Make better investment decisions with Simply Wall St’s easy, visual tools that give you a competitive edge.

If you are wondering whether Dropbox shares offer solid value at today’s price, it helps to step back from the headlines and look closely at what the current market is implying.

The stock last closed at US$24.53, with returns of a 1.9% decline over 7 days, a 7.5% decline over 30 days, an 8.9% decline year to date, a 25.2% decline over 1 year, and positive returns over 3 and 5 years.

Recent moves in the share price have kept investor attention on how Dropbox is positioning itself in the crowded cloud storage and collaboration space. Ongoing product updates, partnerships, and changing sentiment toward software companies generally help frame how the market is currently thinking about its long term prospects.

On our valuation checks, Dropbox scores 5 out of 6 for potential undervaluation, as shown in its valuation score. Next, we will compare what different valuation approaches are indicating, then finish with a way of looking at value that can give you an even clearer overall picture.

Find out why Dropbox’s -25.2% return over the last year is lagging behind its peers.

A Discounted Cash Flow, or DCF, model estimates what a company might be worth today by projecting its future cash flows and then discounting those back to a present value. It is essentially asking what those future dollars are worth in today’s terms.

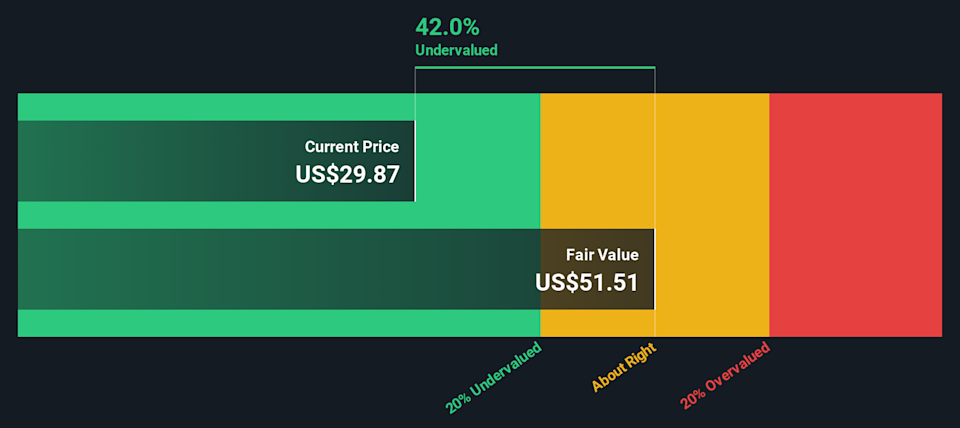

For Dropbox, the model uses a 2 Stage Free Cash Flow to Equity approach. The company recently generated trailing twelve month free cash flow of about $906 million. Analysts provide explicit free cash flow estimates for the next few years, and Simply Wall St then extrapolates those out, with projections rising to around $1.12 billion in 2035, all expressed in US dollars.

When those projected cash flows are discounted back and divided by the number of shares, the DCF model arrives at an estimated intrinsic value of about $50.79 per share. Compared with the recent share price of $24.53, this implies the stock is around 51.7% undervalued according to this method.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Dropbox is undervalued by 51.7%. Track this in your watchlist or portfolio, or discover 53 more high quality undervalued stocks.

DBX Discounted Cash Flow as at Feb 2026

DBX Discounted Cash Flow as at Feb 2026

For profitable companies, the P/E ratio is a useful way to anchor the share price to the earnings that support it. You are essentially asking how many dollars investors are currently willing to pay for each dollar of earnings.

Story Continues

What counts as a normal or fair P/E usually reflects two big pieces: how the market views a company’s growth prospects, and how risky those earnings appear. Higher expected growth or lower perceived risk can justify a higher P/E, while lower expected growth or higher risk tend to pull the P/E down.

Dropbox currently trades on a P/E of 12.6x, compared with a Software industry average of about 26.4x and a peer group average of 29.2x. Simply Wall St’s Fair Ratio for Dropbox is 21.6x, which is its proprietary view of what a reasonable P/E could be given factors such as earnings growth, profit margins, industry, market value and risk profile. This Fair Ratio can be more tailored than a simple industry or peer comparison because it adjusts for Dropbox specific characteristics rather than assuming all software companies deserve the same multiple. On this measure, Dropbox’s current P/E sits below the Fair Ratio, which points to the shares looking undervalued on a P/E basis.

Result: UNDERVALUED

NasdaqGS:DBX P/E Ratio as at Feb 2026

NasdaqGS:DBX P/E Ratio as at Feb 2026

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St you can use Narratives, where you and other investors connect your story about Dropbox to specific forecasts for revenue, earnings and margins. You can then see how that story translates into a Fair Value, compare it with the live share price to frame potential buy or sell decisions, and watch it update automatically as new news or earnings arrive. This is why one Dropbox Narrative on the Community page might anchor on a bearish US$20 fair value, while another uses a more optimistic US$35 fair value, even though both are built from the same underlying data and tools.

For Dropbox however we will make it really easy for you with previews of two leading Dropbox Narratives:

🐂 Dropbox Bull Case

Fair value in this narrative: US$28.57 per share

Difference between this fair value and the last close of US$24.53, expressed as a percentage of the fair value: about 14.2% lower than this narrative fair value

Revenue growth assumption in this narrative: 1.34% annual decline

Focuses on deeper AI integration, new product tiers, and better onboarding to improve monetization, retention, and cash flow from Dropbox’s large user base.

Assumes operational efficiency and cost discipline support solid margins and free cash flow while still funding product development and security.

Anchors on an analyst consensus fair value of US$28.57, with detailed assumptions for revenue, earnings, margins, share count, discount rate, and a future P/E of about 15.76x.

🐻 Dropbox Bear Case

Fair value in this narrative: US$20.00 per share

Difference between this fair value and the last close of US$24.53, expressed as a percentage of the fair value: about 22.7% above this narrative fair value

Revenue growth assumption in this narrative: 1.57% annual decline

Emphasizes churn and downsell pressure in Teams customers, reduced spending on non core products, and currency effects as potential drags on revenue and earnings.

Highlights concerns about execution on AI tools like Dash, near term growth uncertainty, and competitive pressure from larger suites as reasons to assume lower margins and constrained earnings.

Bases its US$20.00 fair value on lower revenue and earnings expectations, a slightly higher required return, and a trimmed future P/E multiple of about 10.88x.

Do you think there’s more to the story for Dropbox? Head over to our Community to see what others are saying!

NasdaqGS:DBX 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include DBX.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com