Australia faces an unprecedented oil security challenge. Fatih Birol, the executive director of the International Energy Agency (IEA), described the current oil shock as “the largest supply disruption in the history of the global oil market”, and called on countries to act rapidly to reduce economic impacts. While Australia navigated recent oil shocks unscathed thanks to a high self-reliance in oil and oil products, the Iran crisis is markedly different. Domestic oil production only amounts to 5.6% of Australia’s demand today, and our two remaining refineries only provide 17% of our refined petroleum products.

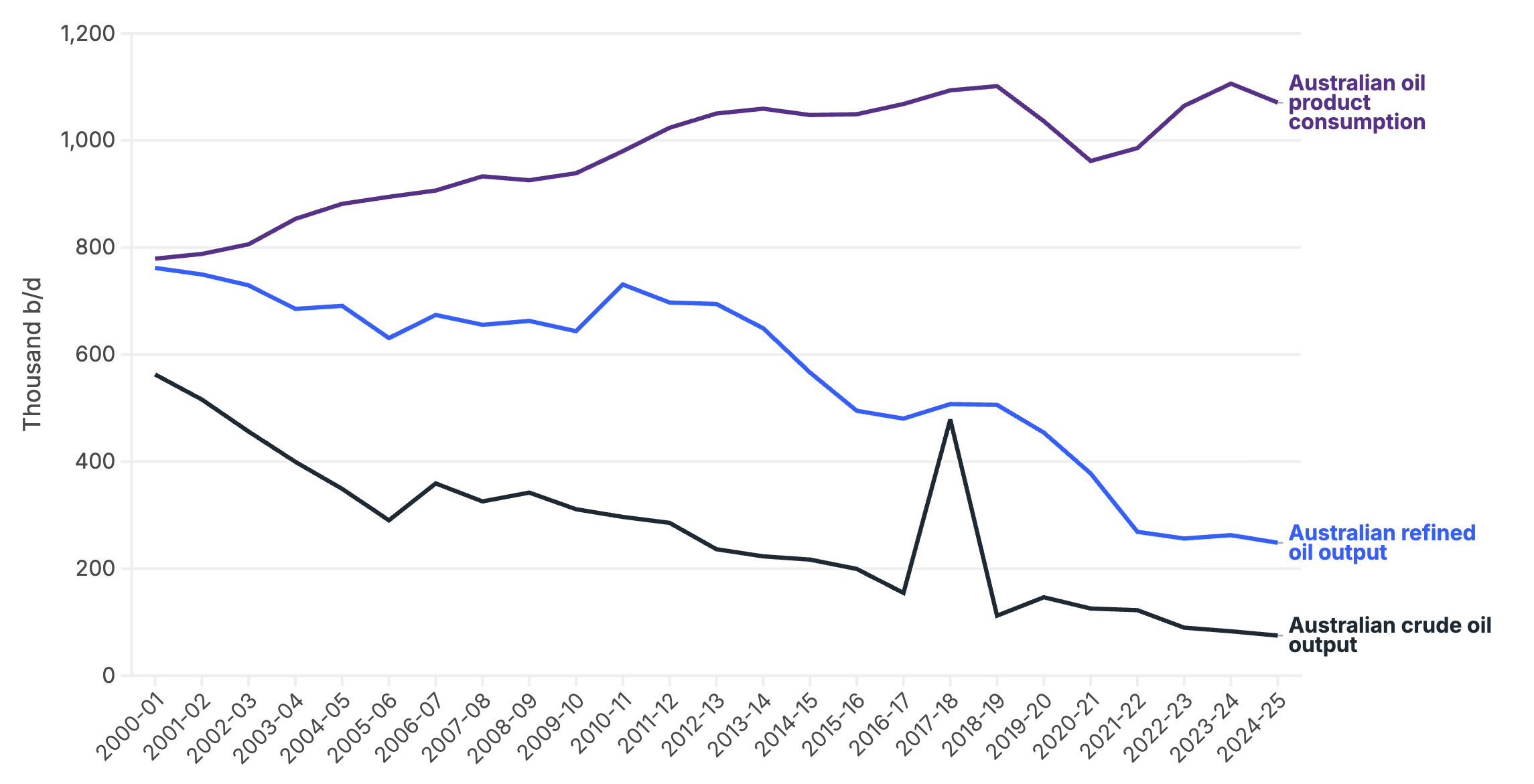

Australian crude oil output, refined oil product output and petroleum sales

Source: DCCEEW: Australian Petroleum Statistics; Australian Energy Statistics.

