For Mr Yoshikawa, 2026 marks his seventh year as an entrepreneur in China. It is also the year he and his wife welcomed their first child in Shenzhen.

“Sometimes, I feel a deep sense of uncertainty,” Yoshikawa told me. Like many Japanese entrepreneurs in China, he finds himself living between two sharply different realities, trying to make sense of both at once.

Politically and militarily, Japan confronts China with its toughest stance yet. Economically and technologically, however, Japanese firms continue to deepen their ties with China.

An investment boom on the edge of a Cold War

For China–Japan relations, 2026 feels like a strange moment, perhaps the worst of times, and the best.

Japan’s Prime Minister Sanae Takaichi won a landslide victory in the snap election of 8 February, a move she framed as a way to consolidate support for a tougher foreign policy after declaring that a Chinese military threat to Taiwan would prompt a Japanese response, even after that position had been heavily criticised by Beijing.

As Beijing increasingly uses trade pressure and military signalling to push back against Tokyo, including restrictions on rare earth exports, the relationship between the two countries is entering a new phase. In 2026, it looks less like uneasy cooperation and more like the early stage of a new Cold War.

And yet, the data tells a far more confusing story. At a time when Tokyo and Beijing appear to be drifting further apart politically, Japanese capital is moving in the opposite direction.

Despite diplomatic relations sinking to a new low, figures from China’s Ministry of Commerce show that Japanese foreign direct investment (FDI) into China surged by 55.5% year-on-year in the first three quarters of 2025. This spike stands in stark contrast to China’s broader investment downturn. In 2025, China’s total utilised FDI (that is, foreign investment that has actually been made rather than just planned or promised) fell to 747.77 billion yuan, down 9.5% from the previous year, marking the third consecutive annual decline.

The popular narrative of “foreign capital fleeing China,” however, only tells part of the story. While total investment value dropped, the number of newly established foreign-invested enterprises reached 70,392, up 19.1% year-on-year. Japan was not an exception. Swiss investment in China jumped 66.8%, British investment rose 15.9%, and the United Arab Emirates recorded 27.3% growth, driven largely by its interest in green energy and the digital economy.

Behind these numbers lies a more calculated shift in Beijing’s thinking: a move away from growth-first logic toward a strategy where security comes first.

Countries like the UK and Switzerland, both global offshore financial hubs, are emerging as indirect gateways for China to access Western capital and technology.

With the launch of China’s 2026–30 Five-Year Plan, technological development has been redefined as a matter of national survival. Beijing is now pursuing what it calls “targeted openness”. Manufacturing is broadly opened, while foreign capital is selectively steered toward sectors such as AI, electric vehicles, and digital services.

China is increasingly positioning itself as a testing ground where advanced energy systems and data-driven technologies converge. By anchoring Japanese and European technologies inside its system, Beijing hopes to ensure that any future sanctions against China would face strong resistance from domestic interest groups in those economies.

Chinese policymakers appear convinced that, even with tighter regulations and the chilling effect of its Anti-Espionage Law, multinational companies will not be able to walk away from China’s market. Takaichi seems well aware of this reality. Having achieved her historic general election victory, she will likely argue that Japan is no longer simply following Washington’s lead but is instead emerging as a rule-setter in the Indo-Pacific.

From “the world’s factory” to embedded survival

This paradox is not abstract. It is already reshaping how businesses operate on the ground. Yoshikawa’s personal story captures this shift.

He first came to China in 2011, when the Japanese expatriate population there peaked at around 150,000. At the time, China was still widely seen as “the world’s factory,” and Yoshikawa was convinced its potential was limitless. He moved to Beijing and immersed himself in studying Mandarin.

That same year, however, tensions over the contested Senkaku/Diaoyu Islands erupted. Beijing imposed rare earth export restrictions on Japan, and China–Japan relations never truly recovered.

