In early February 2026, Philip Morris International reported fourth-quarter 2025 results showing sales of US$10,362 million and net income of US$2,141 million, alongside a new shelf registration for debt securities and warrants.

These results capped a full-year 2025 in which sales rose to US$40,648 million and net income reached US$11.35 billion, underpinned by rapidly expanding smoke-free products such as IQOS, ZYN, and VIVE and management’s guidance for further earnings growth in 2026.

We’ll now examine how this strong smoke-free earnings momentum and upbeat 2026 outlook may influence Philip Morris International’s investment narrative.

Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

To own Philip Morris International, you need to believe its smoke-free portfolio can more than compensate for the structural decline in combustible cigarettes, despite regulatory and tax uncertainty. The latest results, showing Q4 and full-year 2025 profit growth led by IQOS, ZYN, and VIVE, broadly support that thesis. In the near term, the key catalyst is continued smoke-free volume and earnings growth, while the biggest risk remains regulatory pressure that could slow adoption or constrain margins. The February news does not materially change that balance.

The most relevant recent announcement here is PMI’s new shelf registration for debt securities and warrants, filed alongside the earnings release. This gives the company flexibility to raise capital in future, which matters because its smoke-free transition depends on ongoing investment in capacity, R&D, and product rollouts like IQOS and ZYN. How efficiently PMI funds that spending, given its already high debt levels, ties directly into the earnings growth investors are watching.

Yet beneath the strong smoke-free momentum, investors should still be aware of how shifting public health sentiment and tightening regulation could eventually affect…

Read the full narrative on Philip Morris International (it’s free!)

Philip Morris International’s narrative projects $49.4 billion revenue and $14.5 billion earnings by 2028. This requires 8.2% yearly revenue growth and about a $6.3 billion earnings increase from $8.2 billion today.

Uncover how Philip Morris International’s forecasts yield a $180.38 fair value, a 4% downside to its current price.

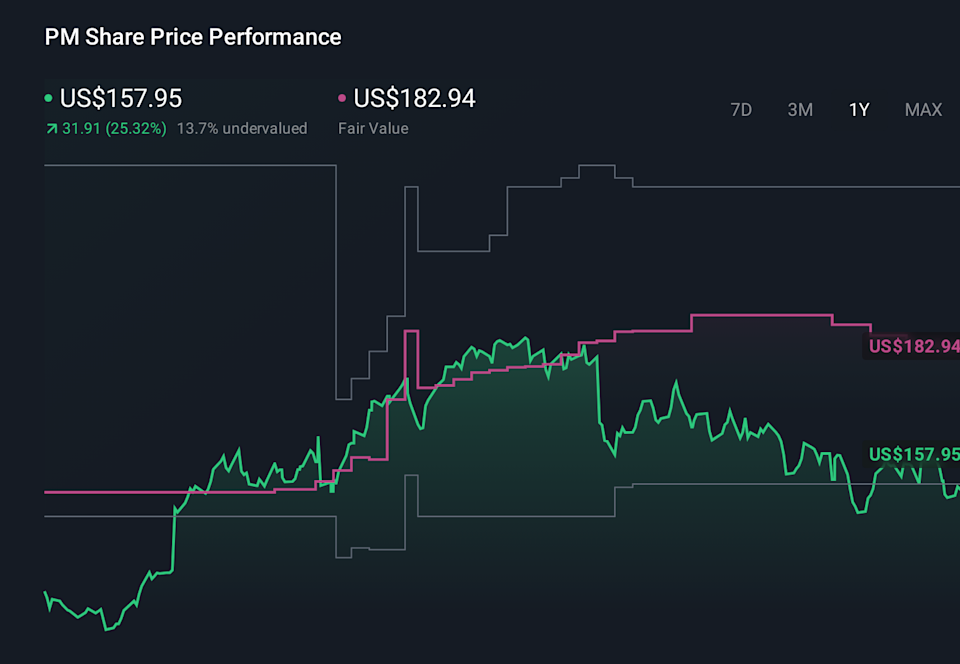

PM 1-Year Stock Price Chart

PM 1-Year Stock Price Chart

Some of the lowest ranked analysts came in much more pessimistic, assuming revenue of about US$47.1 billion and earnings of US$14.4 billion by 2028, and arguing that rising ESG pressures and stricter health regulation could limit the payoff from smoke-free growth, so it is worth comparing those assumptions with the latest results and deciding which risk story you find more convincing.

Explore 11 other fair value estimates on Philip Morris International – why the stock might be worth 16% less than the current price!

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Markets shift fast. These stocks won’t stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include PM.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com