These companies are growing at healthy rates and are on track to capitalize on AI’s growth in their respective industries.

Artificial intelligence (AI) stocks have been witnessing bouts of volatility of late, primarily due to concerns about the significant increase in the capital expenses of tech giants. That’s re-ignited fears of a bubble, in addition to worries about the disruption that the adoption of this technology could cause in the software and services sector.

However, savvy investors would do well to look at the bigger picture. The reason tech giants and AI companies have been spending big bucks on AI infrastructure is the productivity gains this technology is expected to deliver. From automating processes to reducing redundancies to enhancing employee productivity, AI is set to contribute to the global economy in multiple ways.

Not surprisingly, market research firm IDC predicts that a dollar spent on AI services could generate $4.90 in value. That’s a good reason to take a look at Nebius Group (NBIS +4.33%) and Twilio (TWLO +2.03%), two stocks that could help investors capitalize on the growing proliferation of AI and that look like solid buys this month.

Image source: Getty Images.

Nebius Group: AI computing demand is a tailwind for this company

Nebius is a neocloud infrastructure company that provides AI hardware and software solutions. The full-stack nature of its platform means that customers can not only rent AI compute capacity from its data centers equipped with powerful graphics processing units (GPUs), but also run and manage their AI models and applications with its software solutions.

Today’s Change

(4.33%) $4.22

Current Price

$101.74

Key Data Points

Market Cap

$25B

Day’s Range

$96.90 – $104.39

52wk Range

$18.31 – $141.10

Volume

568K

Avg Vol

14M

Gross Margin

-765.63%

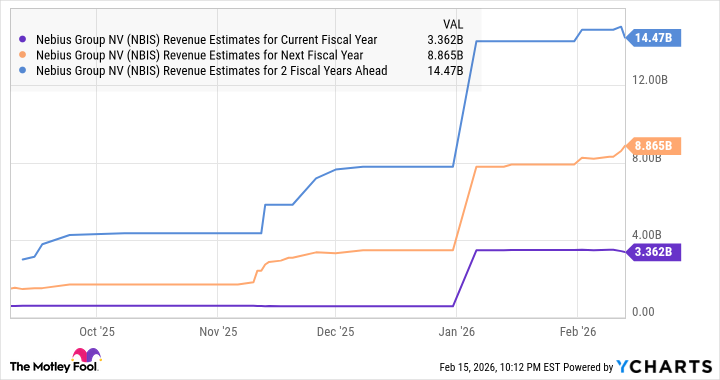

Nebius has established a solid customer base, including major names such as Meta Platforms and Microsoft. The company released its fourth-quarter 2025 results on Feb. 12, posting an almost sixfold jump in revenue to $530 million. Importantly, Nebius expects its annualized run rate revenue (ARR) to land between $7 billion and $9 billion by the end of 2026, a sevenfold increase from the end of last year.

The build-out of more data centers will drive this massive increase. Nebius was operating seven data center sites by the end of 2025. It plans to increase that number to 16 in 2026. The company ended the year with 170 megawatts (MW) of active data center power capacity, well above its 100 MW target. Nebius believes that it can end 2026 with 800 MW to 1 gigawatt (GW) of new capacity.

This aggressive capacity expansion will enable Nebius to convert its solid backlog into revenue, which explains why analysts are expecting a stronger jump of almost 6.4 times in 2026, followed by another big increase next year.

NBIS Revenue Estimates for Current Fiscal Year data by YCharts

Of course, this AI stock is expensive right now at 59 times sales, but that’s justified by its exponential growth and a huge revenue backlog that could ensure years of solid growth and result in healthy gains on the market.

Twilio: AI software demand is accelerating the company’s growth

Twilio may not be a household name in the AI software market like some of its peers, but its growth trajectory has been improving due to this technology. Twilio is a cloud communications company that helps its clients connect with their customers across various channels, including text, chat, voice, and video.

Today’s Change

(2.03%) $2.20

Current Price

$110.69

Key Data Points

Market Cap

$16B

Day’s Range

$105.84 – $112.46

52wk Range

$77.51 – $145.90

Volume

82K

Avg Vol

2.5M

Gross Margin

51.80%

Twilio helps its clients use customer interactions to boost their sales by enhancing the customer engagement experience through personalized recommendations. It has been using various AI tools to deliver better insights to clients about their customers, and this strategy is paying off.

For instance, Twilio’s Voice AI solution witnessed 60% year-over-year revenue growth in the fourth quarter of 2025. This solution helps clients automate their customer support operations, provides real-time response suggestions to customer service agents, and offers personalized recommendations to improve cross-sales.

Not surprisingly, Twilio’s active customer base increased by 24% year over year in Q4 2025 to 402,000, well above the 7% growth it witnessed in the same period last year. Even better, Twilio’s existing customers have increased their spending on its offerings. This was evident from the company’s dollar-based net retention rate of 109% last quarter, up from 106% in the year-ago period.

The metric compares the spending by Twilio’s customers at the end of a quarter with their spending in the year-ago period. So, the improvement in this metric is proof that AI tools are helping Twilio win a bigger share of its customers’ wallets. This, in turn, is driving solid bottom-line growth for the company.

While Twilio’s 2025 revenue increased by 14% to just over $5 billion, its adjusted earnings per share jumped by 33% to $4.89. The company expects to sustain its healthy momentum, forecasting a 15% increase in revenue in the current quarter. Twilio could exceed Wall Street’s 2026 revenue growth estimate of 7% at this pace and also register a bigger-than-anticipated jump in earnings.

That’s why it would be a good idea to buy this tech stock in February while it is trading at just 3.6 times sales and 20 times forward earnings, a discount to the tech-focused Nasdaq Composite index’s sales multiple of 5.3 and earnings multiple of 42. Moreover, the stock has a 12-month median price target of $147, according to 32 analysts covering it, suggesting potential gains of 28%.

It is likely to achieve such gains in the coming year, given its solid growth potential.