Australia has the largest trade deficit in refined petroleum products globally, and by quite a margin. The situation is made more precarious by Australia’s very low stockpiles of key petroleum products, with 37 days of petrol and 30 days or less of diesel and jet fuel. Australia has the lowest level of oil stocks of all IEA members – on average major oil importers held 141 days of stocks in December 2025.

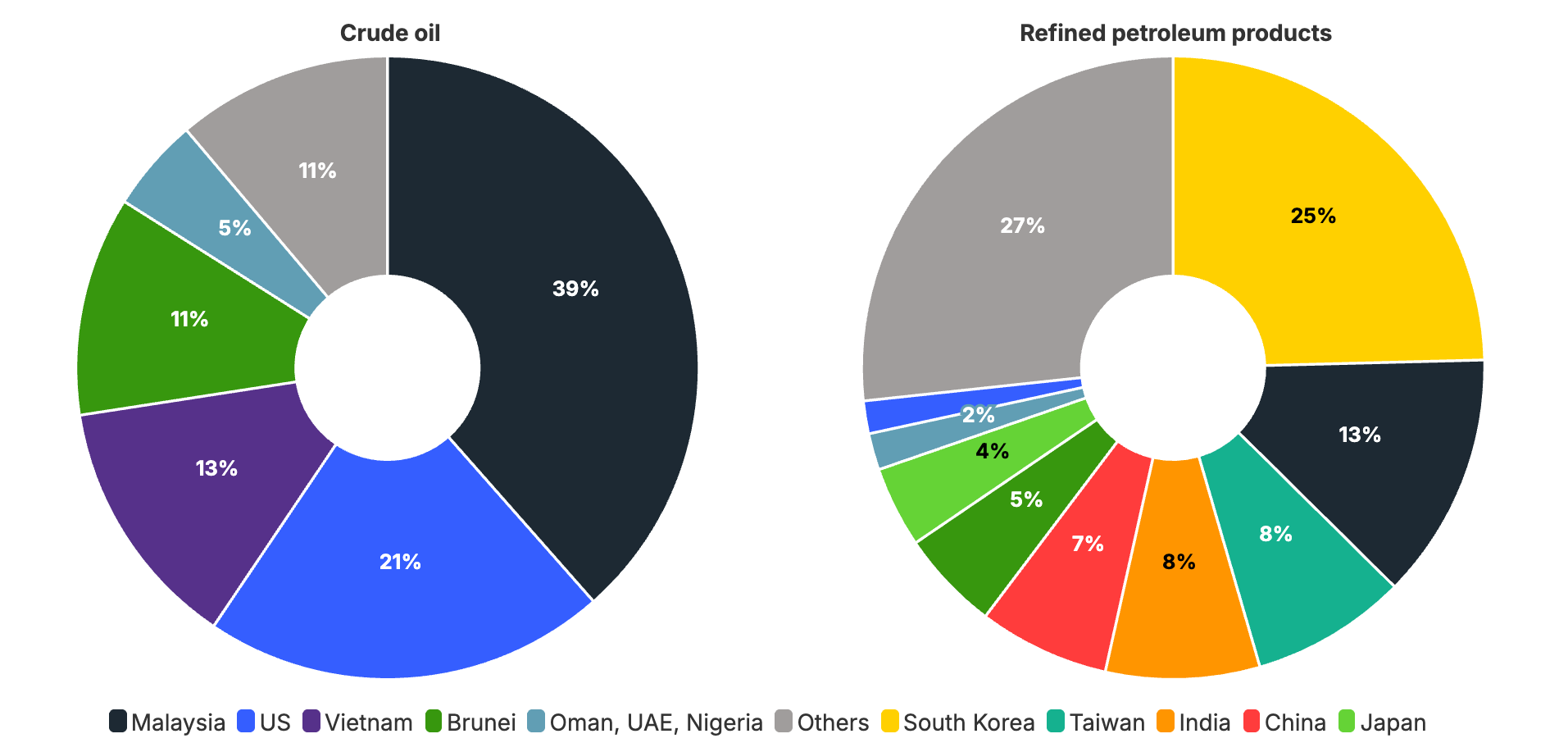

While Australia has limited exposure to the Middle East through its imports of crude oil, it is highly exposed through the Asian refineries that process most of our imports. Some countries, like China, are already restricting exports to prioritise their domestic markets. Several shipments due to arrive in Australia next month have been cancelled or deferred. At this point, they have all been replaced by supply from other regions.

