddly bearish on the stock, and now is a great time to load up.