Key Takeaways CoreWeave is expanding AI data centers, backed by a $66.8B backlog and NVIDIA investment to scale capacity.Cloudflare expects up to $2.8B in 2026 revenues, driven by AI, serverless platform and enterprise growth.NET trades at a much higher Price/Sales ratio, while CRWV faces heavy CapEx, debt and margin pressure risks.

The AI infrastructure boom is creating a new generation of cloud winners. Two prominent names against this backdrop are CoreWeave, Inc. (CRWV Quick QuoteCRWV – Free Report) and Cloudflare, Inc. (NET Quick QuoteNET – Free Report) . Both operate in cloud infrastructure and benefit from AI-driven computing demand, making them comparable plays on AI and cloud infrastructure growth.

Cloudflare is a global cloud services provider offering integrated solutions for web performance, security, networking and developer needs, with AI increasingly embedded into its offerings. CoreWeave is a specialized AI cloud provider focused on renting high-performance GPUs for training and running AI models. Cloudflare acts as a software-first platform that leverages AI demand, while CoreWeave serves as a mini hyperscaler for AI compute.

Per a report from Fortune Business Insights, the global cloud AI market is estimated to grow from $133.42 billion in 2026 to $780.64 billion by 2034, at a CAGR of 23.8%. The Cloud AI market is growing rapidly due to the rising adoption of generative AI, intelligent automation and cognitive computing. The expansion of 5G, increasing web traffic and growing demand for data storage, virtualization and analytics are also driving market growth.

While both CRWV and NET benefit from AI tailwinds, they operate very different business models, risk profiles and growth trajectories. Let’s break down which stock looks more attractive right now.

The Case for CRWV

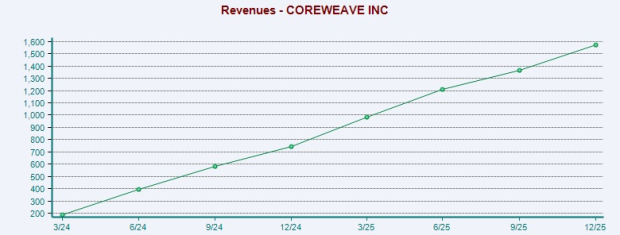

CoreWeave is positioning itself at the forefront by developing large, purpose-built AI clusters for demanding workloads. Management highlighted four key fundamentals – strong and diversified demand from hyperscalers, AI-native and enterprise customers; new margin-expanding opportunities driven by platform expansion and its NVIDIA (NVDA Quick QuoteNVDA – Free Report) partnership; rapid data center expansion supported by strong execution and strategic capacity growth; and a disciplined financial model that invests ahead of revenues to meet contracted demand, backed by a $66.8 billion backlog that provides strong visibility into future cash flows and returns.

Image Source: Zacks Investment Research

In 2025, CoreWeave increased the number of customers spending at least $1 million on its cloud by nearly 150%. These are long-term, multi-product relationships that can grow over time as companies integrate AI more deeply into their operations. It is expanding new ways to monetize its cloud as its platform evolves with higher-margin products and services, including offering its proprietary cloud stack to the broader NVIDIA ecosystem. It ended 2025 with more than 850 MW of active power across 43 data centers, and added about 260 MW in the fourth quarter alone. It also contracted nearly two GW of additional power in 2025, bringing total contracted capacity to more than 3.1 GW, most of which is expected to come online by 2027. This contracted, but not yet active, capacity represents solid future revenue potential as new capacity is built and deployed. In January 2026, NVDA invested $2 billion in CoreWeave, nearly doubling its stake, to expand data centers with a capacity of five GW by 2030.

Apart from organic growth, CoreWeave is expanding vertically and horizontally through strategic acquisitions. In October, it agreed to acquire Monolith AI Limited, a leader in applying AI to complex physics and engineering problems, to enhance its AI platform and accelerate R&D, product design and efficiency for customers. The deal builds on CoreWeave’s earlier strategic acquisitions, including OpenPipe (reinforcement learning) and Weights & Biases, which strengthen its end-to-end AI development capabilities. However, its proposed $9 billion purchase of Core Scientific was canceled after stakeholders rejected the deal.

CRWV’s growth is explosive but extremely expensive. It is funding its growth with significant capital, including $2.6 billion in convertible notes and a $2.5 billion credit facility, raising concerns about dilution and debt. As of Dec. 31, 2025, long-term debt was $14.7 million compared with $5.5 million a year earlier.

Fourth-quarter interest expense jumped to $388 million from $149 million, due to higher debt taken to fund CRWV’s infrastructure growth. It expects 2026 CapEx of $30–$35 billion, more than doubling 2025 levels, which will likely pressure near-term profits due to the timing gap between upfront costs and gradual revenues from new capacity. The company is investing heavily in AI infrastructure while burning cash, and risks remain due to customer concentration and intense competition in the AI infrastructure market.