Sources of Australia’s oil imports, 2025

Source: DCCEEW: Australian Petroleum Statistics.

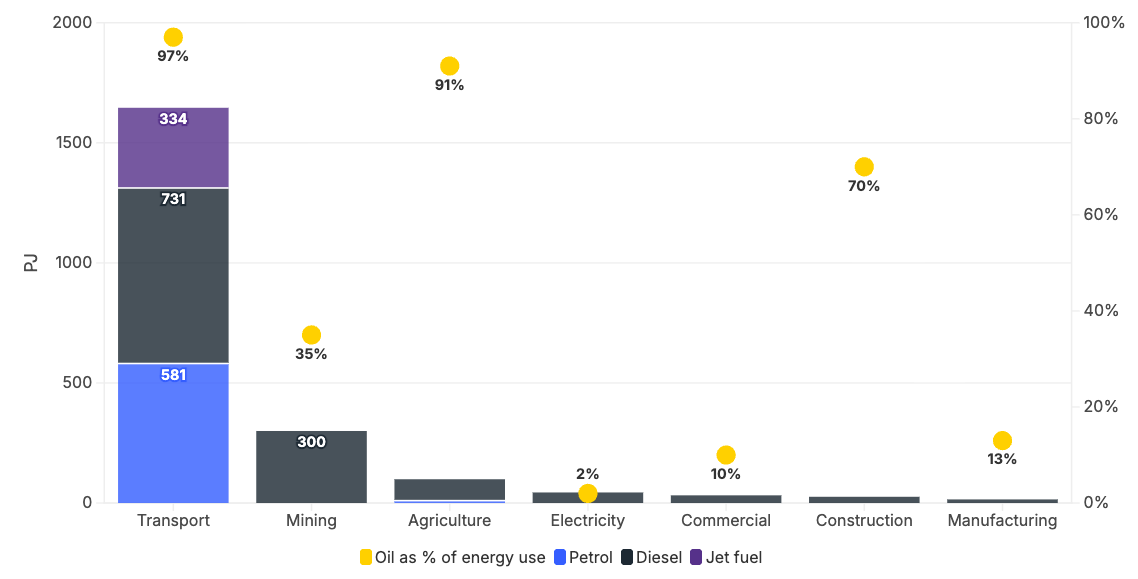

This exposure presents a large economic risk for Australia because oil is our largest energy source and is critical to many of our key economic sectors. There could be serious impacts on our agricultural production, mineral exports, as well as inflation and economic growth. Despite this, successive governments on both sides have repeatedly ignored warnings about the country’s vulnerability.

Use of oil products by sector of Australia’s economy, petajoules (PJ) and % of energy use, FY2023-24

Source: DCCEEW: Australian Energy Statistics. Note: Oil use for petroleum refining was excluded from the data.

Australia does not have many options to address the situation. The government has already implemented a temporary relaxation of fuel specifications to make more fuel available, and started diversifying its suppliers of refined products by increasing imports from the US. It should now take rapid action to curb demand, as recommended by the IEA. This can include voluntary measures, such as working from home and reducing air travel, as well as required changes such as dropping speed limits and imposing driving restrictions. Such measures can make Australia’s stockpiles last longer without material economic impacts.

