Make better investment decisions with Simply Wall St’s easy, visual tools that give you a competitive edge.

If you are wondering whether Millrose Properties is still attractively priced or has already run ahead of itself, the recent share performance gives some useful clues before we get into the valuation work.

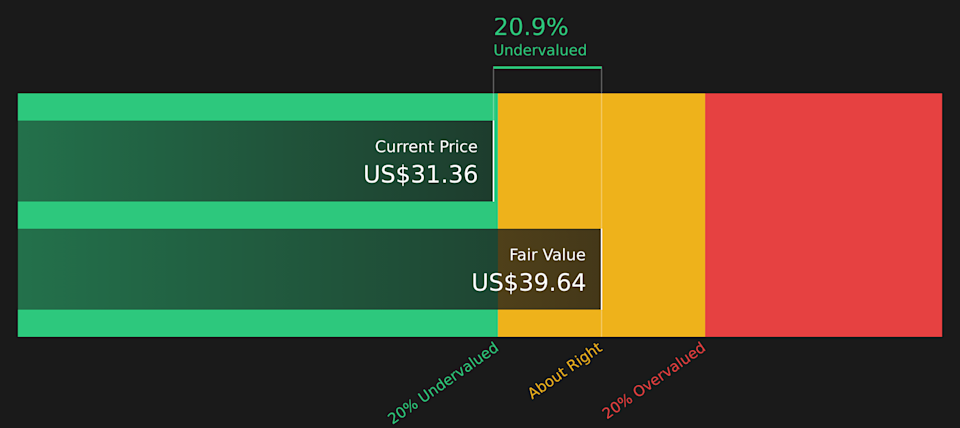

The stock last closed at US$31.36, with returns of 1.0% over the past week, 5.2% over the past month and 49.6% over the past year. This naturally raises questions about how much of the story is already reflected in the price.

Recent coverage has focused on Millrose Properties as a real estate name that continues to attract investor interest, with attention on how its portfolio and market positioning stack up against peers. This context helps explain why the share price has been active and sets up an important question around whether the current valuation still looks reasonable.

On our checks, Millrose Properties scores a full 6 out of 6 for being undervalued. Next, we will walk through the standard valuation approaches investors often rely on and then finish with a broader way to think about what that score really means for you.

The Dividend Discount Model looks at a stock through the lens of the cash dividends you might receive in the future, then adds them up in today’s dollars. It is essentially asking what Millrose Properties could be worth if you value it purely on the stream of dividends.

For Millrose Properties, the model uses a current dividend per share of about US$3.15. The company currently has a payout ratio of 106.61%, which means it is paying out more in dividends than it generates in earnings. Based on the inputs provided, this leads to an extremely low implied long term dividend growth rate of about 0.05%, calculated from the combination of payout ratio and return on equity.

Plugging these dividend assumptions into the DDM yields an estimated intrinsic value of around US$39.64 per share. Compared with the recent share price of US$31.36, this points to an implied discount of 20.9%. On this dividend based lens, the shares screen as undervalued.

Result: UNDERVALUED

Our Dividend Discount Model (DDM) analysis suggests Millrose Properties is undervalued by 20.9%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

MRP Discounted Cash Flow as at Mar 2026

MRP Discounted Cash Flow as at Mar 2026

For profitable companies, the P/E ratio is a useful shorthand because it ties what you pay for the stock directly to the earnings it generates. It gives you a quick sense of how many dollars investors are currently willing to pay for each dollar of earnings.

What counts as a “normal” or “fair” P/E depends on what investors expect for future growth and how risky they think those earnings are. Higher growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk usually leads to a lower one.

Millrose Properties currently trades on a P/E of 12.86x. That sits below the Specialized REITs industry average of 15.86x and also below the peer group average of 24.00x. This suggests the market is assigning a lower multiple than many of its comparables.

Simply Wall St’s Fair Ratio for Millrose Properties is 37.70x. This is a proprietary estimate of what the P/E could be given factors such as earnings growth, profit margins, industry, market cap and company specific risks. Because it adjusts for these elements, it can be more tailored than a simple comparison with industry or peer averages.

Set against the current P/E of 12.86x, the Fair Ratio of 37.70x indicates that, on this metric, the stock screens as undervalued.

Result: UNDERVALUED

NYSE:MRP P/E Ratio as at Mar 2026

NYSE:MRP P/E Ratio as at Mar 2026

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply your own story about Millrose Properties that connects what the business is doing to a financial forecast, and then to a fair value you can compare with today’s share price.

On Simply Wall St’s Community page, Narratives let you plug in your assumptions for Millrose’s future revenue, earnings, margins and fair value, then see how your view stacks up against others on the platform.

Because these Narratives update when new information like news or earnings is added, they provide a living framework to decide whether the current price looks attractive, stretched or somewhere in between.

For example, one investor might build a Narrative that aligns closely with the US$38.60 consensus fair value and expected 2028 revenue of about US$1.1b and earnings of US$685.3m. Another investor might be far more conservative and use much lower revenue, margin and valuation assumptions. This shows in one place how different stories about Millrose can lead to very different views on whether to buy, hold or sell.

Do you think there’s more to the story for Millrose Properties? Head over to our Community to see what others are saying!

NYSE:MRP 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include MRP.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com