(Bloomberg) — Credit investors are loading up on riskier debt, betting that Iran and the US can extend their truce, and leaving behind havens they’ve favored since the war broke out in late February.

Most Read from Bloomberg

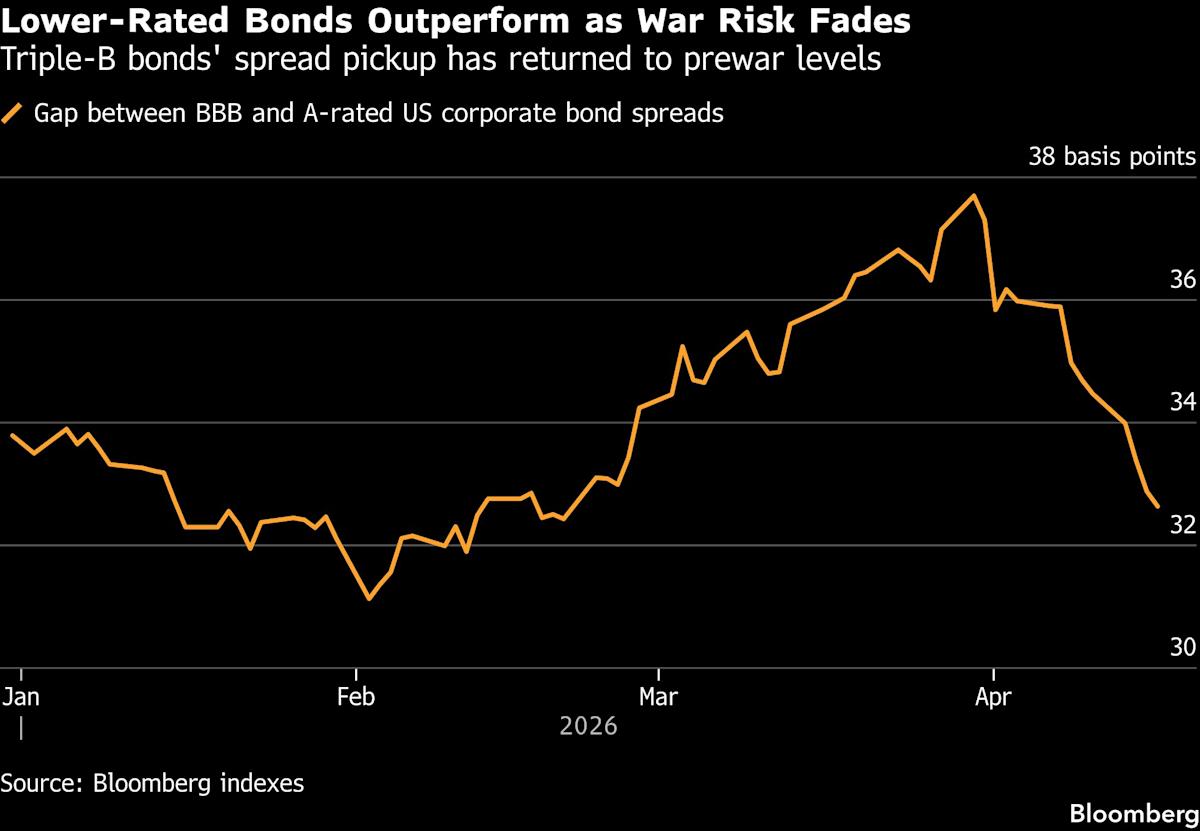

In the first half of April, investors bought a net $500 million of bonds in the lowest tier of investment grade, and sold $7.3 billion of the higher tiers, according to JPMorgan Chase & Co. That helped BBB bonds perform comparatively better than higher-rated notes, pushing the gap between spreads for BBB and A corporates to the tightest since before the war.

There may be good reason for these slightly riskier bonds to be performing better: BBB rated companies have outperformed analysts’ average forecasts more than A companies have, according to a Bloomberg News analysis. Buyers are hoping a more lasting peace in the Middle East can be forged by negotiators, and that companies in the lower edges of investment grade can keep performing well.

“There is some value in the BBB space and issuers there have been good stewards of the balance sheet and generally improving credit quality,” said Gene Tannuzzo, global head of fixed income at Columbia Threadneedle Investments.

Investors have also been snatching up junk bonds, although with a preference for the higher-rated end of the spectrum, implying that money managers still see risk ahead even as they grow moderately more hopeful. Overall spreads for junk bonds are at their tightest since the war began, averaging 2.72% as of Thursday’s close.

On Thursday, cloud infrastructure provider CoreWeave Inc. tapped the US junk-bond market for the second time in just a week, selling $1 billion of additional debt following the successful raise of $1.75 billion. High-yield bonds posted a $2.8 billion inflow this week, the largest amount recorded since June of last year, according to LSEG Lipper.

In the high-grade market, first-quarter results so far bolster the view that companies have withstood the energy shock. Among the first 100 companies to report, those rated within the BBB band by S&P Global have outperformed analysts’ average earnings expectations by 9.3%, based on data compiled by Bloomberg News. The number for firms rated A or above is 6.2%.

Corporate earnings expectations have continued to rise despite the conflict, with lower-rated firms delivering early earnings beats and renewing optimism over artificial intelligence.

Story Continues

To be sure, bets on BBB issuers are becoming crowded, with their spread to A peers in the US at the lowest since before the war.

“We view BBBs as rich,” said Tony Trzcinka, an investment grade portfolio manager at Impax Asset Management.