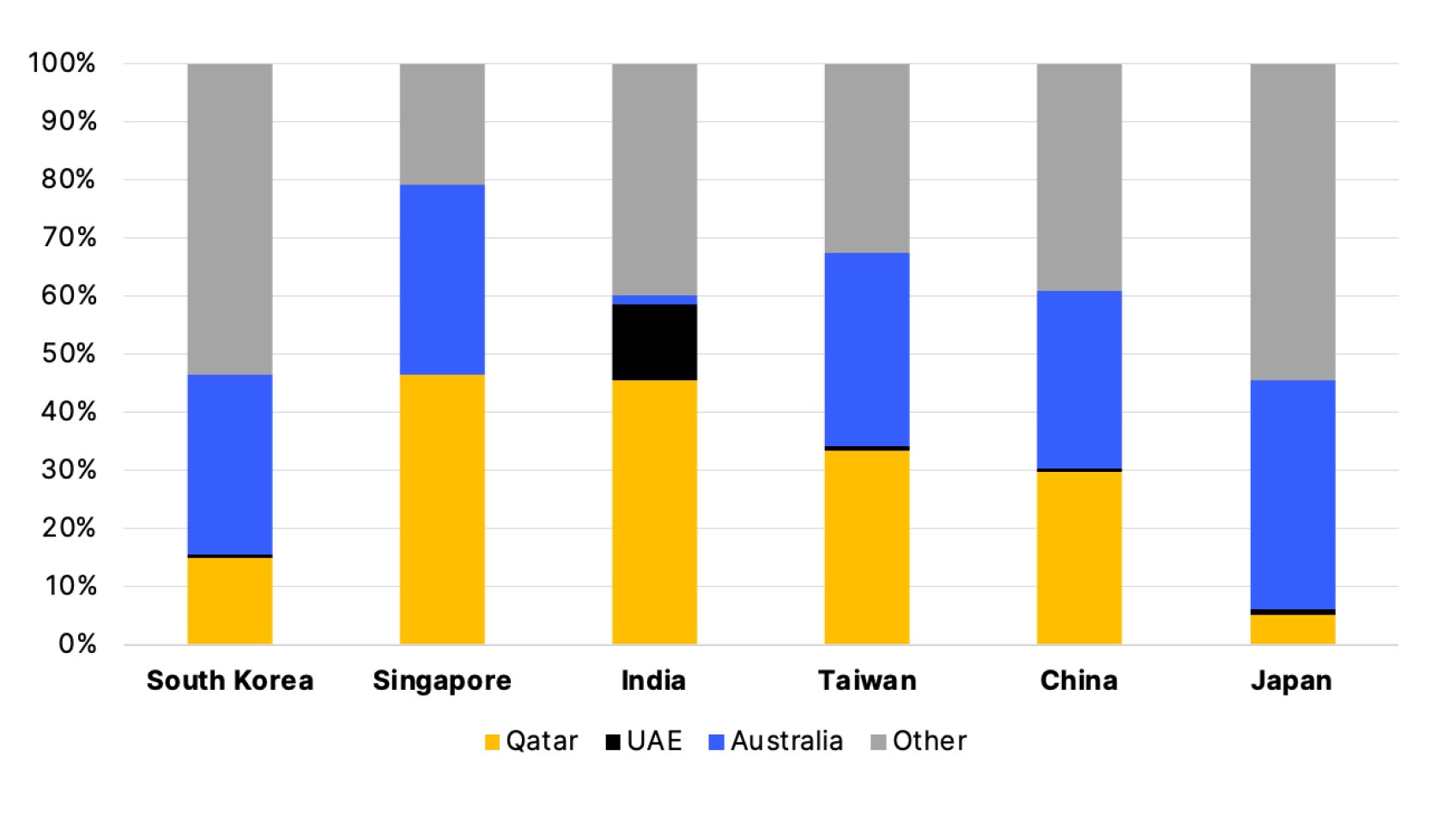

Another lever Australia could explore is to negotiate bilateral crisis supply agreements with our suppliers of refined oil products that are also major importers of liquified natural gas (LNG) with significant exposure to Middle East supplies. Australia may be able to offer priority for spot LNG sales (sales beyond contracted volumes, which made up about a quarter of Australia’s LNG exports in 2024) in exchange for refined oil products. For example, South Korea is a large exporter with high stockpiles, and relies on LNG for over a quarter of its electricity generation.

Source of LNG imports for suppliers of Australian refined oil products

Source: Kpler

The Australian government would need to introduce new export control mechanisms to give it the ability to direct some spot sales to specific countries in times of crisis. Such a mechanism should be based on prevailing market prices to avoid the need to compensate LNG exporters. It could be embedded in an export licensing mechanism as part of the proposed domestic reservation policy.

Increased taxation of coal and gas exports, which are expected to attract elevated prices for the duration of the crisis, could provide funds for cost-relief and fuel-shift measures.

Longer term, Australia has more solutions available to improve its resilience to future oil market shocks, but few can offer protection at scale. Increasing domestic supply is not feasible due to the lack of commercial oil reserves, and increasing stockpiles should be a priority but will take years.

