As Europe links market access to carbon intensity, India faces a strategic test; and Israel’s innovation ecosystem offers practical tools to support its transition.

As carbon costs become embedded in global trade, India finds itself navigating a profound economic transition. The country must rethink how it competes, how it produces, and how it positions itself in markets that increasingly reward low‑carbon manufacturing. Policy reform will be essential; and so, will the right partners. Israel, with its strengths in climate‑tech innovation, offers India a practical bridge into this emerging landscape.

CBAM and the EU’s Fit for 55: A New Trade Reality

The European Union’s Carbon Border Adjustment Mechanism (CBAM) is the clearest sign of how global trade is being reshaped by climate policy. It forms part of the EU’s Fit for 55 packages; a broad set of reforms aimed at cutting emissions by 55 percent by 2030. Fit for 55 updates the EU’s core climate tools, including emissions trading and renewable‑energy targets, and CBAM serves as its external counterpart. Its purpose is simple: ensure that imports face the same carbon costs as goods produced within Europe.

Since October 2023, exporters to the EU have been required to report the embedded emissions of their goods. In 2026, CBAM enters its financial phase, when importers must purchase certificates to cover the carbon content of their products. For India, this is not a distant regulatory shift. It is a direct challenge to the foundations of its industrial competitiveness; particularly in sectors where carbon intensity is structurally high and where the EU remains a major export destination.

The Exposure India Cannot Ignore

CBAM applies to a narrow set of sectors; but they are sectors where India is deeply exposed. Three stand out: steel, aluminum, and fertilizers. These industries are central to India’s export economy and major employers across the country.

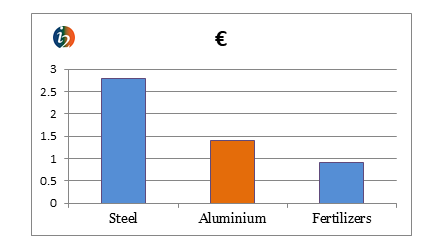

The EU imports between 1.5 and 2 million metric tons of Indian steel each year. It buys 300,000 to 400,000 metric tons of aluminum, and more than a billion dollars’ worth of fertilizers. These are precisely the sectors CBAM targets; and they are also the sectors where India’s carbon intensity is highest.

Exports in all three sectors have already begun to decline. Steel shipments to the EU fell sharply in 2024, with aluminum and fertilizer exports also contracting. Even before CBAM’s financial obligations begin, European buyers are adjusting to the new logic of carbon‑linked competitiveness.

“CBAM is not merely a constraint for India; it is an accelerant, pushing the country toward a cleaner, more competitive industrial future.”

India’s CBAM Exposure in One Picture

Figure: Estimated value of India’s steel, aluminum, and fertilizer exports to the EU (latest available full‑year data, 2024) | Sources: Eurostat; Indian industry export estimates (2024)

The concentration of India’s exposure is unmistakable; a small cluster of carbon‑intensive sectors accounts for a meaningful share of India’s EU‑bound industrial exports; and they are the first to feel CBAM’s impact.

A Structural Carbon Challenge

India’s industrial emissions profile is among the most carbon‑intensive in the world. Roughly three‑quarters of its electricity still comes from coal. More than 90 percent of steel is produced using coal‑based blast furnaces. Over 80 percent of aluminum smelting relies on captive coal power. Fertilizer production, especially ammonia and urea, is similarly energy‑intensive.

Because CBAM charges are tied directly to emissions, these structural realities translate into real cost increases. Indian exports could face double‑digit price additions once CBAM fees begin; 15–25 percent for steel, 20–35 percent for aluminum, and 10–20 percent for fertilizers. Without rapid adaptation, India risks losing ground in sectors that anchor both its export earnings and its industrial workforce.

A Moment to Leapfrog, Not Just Comply

Yet CBAM is not only a challenge. It is also a generational opportunity. India is already the world’s lowest‑cost producer of solar power. The National Green Hydrogen Mission aims to produce five million tons of green hydrogen annually by 2030, positioning India to export hydrogen‑based steel, ammonia, and other low‑carbon materials. The country’s target of 500 GW of non‑fossil energy capacity by 2030 provides the foundation for renewable‑powered industrial clusters.

These strengths give India a credible pathway to leapfrog older, carbon‑heavy technologies and build a new industrial ecosystem aligned with global demand. CBAM, in this sense, is pushing India toward a cleaner and more competitive future.

Where India Needs Support; and Why Israel Matters

India has challenged CBAM at the WTO, but it has also begun preparing domestically. The government is developing a national carbon market, expanding renewable energy infrastructure, and supporting green hydrogen production. But one critical gap remains: India lacks a unified national framework for emissions measurement and verification.

Without reliable product‑level emissions data, Indian exporters will struggle to comply with CBAM’s reporting requirements, even if their production becomes cleaner. This is where Israel becomes strategically relevant.

Israel has spent decades developing technologies at the intersection of energy, water, agriculture, and industrial efficiency; the very areas where India must move quickly. Its expertise in solar integration, grid management, and water‑energy optimization can help India reduce emissions in energy‑intensive manufacturing. Its leadership in clean‑tech innovation, from advanced sensors to industrial monitoring systems, can help Indian exporters measure and verify emissions more accurately, reducing reliance on EU default values and lowering CBAM‑related costs.

Just as importantly, Israel’s culture of rapid commercialization allows new technologies to move from pilot to deployment quickly. When paired with India’s manufacturing scale and vast domestic market, this creates a powerful combination: innovation at speed, and implementation at scale.

This partnership is not about altering India–Israel trade flows; CBAM does not apply to their bilateral trade. It is about leveraging complementary strengths to accelerate India’s readiness for a carbon‑priced global economy.

A Defining Moment

CBAM is a turning point. It challenges India to rethink how it produces, exports, and competes. But it also offers a pathway to transform India into a global hub for low‑carbon manufacturing. The countries that adapt early will shape the next era of global trade.

India has the scale, the talent, and the momentum to lead; if it chooses to act decisively, and if it embraces partners who can accelerate its transition. Israel, with its innovation ecosystem and clean‑tech strengths, is well positioned to be one of those partners, helping India move confidently from today’s carbon‑intensive landscape toward tomorrow’s low‑carbon economy.

Eliezer Avraham is the founder of i2, a strategic advisory firm shaped by Herzlian vision and legacy stewardship. He forges trusted Israel–India partnerships and writes on diplomacy, heritage, Jewish thought, and the strategic choreography of global alliances. His work blends biblical insight with geopolitical foresight, offering a storyteller’s lens on values, movement, and meaning across the Israel–India–US triangle.