Energy firms account for about 10% of Bloomberg’s BBB corporate index, but just 3% of A rated peers. That also helps explain some of the outperformance for the former.

AI Binge

Issuers whose debt has ballooned are also stirring concern. Notably, BBB rated Oracle Corp. has taken out $120 billion of bonds for a debt-fueled and still unproven wager on AI, and become the biggest borrower in the Bloomberg US high-grade corporate bond index, outside of banks.

Tannuzzo is wary of companies rapidly increasing leverage to finance AI projects, and sees value in utilities, energy and telecommunications firms.

Likewise, Jon Curran, head of investment grade credit for Principal Asset Management, is looking for companies that are deleveraging and issuers with strong balance sheets and industry positions.

Meanwhile, negotiations to end the war are ongoing, with some Gulf Arab and European leaders warning a peace deal would take about six months to be agreed, though President Donald Trump said he’d won key concessions. On Friday, Iran said it would open the Strait of Hormuz for the duration of a 10-day ceasefire between Israel and Hezbollah in Lebanon, increasing the prospect of a wider peace deal.

These hopeful signs are enough to unleash buyers in both secondary and primary credit markets. Borrowers in the high-grade US market sold nearly $58 billion in bonds this week, led by banks, more than 40% above expected issuance. In Europe, banks and insurers raised the largest amount from junior-ranked bonds since before the war.

“Demand has kept pace with elevated issuance, with the market absorbing supply in an orderly way,” Curran said.

Click for a podcast with Davidson Kempner as it eyes $770 billion in troubled loans

Week In Review

Private credit funds known as business development companies this week were able to borrow in the US bond market for the first time since February, amid a broader easing of fears across markets as the war in Iran showed signs of moving toward a settlement. A Goldman Sachs private credit fund raised $750 million, while a Blue Owl private credit fund raised $400 million.

Pacific Investment Management Co. bought all of the bonds sold by the Blue Owl fund.

But fear hasn’t totally left the market for BDC debt. Average spreads on the securities are still wider than their levels in early January, even after a recent rally, according to a Bloomberg index.

The biggest US banks disclosed more than $185 billion of combined exposure to private credit. Executives — many of whom sought to calm investors’ jitters — still see potential in the market.

Anxiety about American financial institutions’ exposure to private credit has led investors to demand a higher premium on bonds issued by US banks than their European counterparts, even as the space has shown signs of stabilizing in recent days, Citigroup wrote earlier this month.

A BlackRock private credit fund in Asia suffered the first default by a borrower in its portfolio after a Chinese company failed to repay a loan.

Golden Goose priced an €880 million ($1.04 billion) bond sale to fund its acquisition by Chinese private equity firm HSG, a test of investor sentiment given struggles in the luxury sector and concerns around the Iran war.

Sotheby’s seized a window of opportunity to refinance debt due next year, before any disruptions from the US-Iran negotiations can derail capital-raising efforts. And Herbalife sold junk debt a month after shelving a loan offering due to market volatility.

More banks are being invited to join SoftBank Group’s $40 billion loan backing its investment in US tech giant OpenAI, in one of the biggest tests yet of creditor sentiment toward the Japanese conglomerate’s debt-fueled push into AI. Separately, SoftBank also tapped the bond market for an additional source of funding.

A record deal involving Google-backed data centers and an add-on sale by cloud infrastructure firm CoreWeave raised a combined $6.7 billion in new junk debt.

TCW Group marked down its equity stake in Red Lobster by roughly 98% since acquiring it via the restaurant’s 2024 bankruptcy, leaving shares held by a private credit fund it oversees now worth less than $1 million.

Television shopping network QVC Group filed for bankruptcy as part of a plan to cut more than $5 billion of debt, as declining viewership and a shift to online retail weighed on sales and squeezed margins.

China’s data center operators are tapping a fast-growing asset-backed security market, raising more than $1 billion dollars from investors hungry for higher yields.

On the Move

JPMorgan hired Steve Cho, formerly of Hudson River Trading, as a managing director. He left HRT in May after nearly five years at the market-making firm, where he was an algorithm developer and quantitative portfolio manager focused on credit.

Bobby Jain’s multi-strategy hedge fund made four new hires from rival firms, including Brendan O’Hearn who is joining from Hudson River Trading as a credit portfolio manager based in New York.

RBC Capital Markets hired Dana Leventhal as head of private finance origination. She previously worked at Nomura, spending 16 years in securitized product sales.

Goldman Sachs’ head of leveraged finance for Asia (ex-Japan), Nelson Lo, is retiring at the end of April after a banking career spanning four decades.

Bank of Montreal hired Bhardeep Heer to work in its public sector debt capital markets origination and syndication businesses. Heer joins from Nomura where he worked for almost two decades.

One of Oaktree Capital’s most senior investment professionals for Asia, Pedro Urquidi, is set to leave the firm in coming months. He heads opportunistic credit outside North America, having moved to Hong Kong in 2019 to help grow the firm’s Asia platform.

ING named Joseph Kerkor head of emerging markets credit trading in EMEA. Kerkor was previously an executive director in emerging markets credit trading at Barclays.

Mizuho hired two loan bankers in Hong Kong, namely Bank of America veteran Joseph Yip and UBS Group’s Alex Lo, as the Japanese lender builds out its leveraged and acquisition finance business.

–With assistance from Rene Ismail.

Most Read from Bloomberg Businessweek

©2026 Bloomberg L.P.