Track your investments for FREE with Simply Wall St, the portfolio command center trusted by over 7 million individual investors worldwide.

If you are wondering whether GXO Logistics is fairly priced or offering value at its current level, you are not alone. This article will walk through the key clues in the valuation picture.

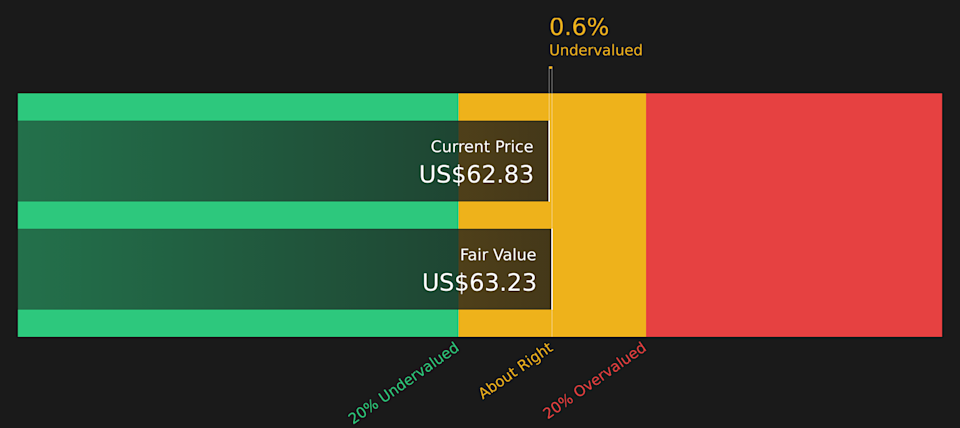

The stock closed at US$62.83, with a 4.2% decline over 7 days, 11.0% over 30 days, 15.7% year to date and 59.4% over 1 year. This naturally raises questions about how much optimism or risk is now reflected in the price.

Recent news coverage has focused on GXO Logistics as a pure play contract logistics provider and how it fits into long term outsourcing and supply chain trends. This helps frame these share price moves. Investors are paying close attention to how these themes could influence expectations around volumes, efficiency and customer demand over time.

On our valuation checks, GXO Logistics currently scores 4 out of 6. Next we will look at what different valuation methods say about that score, before finishing with a broader way to think about what value really means for this stock.

A Discounted Cash Flow, or DCF, model estimates what a business could be worth by projecting its future cash flows and discounting them back to today using a required rate of return. It is essentially asking what all those future dollars are worth in today’s terms.

For GXO Logistics, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The company’s last twelve month free cash flow is about $70.2 million. Analyst estimates and extrapolations then step this forward, with projected free cash flow rising to $617.8 million in 2035. Simply Wall St uses analyst inputs up to around 5 years, and then extends the trend for the remaining years in the 10 year projection period.

Putting all of those projected cash flows together and discounting them back gives an estimated intrinsic value of about $63.23 per share. Against the recent share price of $62.83, that implies the stock is around 0.6% undervalued, which is effectively in the margin of error for this kind of model.

Result: ABOUT RIGHT

GXO Logistics is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment’s notice. Track the value in your watchlist or portfolio and be alerted on when to act.

GXO Discounted Cash Flow as at Mar 2026

GXO Discounted Cash Flow as at Mar 2026

For companies where revenue is a key reference point, the P/S ratio is a useful way to think about value because it links the share price directly to the sales the business is generating today.

What investors are willing to pay on a P/S basis often reflects a mix of growth expectations and perceived risk. Higher expected growth or lower perceived risk can support a higher “normal” P/S multiple, while slower expected growth or higher uncertainty usually pulls that multiple down.

GXO Logistics currently trades on a P/S of 0.55x, compared with the Logistics industry average of 0.84x and a peer group average of 1.62x. On the surface, that points to a lower valuation than those simple benchmarks.

Simply Wall St’s Fair Ratio is designed to go a step further. It estimates what a more tailored P/S multiple could look like after considering factors such as earnings growth, profit margins, industry, market cap and company specific risks. Because it adjusts for these elements, it can give a more rounded view than a straight comparison with peers or the broad industry.

For GXO Logistics, the Fair Ratio is 1.00x, which is higher than the current P/S of 0.55x. This suggests the shares may be trading below that model based reference point.

Result: UNDERVALUED

NYSE:GXO P/S Ratio as at Mar 2026

NYSE:GXO P/S Ratio as at Mar 2026

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Earlier we mentioned that there is an even better way to understand valuation. Narratives let you turn your view on GXO Logistics into a clear story that links what you think about its contracts, automation plans and sector position to a set of revenue, earnings and margin estimates. These then roll up into a Fair Value you can compare with the current price on the Simply Wall St Community page. This updates automatically as new earnings or news arrive, and you can see it side by side with other users’ views, such as a higher fair value around US$85.09 at the optimistic end or closer to US$44.61 at the cautious end, so you can judge where your own story fits in that range.

For GXO Logistics, however, we will make it really easy for you with previews of two leading GXO Logistics Narratives:

🐂 GXO Logistics Bull Case

Fair value in this bullish narrative: US$85.09 per share

Implied discount to this fair value: about 26.2% undervalued versus the recent US$62.83 close

Revenue growth assumption in this view: 6.57% a year

Analysts in this camp focus on demand for outsourced logistics and complex e commerce fulfillment, supported by a growing sales pipeline and multi year contracts.

They highlight investments in automation, AI and technology that are expected to improve productivity, margins and earnings over time.

This view leans on GXO’s global scale, entry into sectors like healthcare and aerospace, and alignment with themes such as ESG requirements and supply chain resilience.

🐻 GXO Logistics Bear Case

Fair value in this cautious narrative: US$58.96 per share

Implied premium to this fair value: about 6.6% overvalued versus the recent US$62.83 close

Revenue growth assumption in this view: 5.49% a year

Analysts on this side point to customer capacity changes, start up timing and integration work that could pressure EBITDA and margins.

They see near term risks around the Wincanton acquisition, higher investment in AI and automation, and cost pressures in complex supply chains.

This narrative also factors in regulatory reviews, economic uncertainty and uneven consumer demand that could affect contract ramp up, free cash flow and the valuation multiple.

Do you think there’s more to the story for GXO Logistics? Head over to our Community to see what others are saying!

NYSE:GXO 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include GXO.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com