Energy-intensive industries (EIIs) account for around one-fifth of EU greenhouse-gas (GHG) emissions. Within this group, the chemicals sector occupies a distinctive position. It is the Union’s fourth-largest manufacturing industry, with a turnover of €635 million in 2024, supplying essential inputs across almost all industrial value chains. Decarbonisation of the chemical sector will therefore shape the pace of the bloc’s broader industrial transformation.

The sector’s emissions stem not only from fossil fuels burned during production, but also from fossil-derived feedstocks. These are chemically incorporated into products and released as greenhouse gases at end of life disposal. Estimates suggest that feedstock-related emissions account for between 60% and over 80% of the sector’s total GHG footprint.

Technical solutions for low-carbon chemical production exist, including using bio-based and recycled feedstock and switching from gas-powered to electric furnaces. However, their large-scale deployment is constrained by economic factors. Upstream producers face significant capital expenditure to shift away from fossil-based feedstocks and processes. Downstream manufacturers must manage higher input costs, compliance costs and administrative complexity.

The central challenge is recovering the green premium: the additional cost associated with producing low-carbon goods. Without predictable demand, the green premium risks becoming a structural barrier to decarbonisation of the chemicals sector rather than a transitional feature. While estimates exist on how the premium could be distributed across value chains, more research is needed to understand real-world distribution mechanisms and their implications for competitiveness.

The European Green Deal established a governance framework to reach climate neutrality by 2050, backed by intermediate emission-reduction targets for 2030 and 2040. The chemicals industry faces growing pressure to reduce its carbon emissions, particularly due to carbon pricing introduced by the EU Emissions Trading System (ETS).

The ETS does not directly price feedstock carbon. However, it creates indirect pressure to shift away from fossil-based inputs, as their processing generates emissions and their embedded carbon is eventually released when products are used or disposed of. Extended Producer Responsibility (EPR) schemes, already in place for electronics, batteries and packaging, add further pressure by making producers financially responsible for end-of-life product management. While current EPR schemes do not directly price carbon, carbon-footprint declarations are increasingly being considered. The forthcoming Circular Economy Act could further extend EPR requirements. Taken together, ETS and EPR schemes increase the cost of carbon-intensive production, but do not provide a mechanism to recover those costs through guaranteed demand at viable prices.

The EU’s Clean Industrial Deal (CID) signals a shift towards stronger demand-side industrial policy, including public procurement, amounting to 16% of EU GDP annually, labelling and investments. By strengthening demand for low-carbon products, these measures aim to de-risk investments in cleaner production technologies and help chemical producers recover the costs of decarbonisation. However, the fundamental challenge of the green premium persists: without careful design, these instruments risk shifting costs and risks across the value chain rather than resolving them.

Public intervention to bridge the green premium is a strategic investment in industrial transformation. Well-designed demand-side instruments are more targeted and time-limited than direct subsidies. They are structured to leverage private capital alongside public funds, which alone are insufficient to finance full decarbonisation. Such policies can unlock investments, create high-skilled employment and strengthen European value chains.

This Policy Brief examines how the EU can accelerate chemical sector decarbonisation while safeguarding competitiveness through demand-side measures. Adopting a value-chain perspective, it puts forward policy recommendations to accelerate industrial decarbonisation in the chemicals sector while preserving the Union’s industrial base.

Read the full Policy Brief here.

