Find winning stocks in any market cycle. Join 7 million investors using Simply Wall St’s investing ideas for FREE.

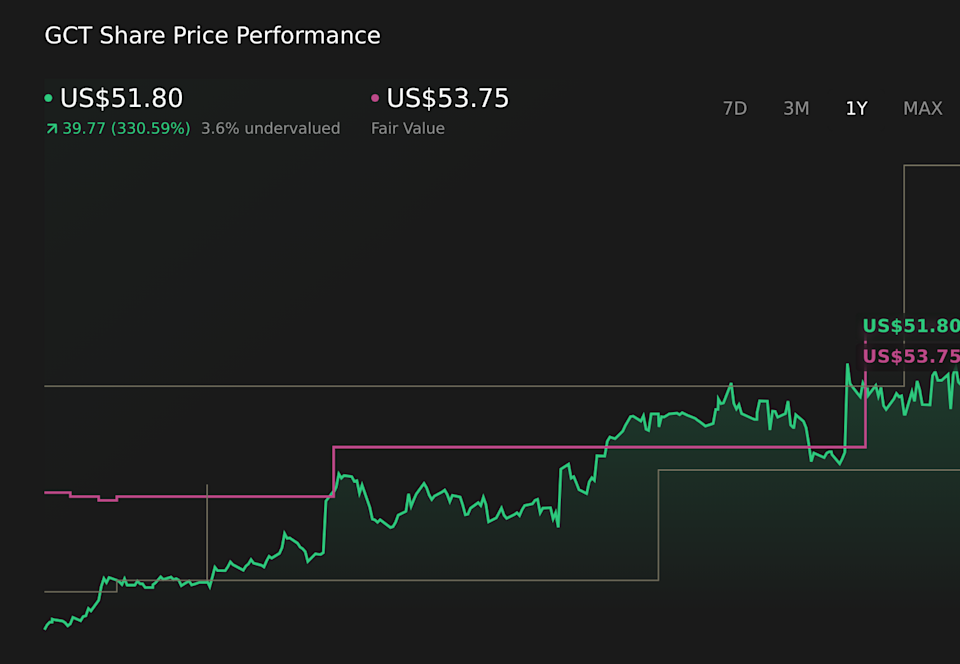

GigaCloud Technology’s refreshed analyst narrative is anchored around a higher modeled fair value, with the price target moving from US$52.00 to US$53.75 per share. Analysts tying this shift to recent research point to stronger Q4 execution and a mix of optimism and caution around how that performance supports updated assumptions. As you read on, you will see how these changing targets and viewpoints can help you track the next phase of the GigaCloud story.

Stay updated as the Fair Value for GigaCloud Technology shifts by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on GigaCloud Technology.

Maxim lifted its price target on GigaCloud to US$73 from US$44, signaling that its analyst now assigns a higher fair value to the shares based on recent research.

In its Q4 review, Maxim highlighted results that were ahead of estimates across key metrics, with revenue above the high end of management guidance.

Maxim cited the recovery in the Noble House brand and firm international sales as important supports for its updated view on the business.

Even with the higher price target, Maxim’s stance still leaves room for debate around how repeatable the recent Q4 performance may be and how much of it is already reflected in current expectations.

The emphasis on specific drivers such as the Noble House turnaround and international sales implies that any cooling in these areas could challenge the assumptions behind Maxim’s revised valuation.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there’s more to the story. Head to the Simply Wall St Community to discover more perspectives!

NasdaqGM:GCT 1-Year Stock Price Chart

NasdaqGM:GCT 1-Year Stock Price Chart

We’ve flagged 2 risks for GigaCloud Technology. See which could impact your investment.

The audit committee appointed Grant Thornton LLP as GigaCloud Technology’s new independent registered public accounting firm, following the dismissal of KPMG Huazhen LLP, citing a better fit with the current operational structure and priorities.

Between October 1, 2025 and February 26, 2026, the company repurchased 626,310 shares for US$22.02 million, bringing total buybacks under the August 18, 2025 program to 1,055,045 shares for US$33.35 million, or 2.82% of shares.

For the first quarter of 2026, management issued revenue guidance in a range of US$330 million to US$355 million, giving investors a reference point for near term expectations.

Story Continues

The fair value per share has been updated from US$52.00 to US$53.75.

The assumed long-term revenue growth rate has moved from 9.13% to 9.85%.

The modeled net profit margin has been adjusted from 9.46% to 9.86%.

The target future P/E multiple has changed from 13.06x to 12.72x.

The discount rate in the model has been revised from 7.55% to 7.61%.

Narratives connect GigaCloud Technology’s business story to a set of explicit assumptions on growth, profitability, and risks. They update as new data and research come through, so you can see how the story and the modeled fair value evolve together.

Head over to the Simply Wall St Community and follow the Narrative on GigaCloud Technology to stay up to date on:

How expansion into international markets and integrated cross border logistics is shaping GigaCloud’s position in B2B ecommerce and supporting revenue and customer growth.

The role of operational efficiencies, SKU rationalization, and acquired businesses such as Noble House in supporting margin outcomes and revenue diversification.

Key risks such as reliance on European growth, exposure to tariffs and supply chain disruptions, and the sensitivity of service revenue to freight rates and warehousing demand.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include GCT.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com