Arista Networks’ bright prospects could be a tailwind for this beaten-down stock.

Arista Networks (ANET 2.39%) is an important player in the artificial intelligence (AI) infrastructure ecosystem, providing software-driven networking solutions that enable high-speed data transmission in AI data centers, along with switches and routers that help transfer huge data sets quickly.

However, Arista stock has been under pressure in recent months. The stock ended 2025 on a sour note as the company was unable to produce enough components to meet customer demand. The long lead times pressured Arista’s growth.

However, the company could finally go on a bull run following its latest quarterly report. Let’s take a closer look.

Image source: Getty Images.

Arista Networks’ stock popped after its latest quarterly report

Arista released its fourth-quarter 2025 results on Feb. 12. Investors were impressed by the quarterly report, as its revenue and earnings exceeded expectations, propelled by healthy demand for networking switches and routers that power AI data centers. Arista also provided better-than-expected guidance for the current quarter.

Arista’s full-year revenue and earnings jumped nearly 29% last year to $9 billion and $2.32 per share, respectively. It is worth noting that high memory prices and supply constraints are likely to weigh on Arista’s performance in 2026. Even then, the company has raised its 2026 revenue growth estimate to 25% from the prior estimate of 20%.

Today’s Change

(-2.39%) $-3.18

Current Price

$129.71

Key Data Points

Market Cap

$167B

Day’s Range

$127.00 – $132.60

52wk Range

$59.43 – $164.94

Volume

175K

Avg Vol

7.6M

Gross Margin

64.06%

It is easy to see why Arista is more upbeat about its 2026 performance. The company continues to receive orders at a robust clip for its networking components, which is why its deferred revenue balance jumped to $5.4 billion in Q4 from $4.7 billion in the previous quarter. Deferred revenue is the money Arista collects in advance for products and services it will provide at a later date, suggesting it already has a solid revenue pipeline that should help it deliver robust growth in 2026.

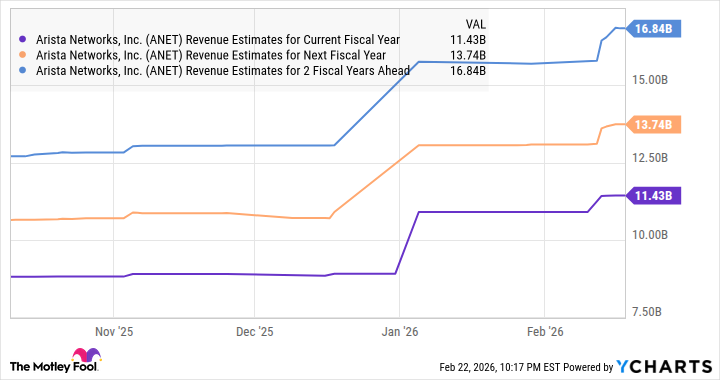

What’s more, Arista is poised to benefit from a fast-growing end-market opportunity in the long run. The company estimates that the data center Ethernet switch market could generate $110 billion in revenue by 2030, up from around $30 billion last year. That explains why analysts are forecasting an uptick in Arista’s growth.

ANET Revenue Estimates for Current Fiscal Year data by YCharts

Analysts anticipate a nice jump in this networking stock

A 12-month median price target of $177.50 suggests a potential upside of 33% for this AI stock. What’s more, nearly all the 25 analysts covering Arista suggest buying the stock.

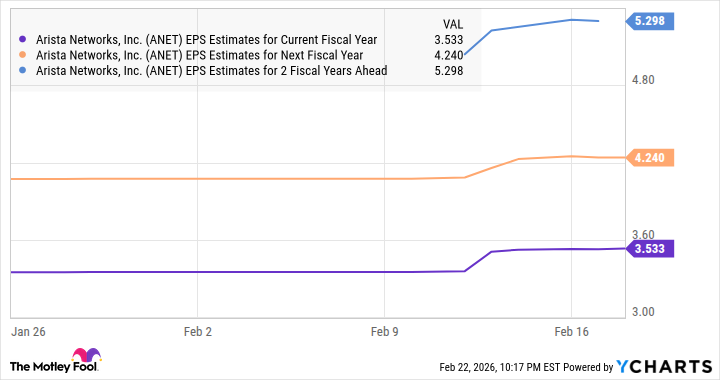

Of course, Arista stock trades at an expensive 44 times forward earnings right now, a premium to the tech-laden Nasdaq-100 index’s forward earnings multiple of 26. However, the potential acceleration in its earnings growth could help justify the premium valuation.

ANET EPS Estimates for Current Fiscal Year data by YCharts

So, it won’t be surprising to see Arista hit Wall Street’s price target in the coming year and head higher in the long run, as it is in a solid position to capitalize on the huge spending on AI data centers.