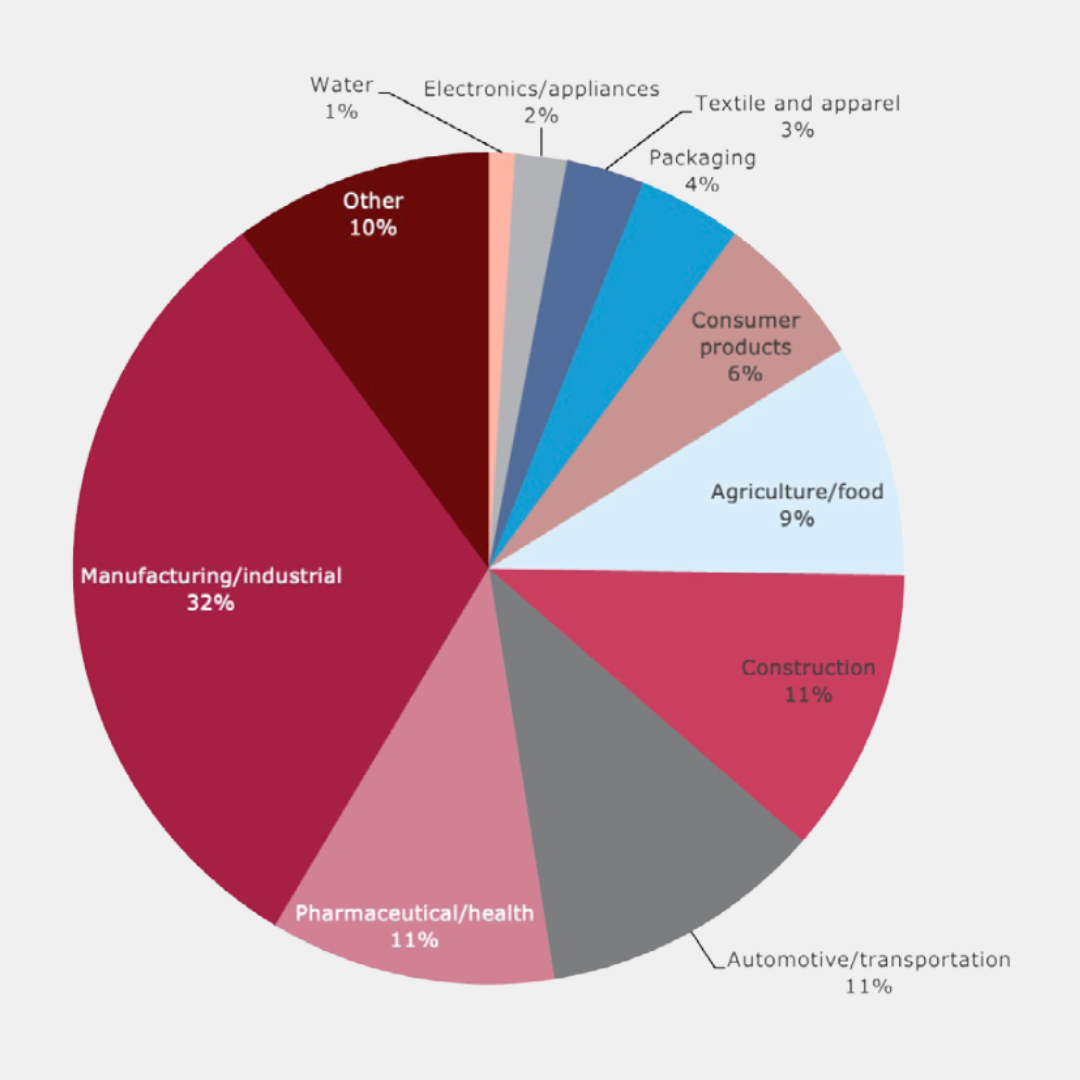

Figure 1: Share of chemicals sales in Europe by end market served

Credit: EPC, with data by Cefic, The Competitiveness of the European Chemical Industry, January 2025.

Anna Crawford is a Policy Analyst in the Sustainable Prosperity for Europe programme.

Stefan Šipka is Head of Sustainable Prosperity for Europe programme at the European Policy Centre.

Ana Berdzenishvili is a Junior Policy Analyst in the Sustainable Prosperity for Europe Programme at the EPC.

This project has been financially supported by the International Association for Soaps, Detergents and Maintenance Products (AISE).

The support the European Policy Centre receives for its ongoing operations, or specifically for its publications, does not constitute an endorsement of their contents, which reflect the views of the authors only. Supporters and partners cannot be held responsible for any use that may be made of the information contained therein.