Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

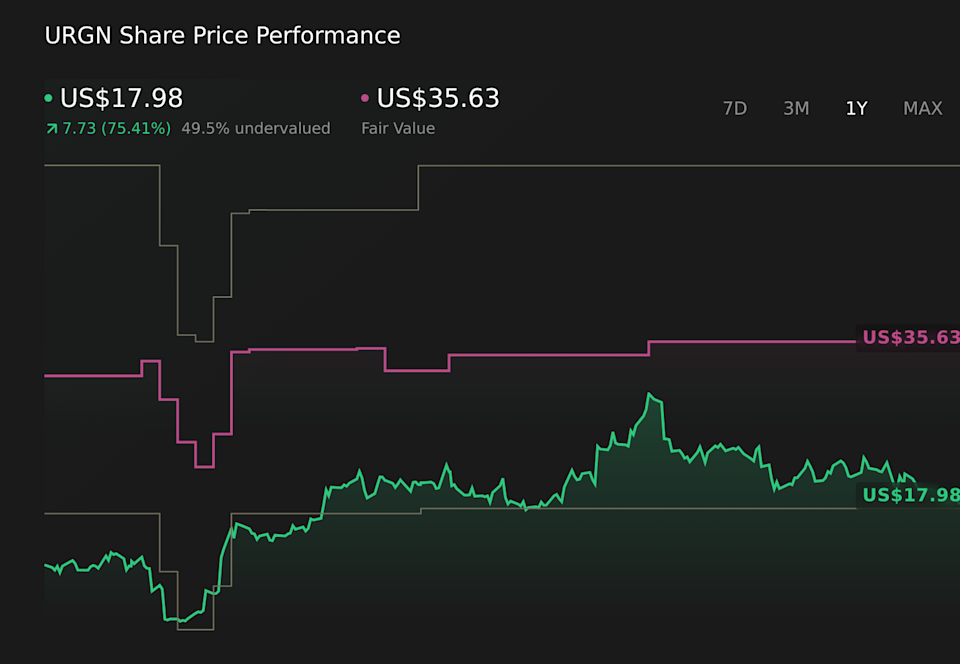

UroGen Pharma’s latest analyst update keeps the fair value target effectively anchored at US$35.63, with no reset in the central valuation estimate. Bullish voices see this as support for a constructive risk and reward setup, while more cautious analysts point to the unchanged fair value as a reason to wait for clearer clinical or commercial evidence. As you read on, you will see how to track these shifting views and what signals to watch as the narrative develops.

Stay updated as the Fair Value for UroGen Pharma shifts by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on UroGen Pharma.

H.C. Wainwright keeps a Buy rating while trimming its Ur-Energy price target to US$2.30 from US$2.60. This signals that, even with recent dilution, the firm still sees upside potential in the equity story.

Northland maintains an Outperform rating with a revised target of US$1.85 from US$2.15. This indicates that, despite updated operating cost assumptions, the firm continues to view the risk and reward trade off as attractive.

Northland highlights higher operating expenses at Lost Creek, which it says more than offset about 1 million pounds of net additional resource. This raises questions for investors about cost efficiency and future cash needs.

The same Northland report flags a startup delay at Shirley Basin from Q1 to Q2 due to regulatory approvals. This may make some holders more cautious around execution timing and potential project slippage.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there’s more to the story. Head to the Simply Wall St Community to discover more perspectives!

NasdaqGM:URGN 1-Year Stock Price Chart

NasdaqGM:URGN 1-Year Stock Price Chart

We’ve flagged 2 risks for UroGen Pharma. See which could impact your investment.

The pivotal Phase 3 ENVISION trial results for ZUSDURI in The Journal of Urology reported a 79.6% complete response rate at three months and a 72.2% probability of remaining event free at 24 months after complete response in adults with recurrent low grade intermediate risk non muscle invasive bladder cancer, with mostly mild to moderate adverse reactions and 12% serious adverse reactions.

Post hoc analyses from ENVISION showed three month complete response rates of 83.9%, 81.2%, and 60.0% for ZUSDURI in low, intermediate, and high European Organization for Research and Treatment of Cancer recurrence risk groups, with Kaplan Meier estimates indicating most responders remained recurrence free at 24 months.

A permanent Healthcare Common Procedure Coding System Level II J Code (J9282) for ZUSDURI took effect on January 1, 2026, which is expected to streamline billing and reimbursement in US hospital outpatient and physician office settings.

UroGen Pharma entered a loan agreement of up to US$250,000,000 with BPCR Limited Partnership and BioPharma Credit Investments V (Master) Lp, including an initial US$200,000,000 Tranche A funded on February 26, 2026, an optional US$50,000,000 Tranche B available through June 30, 2027, a fixed 8.25% interest rate, and maturity in 2031 with related fees.

Story Continues

Fair value is held at US$35.63, with no change in the central valuation estimate.

Revenue growth is kept at 70.60%, with no material shift in long term top line assumptions.

Net profit margin remains around 31.33%, with only a minimal technical model adjustment.

Future P/E is held at 14.69x, reflecting a very small refinement in the earnings multiple.

The discount rate is shown at 7.31%, with only a very slight recalibration of perceived risk.

Narratives link a company’s clinical and commercial story to a financial forecast and fair value, updating as fresh trial data, reimbursement decisions, or financing moves come through. They help you see how individual headlines fit into a bigger picture that analysts are tracking over time.

Head over to the Simply Wall St Community and follow the Narrative on UroGen Pharma to stay up to date on:

How ZUSDURI’s launch into a large, underserved bladder cancer market and its ENVISION Phase 3 data feed into revenue expectations and product dependence.

The impact that a permanent J-code, office based treatment trends, and pipeline progress for programs like UGN-103 could have on revenue mix and future profit margins.

Key risks such as heavy operating losses, concentrated revenue around a small product set, reimbursement hurdles, and high R&D and SG&A spending that could pressure funding needs and profitability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include URGN.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com