OC Oerlikon (SWX:OERL) has drawn fresh attention after reporting a full year 2025 net loss of CHF 19 million, while its board proposed a total dividend of CHF 0.85 per share, including a one time extraordinary payout.

See our latest analysis for OC Oerlikon.

At a share price of CHF4.23, OC Oerlikon has seen strong short term momentum, with a 30 day share price return of 18.16% and a 90 day share price return of 33.95%, even though the 5 year total shareholder return of 46.83% loss shows a much weaker longer term picture.

If this dividend news has you rethinking where you look for opportunities, it could be a good moment to broaden your search with our 96 top founder-led companies.

With a recent rally, an extraordinary dividend and an intrinsic value estimate suggesting a discount of about 19%, OC Oerlikon sits at an interesting crossroads. Is this a genuine value opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 13.7% Overvalued

With OC Oerlikon last closing at CHF4.23 against a widely followed fair value estimate of CHF3.72, the current price sits above that narrative line and puts extra focus on what assumptions are doing the heavy lifting.

Oerlikon’s continued strategic focus on advanced surface solutions for electrification, e-mobility, aviation, and energy-efficient manufacturing positions the company to benefit from growing demand arising as manufacturers invest in next-generation batteries, lightweight automotive components, and more sustainable industrial processes, supporting higher medium-term revenue growth and improved order backlog.

Curious what kind of revenue path and margin rebuild need to line up to justify that fair value, and how a single discount rate ties it together, and what profit multiple underpins the whole story? The full narrative lays out those moving parts in black and white.

Result: Fair Value of CHF3.72 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, there are still clear pressure points, including revenue tied to early cyclical industrial demand and the risk that past write downs signal weaker long term product potential.

Find out about the key risks to this OC Oerlikon narrative.

Another View: Cash Flows Point a Different Way

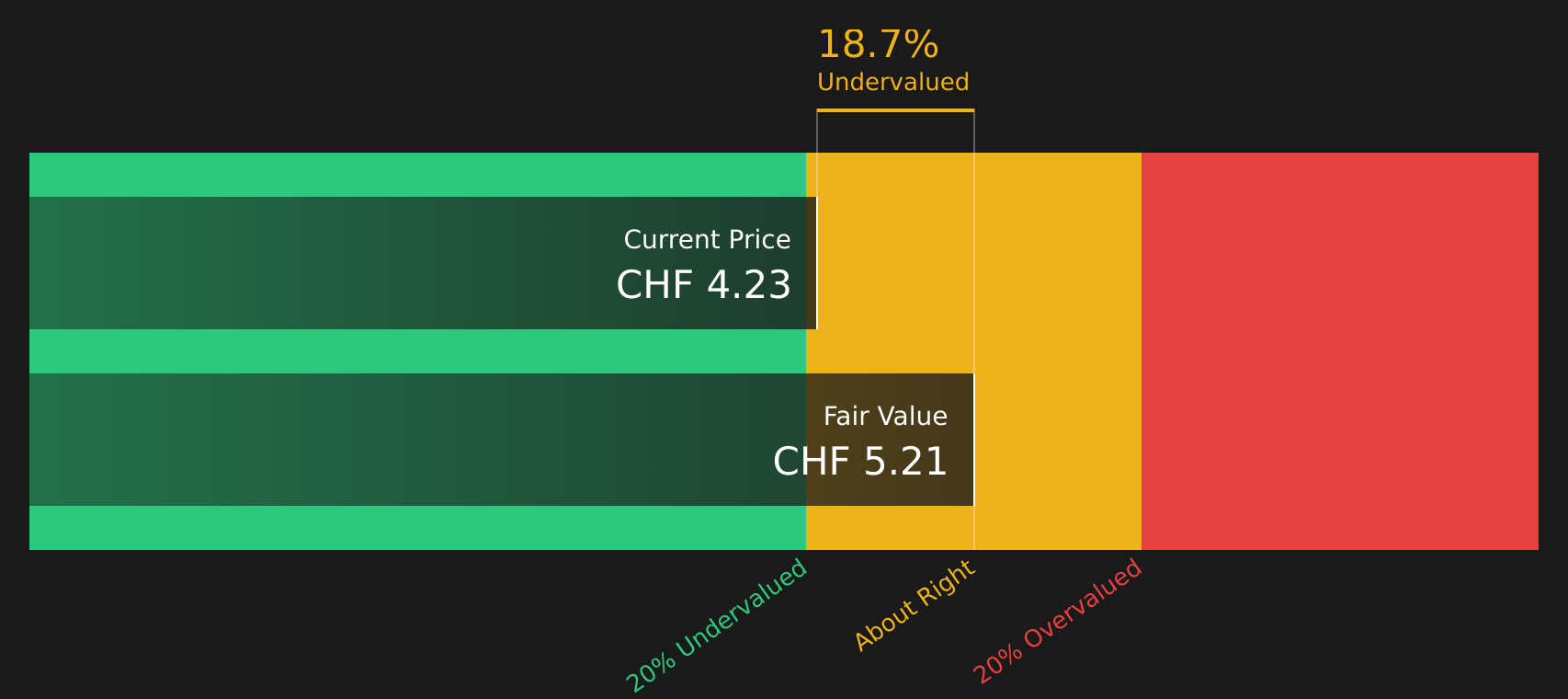

While the popular narrative flags OC Oerlikon as about 13.7% overvalued at CHF4.23 versus a CHF3.72 fair value, our DCF model lands in a different place, with a fair value estimate of CHF5.21 and the shares trading at an 18.7% discount. Same company, very different story.

That split between earnings based targets and cash flow based value raises a simple question for you: which lens do you trust more when profit today and profit tomorrow are pulling in opposite directions?

Look into how the SWS DCF model arrives at its fair value.

OERL Discounted Cash Flow as at Feb 2026

OERL Discounted Cash Flow as at Feb 2026

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out OC Oerlikon for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 220 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

With mixed signals on value, income, and recent price moves, it makes sense to look at the full picture yourself and not just the headline takeaways. If you want to weigh the concerns against the potential upside, a good next step is to review the 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If this story has sharpened your thinking, do not stop here. Use the screener to line up fresh ideas that match what you care about most.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com