Key Takeaways NVIDIA posted record $68.1B Q4 revenues, up 73% YoY, driven by strong AI data center demand.TSMC delivered record profit and revenue growth, fueled by robust demand for advanced AI chips.NVDA shows lower debt, higher ROE, and slightly cheaper valuation than TSMC, strengthening its edge.

NVIDIA Corporation (NVDA Quick QuoteNVDA – Free Report) and Taiwan Semiconductor Manufacturing Company Limited (TSM Quick QuoteTSM – Free Report) , or TSMC, have both delivered strong revenue growth and profitability in their latest quarterly results, benefiting from the ongoing surge in artificial intelligence (AI) demand. But which one is more attractively valued, and a better buy at the moment? Let’s take a closer look.

The Bullish Case for NVDA Stock

NVIDIA’s latest strong data center performance underscored its leading position in hyperscale AI infrastructure investment. The Jensen Huang-led company posted record revenues of $68.1 billion in the fiscal fourth quarter of 2026, representing a 73% jump year over year and a 20% sequential gain, according to nvidianews.nvidia.com.

The data center segment was the primary driver, generating $62.3 billion in revenues, up 75% year over year and 22% sequentially, supported by increased adoption of AI and accelerated computing platforms. Looking ahead, NVIDIA expects revenues of around $78 billion, with a margin of plus or minus 2% for the fiscal first quarter of 2027. This shows management’s confidence in the continued global expansion of AI adoption and reflects strong demand for data center solutions.

Huang added that the enterprise use of AI agents is accelerating rapidly, with customers “racing to invest in AI compute — the factories powering the AI industrial revolution and their future growth.” Meanwhile, NVIDIA continues to generate exceptionally strong gross margins, showcasing its ability to command premium pricing for its graphics processing units (GPUs) and AI accelerators, while maintaining strong demand for its products.

For the fiscal fourth quarter, NVIDIA’s non-GAAP gross margin was 75.2%, and is expected to remain near 75% for the fiscal first quarter, even after accounting for stock-based compensation. This indicates the company’s ability to maintain strong profitability while managing additional cost pressures.

The Bullish Case for TSMC Stock

TSMC is well-known for manufacturing cutting-edge semiconductor chips across a slew of industries, including AI data centers, smartphones and consumer electronics. TSMC’s advanced chips are designed by the likes of NVIDIA, and it boasts of having major customers such as Apple Inc. (AAPL Quick QuoteAAPL – Free Report) , Amazon.com, Inc. (AMZN Quick QuoteAMZN – Free Report) , Broadcom Inc (AVGO Quick QuoteAVGO – Free Report) and Intel Corporation (INTC Quick QuoteINTC – Free Report) , to name a few. These solid partnerships place TSMC alongside big tech players, allowing it to play a pivotal role in the rapid growth of the AI megatrend.

TSMC reported a net income of NT$572.48 billion in the first quarter ended on March 31, 2026, up 58.3% year over year, and easily surpassing analysts’ expectations, according to pr.tsmc.com. TSMC’s net income reached another record as demand for advanced AI chips remained robust.

TSMC posted a consolidated revenue of NT$1,134.10 billion in the first quarter, up 35.1% year over year. In U.S. dollars, revenues for the first quarter were $35.90 billion, up 40.6% year over year. The bulk of the sales was generated by TSMC’s high-performance computing segment, which includes AI-related applications. Meanwhile, advanced process technologies defined as 7-nanometer or smaller accounted for 74% of total wafer revenues during the quarter.

Looking ahead, TSMC expects second-quarter 2026 revenues of $39 billion to $40.2 billion, marking a 10% rise sequentially. The company also expects gross and operating margins to improve in the quarter, and overall growth to remain strong throughout 2026, driven by strong demand for its leading-edge process technologies. The company is projected to increase its capital expenditure this year, reflecting its efforts to scale up its expansion initiatives.

NVDA Has the Edge: Why It’s a Better AI Buy Than TSMC Now

NVIDIA is seeing strong momentum driven by booming AI and data center demand, and expects sustained growth across its data center and accelerated computing business.

Similarly, TSMC posted a record financial performance driven by strong demand for its advanced AI chips. TSMC is expected to maintain solid growth and continue expanding capacity to meet rising industry needs. Management also indicated that the ongoing Middle East crisis isn’t likely to significantly disrupt its supply chain, given its multiple sourcing and well-managed inventory.

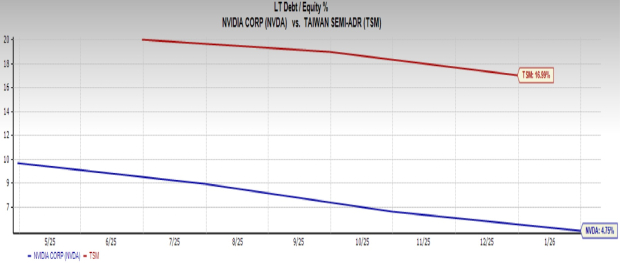

However, TSMC’s debt-to-equity ratio of nearly 17% far exceeds NVIDIA’s 4.8%, indicating greater financial risk and potentially higher vulnerability to economic downturns.

Image Source: Zacks Investment Research

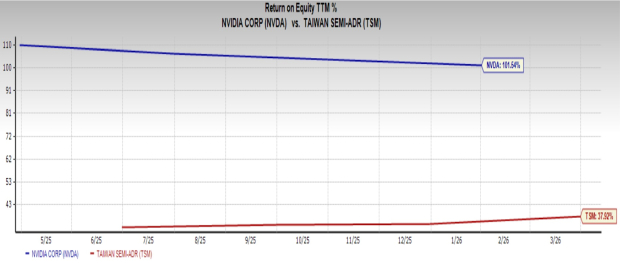

Additionally, NVIDIA remains more efficient in generating profits than TSMC. This is because NVIDIA’s return on equity (ROE) of 101.5% exceeds TSMC’s ROE of 37.9%.

Image Source: Zacks Investment Research

Lastly, NVIDIA’s shares appear more reasonably valued than TSMC’s, offering investors a potential advantage. Per the price/earnings ratio, NVDA trades at 24.69 forward earnings compared with TSM’s forward earnings multiple of 25.17.

Image Source: Zacks Investment Research

Therefore, despite both remaining strong AI leaders with continued growth potential, NVIDIA’s lower debt, higher efficiency, and attractive valuation make it the better buy now. NVIDIA has a Zacks Rank #1 (Strong Buy), while TSMC has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks Rank #1 stocks here.