Get insights on thousands of stocks from the global community of over 7 million individual investors at Simply Wall St.

If you are wondering whether Organon’s current share price reflects its true worth, this article will walk through what the numbers actually say about the stock’s value.

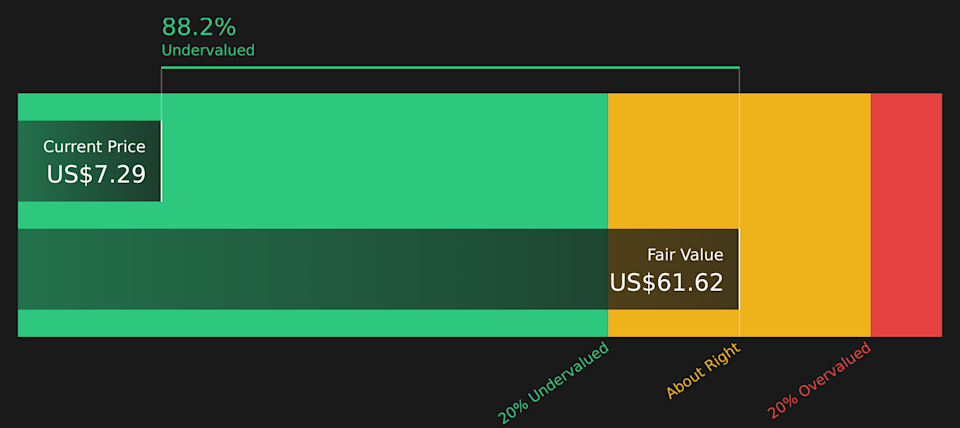

Organon last closed at US$7.29, with returns over the past week, month and year of 10% decline, 14.6% decline and 50.6% decline respectively, while the year to date return sits at 0.7%.

These moves have come as investors react to ongoing headlines around Organon’s role in the broader pharmaceuticals and biotech space and its positioning as a standalone company after prior corporate actions. Taken together, these themes have kept attention on whether the current share price properly reflects its asset base and long term prospects.

Right now, Organon scores a 5 out of 6 valuation score, which suggests it screens as undervalued on most of the key checks we will walk through next. We will also touch on an even more holistic way to think about valuation at the end of the article.

Find out why Organon’s -50.6% return over the last year is lagging behind its peers.

A Discounted Cash Flow, or DCF, model takes projected future cash flows and discounts them back to today to estimate what the business might be worth right now.

For Organon, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about $394.5 million. Analyst estimates extend out to 2030, with projected Free Cash Flow of $1,346 million in that year, and Simply Wall St extrapolates further out to 2035 using gradually moderating growth assumptions.

After discounting these future cash flows back to today, the DCF model arrives at an estimated intrinsic value of about $65.70 per share. Compared to the recent share price of US$7.29, this implies Organon screens as around 88.9% undervalued on this model.

This is a single model and depends heavily on the long term cash flow assumptions. However, it points to a wide gap between price and estimated value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Organon is undervalued by 88.9%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

OGN Discounted Cash Flow as at Mar 2026

OGN Discounted Cash Flow as at Mar 2026

For a profitable business like Organon, the P/E ratio is a useful way to relate what you pay for each share to the earnings the company is already generating. It gives you a quick sense of how much the market is paying per dollar of profit.

What counts as a “normal” or “fair” P/E usually reflects two things: how quickly earnings are expected to grow and how risky those earnings are. Higher growth or perceived stability often justify a higher P/E, while slower growth or higher risk usually align with a lower P/E.

Organon currently trades on a P/E of 10.15x. That sits below the Pharmaceuticals industry average of 20.02x and below the peer group average of 15.47x. Simply Wall St also calculates a proprietary “Fair Ratio” of 24.51x for Organon, which is the P/E level suggested by factors such as its earnings profile, industry, profit margins, market cap and risk characteristics.

This Fair Ratio can be more informative than a simple industry or peer comparison because it adjusts for Organon’s own growth outlook, risk and profitability rather than assuming all companies deserve the same multiple.

With a Fair Ratio of 24.51x versus the current 10.15x P/E, Organon screens as undervalued on this metric.

Result: UNDERVALUED

NYSE:OGN P/E Ratio as at Mar 2026

NYSE:OGN P/E Ratio as at Mar 2026

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These are simply your story about Organon linked directly to numbers like fair value, future revenue, earnings and margins, then compared with today’s share price.

On Simply Wall St’s Community page, Narratives let you set out what you think Organon’s future looks like, connect that view to a forecast, and see what fair value that story implies. This is all presented in an easy format used by millions of other investors.

Because Narratives update automatically when new information comes in, such as Organon’s earnings guidance of about US$6.2b for 2026 or reports of a nonbinding all cash offer from Sun Pharmaceutical Industries, your story and fair value stay current without you needing to rebuild a model from scratch.

For Organon today, one investor might lean toward a higher view of value, around US$12 per share, based on expectations of steady revenue, margins near 13% and a future P/E a little under 5x. Another might focus on governance concerns and softer guidance, and align with a lower fair value closer to US$5. Those two Narratives frame very different decisions when they compare their Fair Value to the current price.

For Organon, here are previews of two leading Organon narratives:

🐂 Organon Bull Case

Fair value in this narrative: US$9.36 per share

Price gap to this fair value: Organon trades at about 22.2% below this narrative fair value based on the last close of US$7.29

Revenue growth assumption: 4.13% a year

Analysts in this camp see new product launches, biosimilars and margin improvement supporting earnings, while still flagging risks from legacy products, pricing pressure and a lighter internal pipeline.

The numbers behind this view include revenue of about US$6.5b and earnings of about US$990.3m by 2028, with margins rising from 11.1% to 15.2% and a future P/E of 4.7x.

This narrative lines up with a consensus price target of US$13.17, with a wider range from US$9.00 to US$18.00, and uses a 9.4% discount rate to bring those future cash flows back to today.

🐻 Organon Bear Case

Fair value in this narrative: US$5.00 per share

Price gap to this fair value: Organon trades at about 45.8% above this narrative fair value based on the last close of US$7.29

Revenue growth assumption: 1.85% annual contraction

The more cautious view focuses on pricing pressure, loss of exclusivity, weaker internal innovation, higher debt and regulatory risks, with concerns around internal controls and earnings quality.

Here, bearish analysts assume roughly flat to slightly lower revenues at about US$6.3b by 2028, earnings of about US$1.0b, higher profit margins of 16.6%, but a much lower future P/E of 3.0x.

This group works with a reduced price target around US$5.00, uses a 9.4% discount rate and assumes the market applies a steeper discount to Organon because of governance, policy and execution risks.

If you want to go deeper than these previews and see how each storyline links through to detailed numbers, you can review the full bull and bear cases for Organon using Curious how numbers become stories that shape markets? Explore Community Narratives.

Do you think there’s more to the story for Organon? Head over to our Community to see what others are saying!

NYSE:OGN 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include OGN.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com