Layoffs don’t just affect an individual mentally, but have an equal, and sometimes a bigger impact on their finances. Without a proper safety net, your savings can take a hit in no time. If not managed well it can even lead to a debt trap. To help employees navigate such scenarios, the Employees’ Provident Fund Organisation (EPFO) has simplified its withdrawal rules, so that members can easily access their PF amount.

Under the revised rules, the employee pension fund body has shrunken the number of categories for funds withdrawal, making it easier for members to take out their funds. EPFO’s revised framework has brought down withdrawal categories from 13 to 3 broad groups, which simply means that there are just three simple categories to choose from when deciding to withdraw your PF amount.

Provident Fund withdrawal rules are now categories in 3 main groups – Essential Needs, Housing Needs, and Special Circumstances. This helps ease the choice for members to decide clearly when and how they can withdraw their money. Withdrawal in case of unemployment falls into the Special Circumstances category.

PF withdrawal rules simplified: How much can you withdraw if you are unemployed?

While members are entitled to take out up to 100% of their eligible EPF balance, including both employee and employer contributions, there are certain terms and conditions that apply. So, what happens in case you lose your job or are laid off by your company? Revised EPFO withdrawal rules allow an unemployed person to make a partial withdrawal for the first one year.

ALSO READ | Will EPF interest rate rise to 10%? Central government clarifies stance on rate hike and feasibility

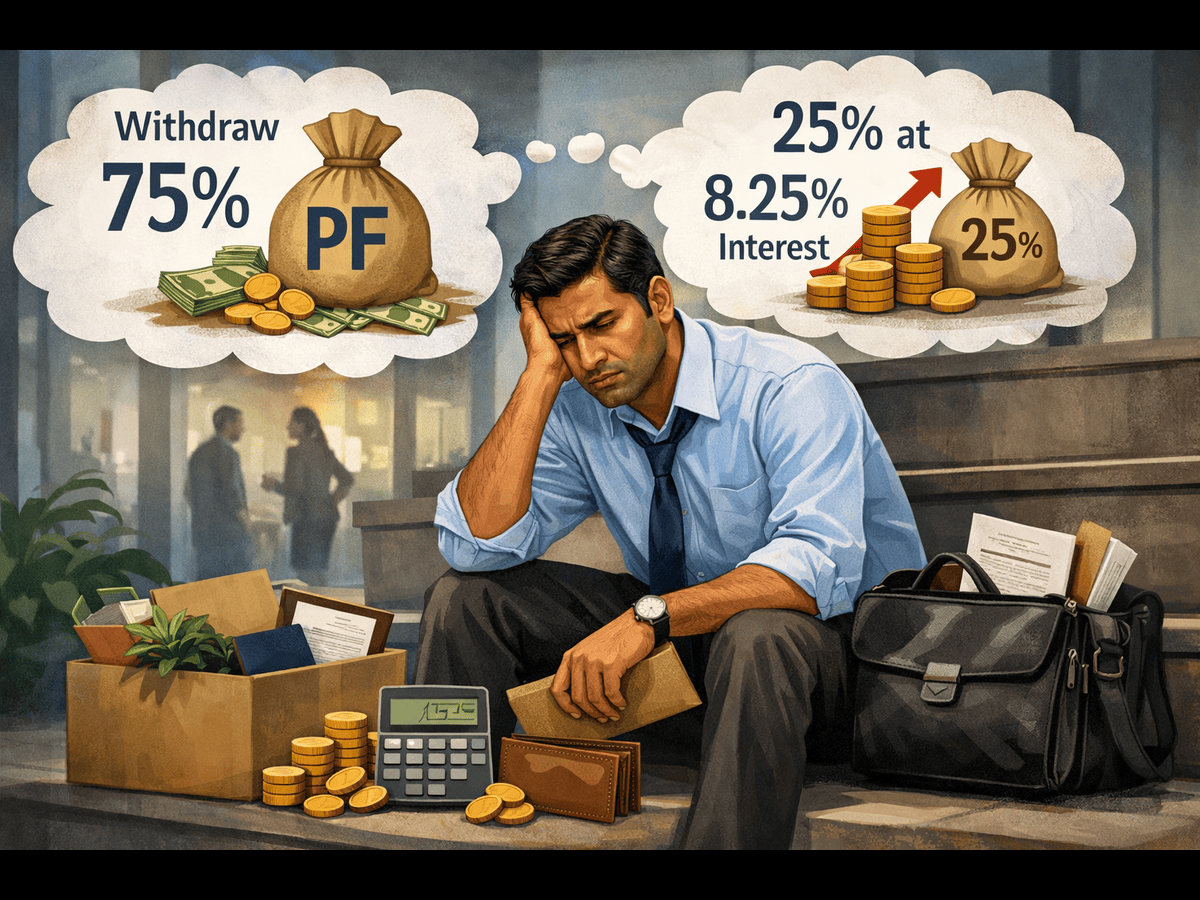

If you lost your job or were laid off, you can now withdraw up to 75% of your PF balance immediately, while the remaining 25% amount can be taken out after 12 months if the person continues to remain unemployed. “Now, the withdrawable amount will also include employer contribution besides employee contribution and interest,” the EPFO had clarified earlier.

This is so that members don’t lose out on all their savings in one go. While explaining the rationale behind allowing 75% PF withdrawal in case of job loss, the EPFO said, “Due to repeated withdrawal, the workers with lower salaries did not realize the benefits of compounding @8.25% and thereby losing out on higher social security at the end of their working life.”

That is why, as per CBT’s decision, 25% of the contribution needs to be retained to ensure respectable corpus at retirement as a safety net and to provide long-term social security.

ALSO READ | EPFO plans auto-settlement to clear Rs 5,200 crore in inoperative accounts

What do EPFO rules say about 100% PF withdrawal?

EPFO says that a full withdrawal of the entire PF balance (including the minimum balance of 25%) can also be made. It is also allowed in case of retirement after attaining 55 years of service, permanent disability, incapacity to work, retrenchment, voluntary retirement or leaving India permanently etc.

Meanwhile, the revised framework has no impact on the pension entitlement at the age of 58 years. A member can withdraw the accumulation in an Employee Pension Scheme (EPS) account before completing 10 years of service at any point of time in these 10 years. However, to qualify for a pension at retirement, a member must complete at least 10 years of EPS membership with regular contribution.