Get insights on thousands of stocks from the global community of over 7 million individual investors at Simply Wall St.

Samsung moves up its HBM4 production schedule and begins preparing for mass output of next generation high bandwidth memory chips.

Nvidia chooses Samsung, not Micron Technology (NasdaqGS:MU), as a primary HBM4 supplier for its upcoming Vera Rubin AI accelerators.

Micron shifts focus away from consumer memory products toward supplying high bandwidth memory for AI and enterprise infrastructure buyers.

Micron Technology, traded as NasdaqGS:MU, is a major producer of DRAM, NAND and high bandwidth memory used in data centers, AI systems and consumer electronics. The latest moves by Samsung and Nvidia highlight how critical HBM4 is becoming for next generation AI chips that require large, fast memory pools to keep accelerators fully utilized. For investors, this is less about short term headlines and more about which suppliers are integrated into the largest AI hardware platforms.

Micron’s pivot toward enterprise and AI memory indicates that the company is working to align more closely with large scale infrastructure spending as AI workloads expand. At the same time, Samsung’s role in Nvidia’s Vera Rubin program illustrates how competitive supplier selection can influence which companies are directly connected to major AI chip launches. How Micron executes on its enterprise focus, and which large buyers it secures, could affect how its memory mix is positioned in the AI market over time.

Stay updated on the most important news stories for Micron Technology by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Micron Technology.

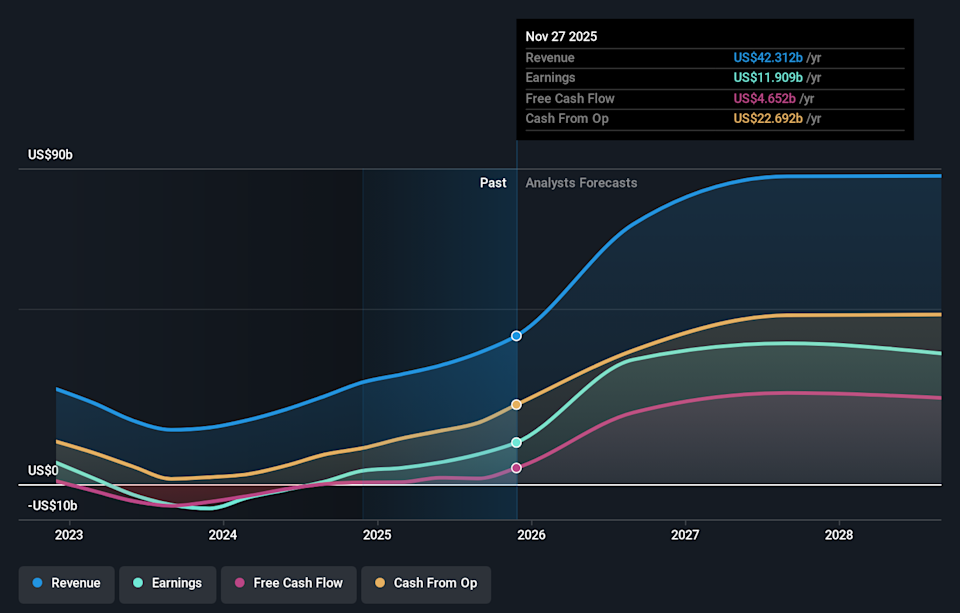

NasdaqGS:MU Earnings & Revenue Growth as at Feb 2026

NasdaqGS:MU Earnings & Revenue Growth as at Feb 2026

How Micron Technology stacks up against its biggest competitors

Samsung pulling forward its HBM4 schedule and winning prime placement in Nvidia’s next AI accelerator tightens the race for high bandwidth memory, but it does not remove Micron from the AI buildout story. For you as an investor, the key question is whether Micron can offset not being a first wave HBM4 supplier for this Nvidia platform by deepening relationships with other hyperscalers and chipset designers that also need large, high speed memory pools.

The community narrative around Micron highlights its push into advanced HBM, DRAM and NAND for AI data centers, supported by capacity expansions in the US and Asia and new process technologies like EUV and 1-gamma nodes. This news tests that thesis, because competitors such as Samsung and SK Hynix are moving quickly in HBM4, yet it also lines up with Micron’s shift away from consumer products toward higher value enterprise and AI memory where demand, including for Nvidia’s current H200 and Blackwell GPUs, has already been strong.

⚠️ Samsung’s earlier HBM4 ramp and Nvidia’s supplier choice could limit Micron’s share of this specific AI accelerator cycle and add pressure in a historically cyclical DRAM and HBM market.

⚠️ Execution risk is real as Micron raises capital expenditure to expand capacity and bets heavily on enterprise buyers, while analysts already flag that extra industry supply can hurt memory pricing.

🎁 Micron is benefiting from tight DRAM and HBM supply, contracted HBM volumes and strong AI driven demand across data centers, PCs and smartphones, which analysts link to improved earnings and margins.

🎁 Reward potential also comes from Micron’s repositioning as a core AI infrastructure supplier, with several narratives pointing to long term AI memory needs and supportive analyst sentiment.

From here, watch how quickly Micron brings its own HBM4 to market, the size and duration of supply agreements it secures with hyperscalers versus rivals like Samsung and SK Hynix, and any signs that added supply starts to cool pricing. If you want a broader view of how different investors see Micron’s long term AI role, take a few minutes to check community narratives on Micron’s dedicated page.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include MU.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com