Markets have a tendency to downplay shocks when the unexpected happens. In my opinion, there’s a psychological reason for this: if you admit to being surprised, this means you didn’t see something coming, which in markets means you failed. This is why so much market commentary tends to downplay shocks when they happen. It’s almost like saying: “Yes, I missed it, but it’s not a big deal.”

So it was once again yesterday. One analyst, for example, emphasized the fact that yesterday’s rise in oil prices was only the 73rd largest since 1988. I’m not sure how this information is remotely useful, but it sounds an awful lot like you’re explaining away a big miss. Today’s post pushes back on all this. It benchmarks the current shock versus Russia’s invasion of Ukraine four years ago. Russia is a massive oil producer and – at the time – markets worried it would get shut out of the global economy. Yesterday’s spike in oil prices was more than three times as big as the rise on Feb. 24, 2022, the day Russia invaded Ukraine. That’s a big shock no matter how you cut it.

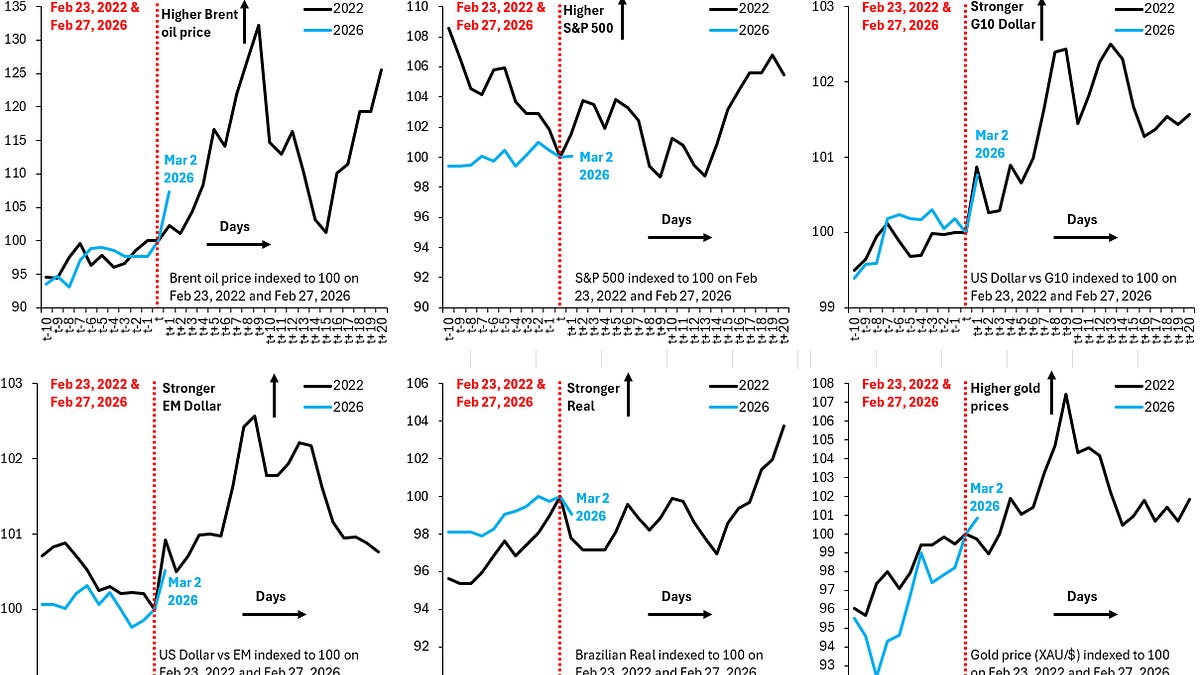

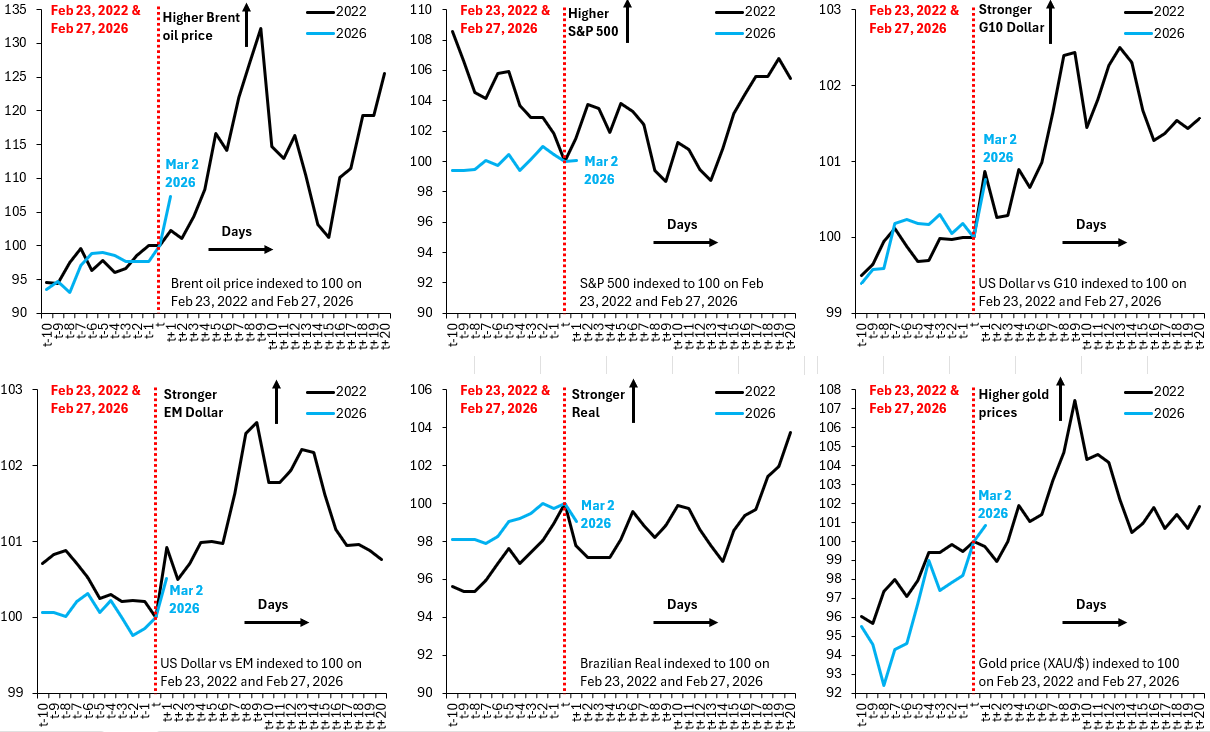

The charts above compare yesterday’s price action to Feb. 24, 2022. Each chart is in event time, with the vertical red line the day before Russia invaded Ukraine (Feb. 23, 2022) and the last trading day before the US attack on Iran (Feb. 27, 2026). The black line in each chart shows price action in the 10 days before and 20 days after invasion. The blue line shows price action now. Both lines are indexed to 100 the day before the shock in question. I look at the Brent oil price (top left), the S&P 500 (top middle), the Dollar versus the rest of the G10 (top right), the Dollar versus emerging markets (EM) on the bottom left, the Brazilian Real versus the Dollar (bottom middle) and the gold price from Bloomberg (bottom right).

