EZCORP (EZPW) is back in focus after reporting first quarter fiscal 2026 results that showed higher revenue and net income, alongside a new three year, US$50 million share repurchase program funded by internal cash resources.

See our latest analysis for EZCORP.

That update landed after a strong run in EZCORP’s shares, with a 30 day share price return of 13.65% and a 90 day share price return of 36.96%. The 1 year total shareholder return of 73.02% and 5 year total shareholder return of about 4x highlight how sentiment around earnings, M&A activity and the new buyback has been building over time.

If this kind of corporate activity has your attention, it could be a good moment to widen your search and check out our 23 top founder-led companies as potential next ideas.

With earnings, M&A ambitions and a fresh US$50 million buyback all in play, EZCORP’s recent share price surge raises a key question for investors: is the real upside still ahead, or is the market already pricing in future growth?

Most Popular Narrative: 3% Overvalued

The most followed narrative puts EZCORP’s fair value at $23.60, slightly below the last close of $24.31. This implies a modest premium built into the current price.

Improving profitability, combined with tighter execution, is not yet fully reflected in the current share price. As a result, they continue to describe the valuation as conservative relative to EZCORP’s operational gains and future growth potential.

Want to see what sits behind that “conservative” label? The narrative leans on steady growth, firmer margins and a future earnings multiple that assumes investors stay patient. Curious which specific operating trends and forecasts are doing the heavy lifting in that fair value math? The full breakdown lays those expectations out in detail.

Result: Fair Value of $23.60 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, there is still real execution risk if gold prices soften or store expansion stumbles. This could pressure margins and challenge the current “conservative” label.

Find out about the key risks to this EZCORP narrative.

Another Angle On Valuation

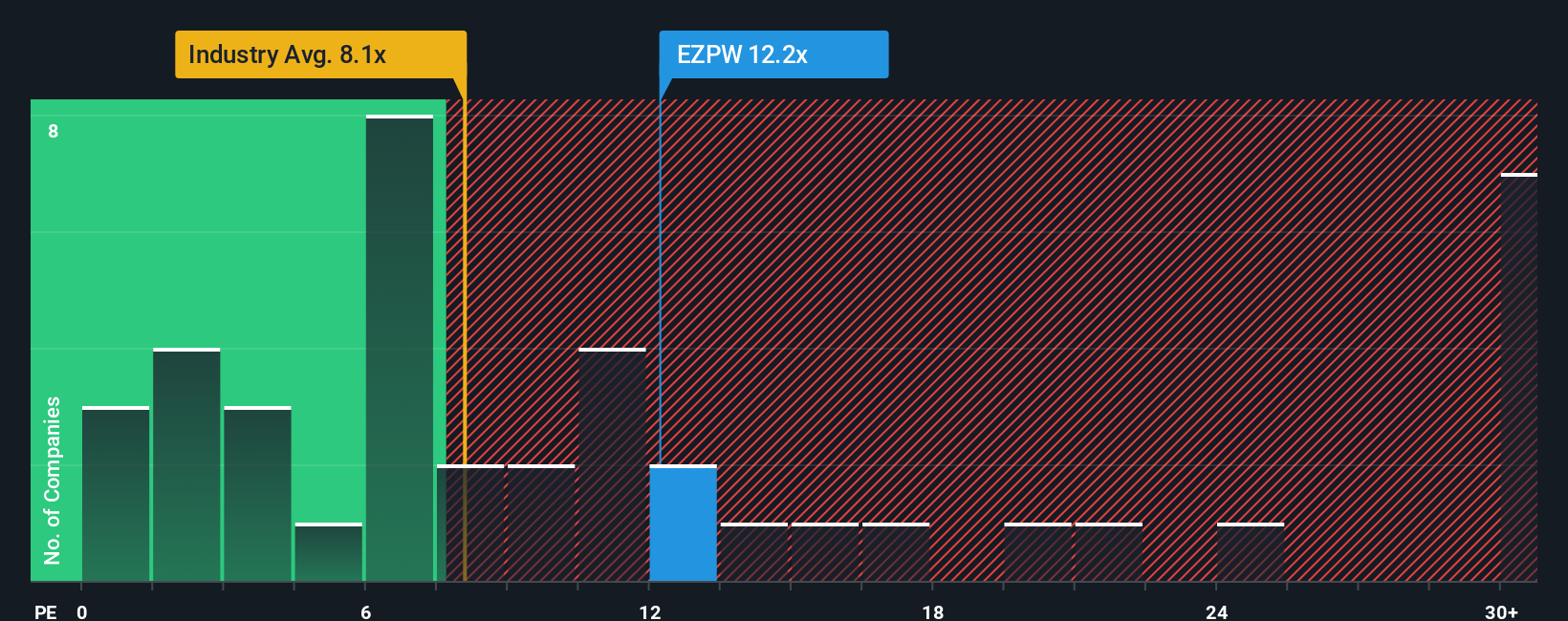

While the narrative model lands on a fair value of $23.60 and describes EZCORP as slightly overvalued at $24.31, the P/E picture is more nuanced. The current P/E of 12.2x is below the fair ratio of 13.9x, yet well above the US Consumer Finance industry at 8x and the peer average at 5.2x. This combination of apparent value and relatively higher sector pricing raises a simple question: is this a quality premium you are comfortable paying, or a valuation risk you would rather avoid?

See what the numbers say about this price — find out in our valuation breakdown.

NasdaqGS:EZPW P/E Ratio as at Feb 2026 Build Your Own EZCORP Narrative

NasdaqGS:EZPW P/E Ratio as at Feb 2026 Build Your Own EZCORP Narrative

If you are not fully sold on this view, or simply prefer to test the numbers yourself, you can build a custom thesis in minutes with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding EZCORP.

Looking for more investment ideas?

If EZCORP has sharpened your focus, do not stop here. Broaden your watchlist with other ideas that match your style before the next move passes you by.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if EZCORP might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com