Make better investment decisions with Simply Wall St’s easy, visual tools that give you a competitive edge.

Globant (NYSE:GLOB) is shifting to an AI-native Pods subscription model, reshaping how it delivers its services.

The company reported record revenue and free cash flow alongside this new business approach.

Globant also expanded partnerships with major technology providers as part of its AI-focused push.

For you as an investor, Globant sits at the intersection of software services, AI and digital transformation work for large enterprises. The move toward AI-native Pods ties directly into how many companies now want modular, outcome focused teams rather than traditional project structures. That puts execution front and center, with subscription style relationships that can be easier for clients to plan around.

Record revenue and free cash flow, combined with deeper ties to large tech partners, mark an important phase in how Globant is positioning NYSE:GLOB. The key questions from here will likely center on how quickly clients adopt the Pods model and how recurring those subscriptions become over time. Expanded alliances with big technology providers may also influence where new demand comes from and how resilient that demand is across different sectors.

Stay updated on the most important news stories for Globant by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Globant.

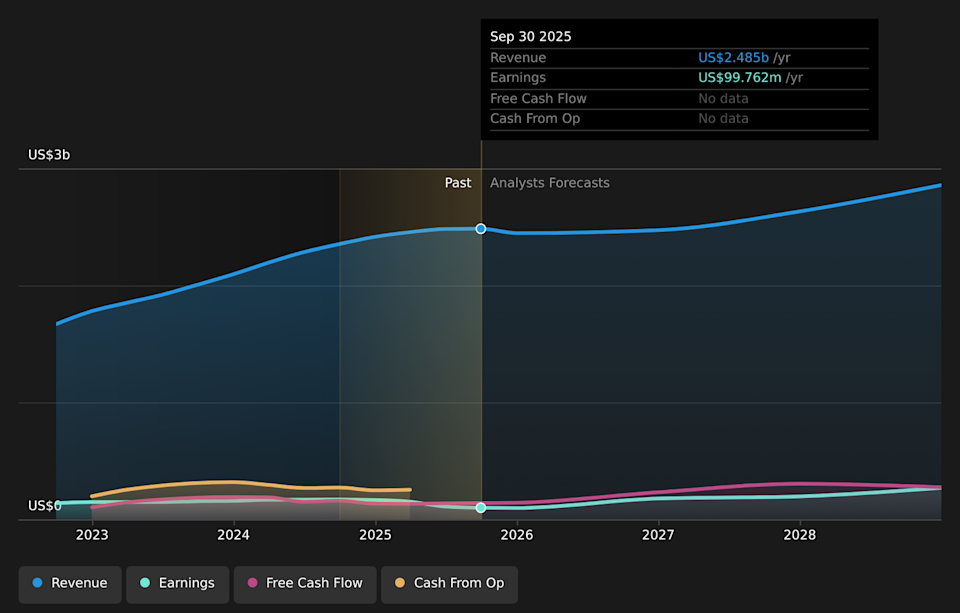

NYSE:GLOB Earnings & Revenue Growth as at Feb 2026

NYSE:GLOB Earnings & Revenue Growth as at Feb 2026

📰 Beyond the headline: 2 risks and 2 things going right for Globant that every investor should see.

The move to AI-native Pods comes as Globant reports mixed earnings trends, which gives you useful context for assessing the opportunity. Quarterly sales were US$612.47m compared to US$642.48m a year earlier, while net income for the quarter was US$41.56m compared to US$38.41m. For 2025 as a whole, sales were US$2,454.88m compared to US$2,415.69m, but net income for the year was US$102.92m compared to US$165.73m. So, the company is talking about record revenue and free cash flow against a backdrop of pressured profitability over the full year.

The AI-native Pods subscription model directly ties into the narrative that outcome-based, recurring AI work could support higher-margin, recurring revenues over time, especially as Globant deepens partnerships with Nvidia, OpenAI, AWS, Microsoft, Google and others.

At the same time, the modest full-year revenue progression and lower net income compared to the prior year highlight the demand softness and margin pressure that analysts have already flagged as risks to sustained growth.

The focus on record free cash flow and a US$3.4b pipeline of AI Pods work adds a cash generation and backlog angle that is only partly reflected in the existing narrative around efficiency measures and subscription-based engagements.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Globant to help decide what it’s worth to you.

⚠️ Profit margins for the latest year were 4.2% compared to 6.9% previously, so profitability is under pressure even as the company talks about record revenue and free cash flow.

⚠️ Large one off items have affected financial results, which can make it harder for you to judge the underlying earnings power of the business during this transition.

🎁 Globant is trading at a level Simply Wall St’s model views as 51.1% below its estimate of fair value. Some investors may see this as room for upside if execution on AI Pods and partnerships goes to plan.

🎁 Earnings are forecast in that same model to grow 21.56% per year. If achieved, this would support the case that AI-driven and subscription-based work can reshape the profit profile.

From here, you will probably want to track how quickly clients adopt the AI-native Pods model, how much of revenue becomes subscription-based and how that feeds into margins. Compare Globant’s progress with peers such as Accenture, EPAM and Cognizant, which are also pushing AI-powered services. The 2026 guidance, which points to flat to low-single-digit revenue growth and specific EPS ranges, gives you clear markers to measure management against. Any updates on the US$3.4b Pods pipeline, free cash flow trends and the depth of work coming through partners like Nvidia, OpenAI and major cloud providers will help you gauge whether this model shift is starting to show through in more stable growth and profitability.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Globant, head to the community page for Globant to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include GLOB.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com