Here’s what stands out to me across the six charts:

Yesterday’s rise in oil prices was more than three times as big as when Russia invaded Ukraine: the Brent oil price yesterday rose over seven percent versus two percent back in 2022. Russia produces ten million barrels of oil per day, of which seven million are exported. Twenty million barrels of oil go through the Straits of Hormuz every day. What’s going on now is on a much bigger scale than 2022.

While the S&P 500 was flat yesterday, this is far more cautious than in 2022 when it rose two percent. The rally in the Dollar versus the G10 and versus EM is consistent with that. Markets were in risk-off mode yesterday and were trading Iran like it’s a big shock – not a little one – which is also why gold rallied. Indeed, yesterday’s rally contrasts with Feb. 24, 2022 when gold fell. The “debasement trade” has made gold a more prominent safe haven.

The Brazilian Real weakened yesterday, but it fell far less than in 2022. The Real fell one percent yesterday versus more than two percent the day Russia invaded Ukraine. This is in my opinion a sign markets are already flirting with Brazil as benefitting from war in the Middle East. Back in 2022, after the initial risk-off, it took markets roughly two weeks to realize higher commodity prices are good for Brazil. I expect this realization to hit faster this time around.

The bottom line is that this isn’t a small shock. Markets are trading a big shock, one that can easily get bigger.