The Case for NET

NET’s growth strategy focuses on a clear progression of acquiring new customers through increased awareness and global reach, deepening relationships by expanding usage and upselling existing clients, and driving innovation through rapid product development to enter new markets. It further aims to extend its serverless platform, enabling new applications, increasing customer stickiness and unlocking additional market opportunities. The company expects up to $2.8 billion in 2026 revenues, backed by large customer growth, strong free cash flow and multiple growth drivers across AI, developer platforms and channel expansion.

Cloudflare’s acquisition strategy has played a key role in expanding its portfolio, strengthening security, networking and developer capabilities. Since 2009, the company has acquired 21 businesses. Recent acquisitions include Human Native and the Astro Technology team in 2026, Outerbase and Replicate in 2025, and Kivera, BastionZero, Baselime, and PartyKit in 2024. These deals enhance Cloudflare’s AI, security, serverless and developer platforms, helping it enter new markets, deepen enterprise adoption and support long-term growth.

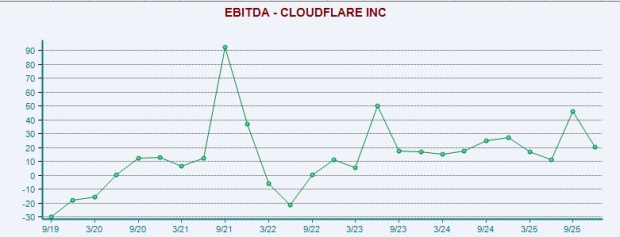

Cloudflare is positioning itself as the infrastructure layer for AI agents, which could dramatically expand its total addressable market. Its serverless platform is becoming a core growth engine, competing with offerings from AWS Lambda and others. With increasing cyber threats, Cloudflare’s integrated security solutions are gaining traction among enterprises. It is driving growth through its subscription-based model, which delivers stable, high-margin recurring revenues. Strong adoption of its core application services, Zero Trust solutions, and network offerings like Magic Transit is supporting steady revenue and profitability growth.

Image Source: Zacks Investment Research

However, Cloudflare faces risks from macroeconomic and geopolitical uncertainty, which can weigh on enterprise IT spending. Management noted a cautious start to 2026, with rising infrastructure costs affecting sentiment. As businesses may delay cloud and security investments, slower deal activity and enterprise budget cuts could impact growth. To survive in the highly competitive cybersecurity market, each player must continually invest in broadening its capabilities. Over the past few years, Cloudflare has invested heavily to enhance its sales and marketing capabilities, particularly by increasing its international presence. This has negatively impacted its operating margins.

Further, in Q4, NET’s gross margin fell to 74.9%, down 40 basis points sequentially and 270 basis points year over year, below its 75–77% target. The decline was driven by higher infrastructure and traffic costs and a shift toward fast-growing platform services. While revenues are growing, margin pressure suggests growth is becoming more expensive, which could limit operating leverage if the trend continues.

Share Performance for NET & CRWV

Over the past year, NET has surged 80.1% while CRWV has gained 101.7%.

Image Source: Zacks Investment Research

Valuation: Discount vs. Premium

In terms of the forward 12-month Price/Sales ratio, NET’s shares are trading at 23.96X, way more than CRWV’s 2.12X.

Image Source: Zacks Investment Research

How Does the Zacks Consensus Estimate Compare for NET & CRWV?

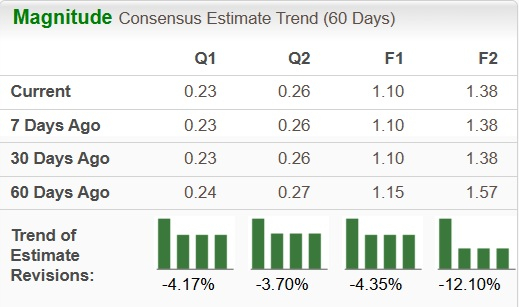

Analysts have significantly revised their earnings estimates downward for NET’s bottom line for the current year.

Image Source: Zacks Investment Research

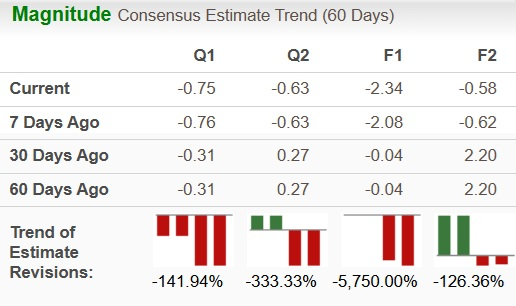

For CRWV, estimates have also been revised downward over the past 60 days.

Image Source: Zacks Investment Research

NET or CRWV: Which Stock Has More Upside?

Both NET and CRWV currently carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

If we compare upside potential alone, CoreWeave likely has higher upside because it is directly tied to AI infrastructure demand and is growing at a much faster pace. However, this also makes it much riskier. Cloudflare, meanwhile, may offer more consistent long-term compounding through recurring revenues, enterprise growth, AI developer platforms and network effects. Investors seeking maximum upside and willing to accept higher risk may prefer CoreWeave, while those looking for long-term stable growth with AI exposure may prefer Cloudflare.