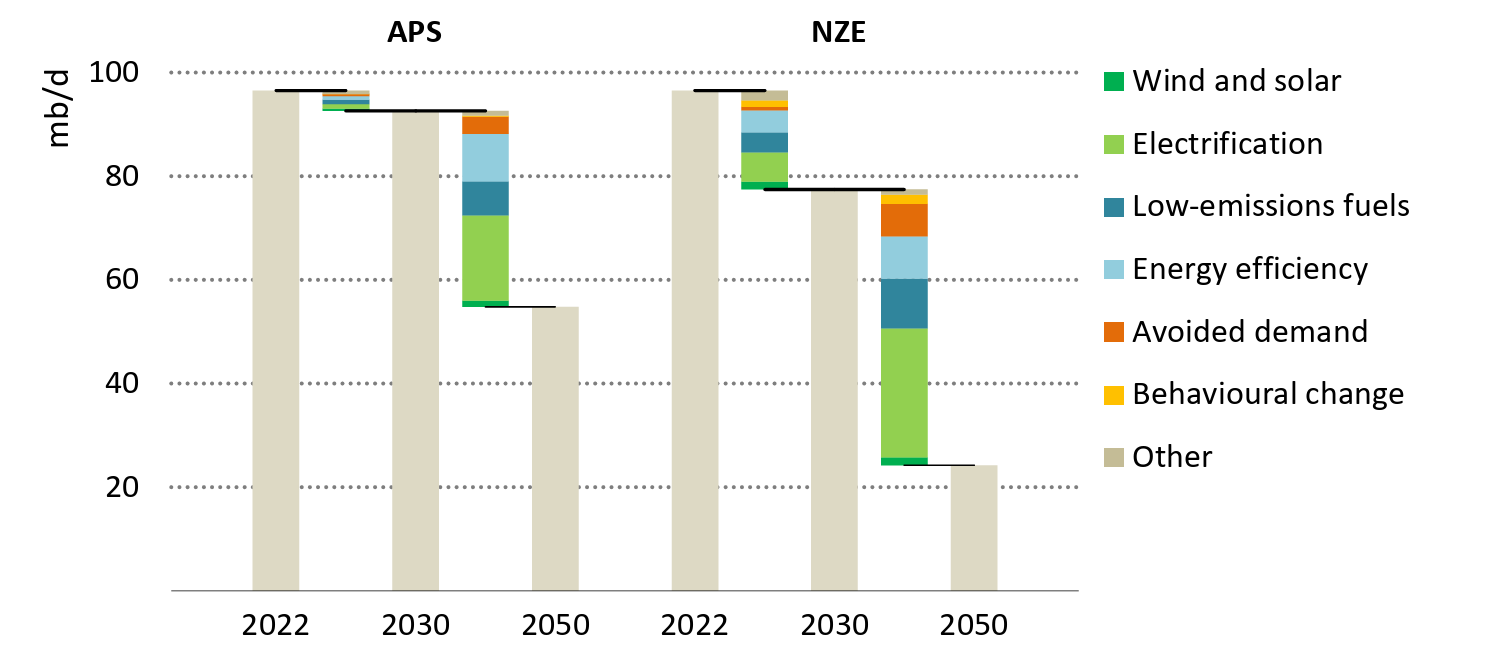

To increase energy security, Australia needs to reduce its dependence on oil throughout the economy. Electrification is the most promising solution as it is mature, cost-effective and can deliver reductions in oil imports at scale, offsetting them with domestically supplied clean energy. The Iran oil shock is the first to happen at a time when renewables and electrification offer a credible alternative.

Key opportunities to reduce oil demand

Source: IEA, Announced Pledges (APS) and Net Zero Emissions (NZE) scenarios. Note: mb/d = millions of barrels per day.

Despite its high oil vulnerability, Australia lags on electric vehicle (EV) adoption, behind not only European countries but also multiple Asian countries such as China, Singapore and Thailand. Beside cars, progress is minimal with fewer than 300 electric vans and trucks sold in 2024. IEEFA also found that diesel use in mining is likely to continue to increase well into the 2030s with many companies deferring their electrification plans. Policy signals are weak and sometimes even hinder progress.

While costly, developing supply chains for low-carbon fuels is also likely to be required, especially in aviation and other heavy transport.

The government knows what it must do – it has already developed transport and resources sector plans. Now is the time to focus on their swift implementation to accelerate the electrification of Australia’s transport and mining sectors, and to ensure the country is not left so exposed to the next global crisis.