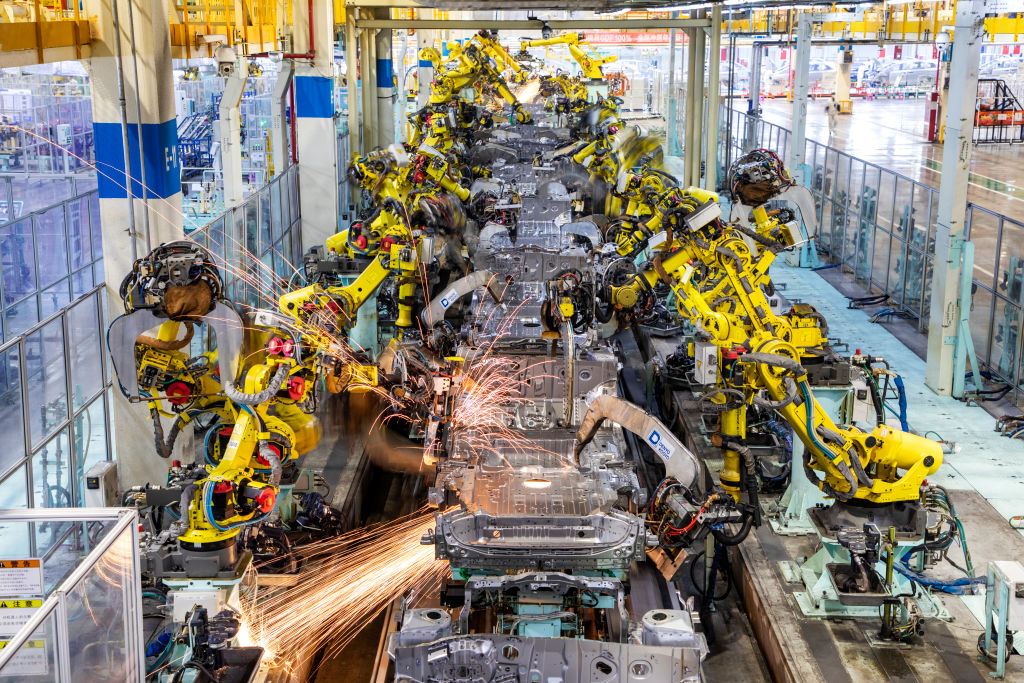

In 2019, Yoshikawa settled in Shenzhen. He initially imported Japanese consumer goods into China. But as China’s automation capacity rapidly expanded, he pivoted toward exporting semi-finished Chinese products overseas. Then came the pandemic, and with it, a painful global supply-chain restructuring.

By 2026, the number of Japanese nationals living in China had fallen to below 100,000. Yoshikawa’s company now develops AI-powered toys and health wearables, and his business is fully embedded in China’s export supply chain. His products are sold not only back to Japan but across Southeast Asia.

“We’re no longer doing business for the China market,” Yoshikawa said. “We’ve become part of China’s supply chain.”

Third-country channels and the rise of “technology custody”

Small and medium-sized businesses are not the only ones staying. Japan’s industrial giants are doing the same.

Despite rising political tensions, major Japanese firms are increasingly adopting an “In China, for China” strategy. Japan is a member of the RCEP, the world’s largest free trade agreement, which enables member states to trade and invest more freely within its framework. Now, Japan is leveraging these benefits by investing heavily in high-end manufacturing and R&D within China, its largest trading partner. Honda, for example, announced a deep partnership in 2025 with Momenta, a leading Chinese autonomous-driving company. Japanese automakers understand that in the age of electrification and intelligent vehicles, walking away from China’s R&D ecosystem risks global marginalisation.

More intriguing, however, may be the rise of “third-country channels.” Countries like the UK and Switzerland, both global offshore financial hubs, are emerging as indirect gateways for China to access Western capital and technology. Saudi Arabia, driven by its energy transition agenda, has also begun channeling capital into Chinese technology and new-energy sectors.

“We’re no longer doing business for the China market,” Yoshikawa said. “We’ve become part of China’s supply chain.”

We are already seeing US companies investing in China’s pharmaceutical industry via Saudi Arabia. It is likely that by 2026, more Japanese firms, seeking to hedge against geopolitical risk, will invest in China through subsidiaries or joint ventures based in third countries. What matters here is not where the capital originates, but how it is legally and statistically classified.

As of 2025, China and Switzerland are negotiating an upgrade to their FTA, which officials say could expand cooperation into digital trade and artificial intelligence. Given China’s strategy of channelling foreign investment into specific industries, Switzerland may evolve into a “technology custody centre” in 2026. Foreign investors, such as those from Japan, may establish their Asian R&D headquarters under Swiss entities before forming joint ventures with Chinese partners, giving these investments the legal appearance of neutrality.

At the same time, China and the UK have restarted their economic and financial dialogue. In January 2026, UK Prime Minister Keir Starmer visited Beijing and promoted closer economic ties, including agreements to expand cooperation in services trade and launch a feasibility study toward a potential bilateral services trade agreement. In theory, multinational firms could use London-based financial structures to facilitate investment cooperation with China. Depending on ownership and reporting arrangements, such structures may affect how investments are formally recorded, although this would vary case by case.

In the Middle East, Saudi Arabia’s Vision 2030 offers another potential route for regional economic engagement. Japan and Saudi Arabia have expanded cooperation in energy transition, industrial development, and emerging technologies, including AI. Several Japanese companies have established regional headquarters in Saudi Arabia as part of the kingdom’s investment reforms. As Saudi investment in China continues to grow, such structures could provide Japanese firms with indirect exposure to opportunities linked to China’s latest Five-Year Plan, depending on regulatory and ownership arrangements.

Sanae Takaichi’s victory in Japan’s 2026 election presents Japanese voters with a new model of behaviour with a deliberate division of political and economic strategy. Politically and militarily, Japan confronts China with its toughest stance yet. Economically and technologically, however, Japanese firms continue to deepen their ties with China through joint funds and partnerships based in Saudi Arabia, Switzerland, or the UK. Japan is demonstrating a form of nintai: a capacity to absorb pressure while maintaining economic flexibility. This approach may well become a new template for how the world engages with China.

When I asked Yoshikawa whether he was satisfied with his current situation, he did not answer.

“Do you have plans to leave China?” I asked.

He paused briefly before answering.

“Whatever happens, I will stay.”