Get insights on thousands of stocks from the global community of over 7 million individual investors at Simply Wall St.

Sociedad Química y Minera de Chile (NYSE:SQM) returned to profit after a prior net loss, supported by record lithium sales volumes.

The company reported record lithium output following its new joint venture and partnership with Chilean state miner Codelco.

Production from the SQM Codelco partnership surpassed initial targets, according to the company.

SQM outlined industry leading growth projections for lithium production and detailed new operational expansion plans.

Sociedad Química y Minera de Chile, listed on the NYSE under ticker SQM, is a major producer of lithium and other specialty chemicals with global exposure to battery and energy transition markets. The fresh profit and record output arrive as lithium remains central to long term electrification trends, with supply and demand imbalances continuing to be a key theme for investors. The new Codelco partnership gives SQM a prominent role in Chile’s lithium sector at a time when resource security is a priority for many countries and manufacturers.

For investors, the recent profit recovery, record volumes and production plans illustrate how SQM is positioning itself in the global lithium supply chain. The combination of a state backed partner, ambitious growth targets and operational expansions suggests that execution, capital allocation and project timelines could be important areas to monitor as this story develops.

Stay updated on the most important news stories for Sociedad Química y Minera de Chile by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Sociedad Química y Minera de Chile.

NYSE:SQM Earnings & Revenue Growth as at Mar 2026

NYSE:SQM Earnings & Revenue Growth as at Mar 2026

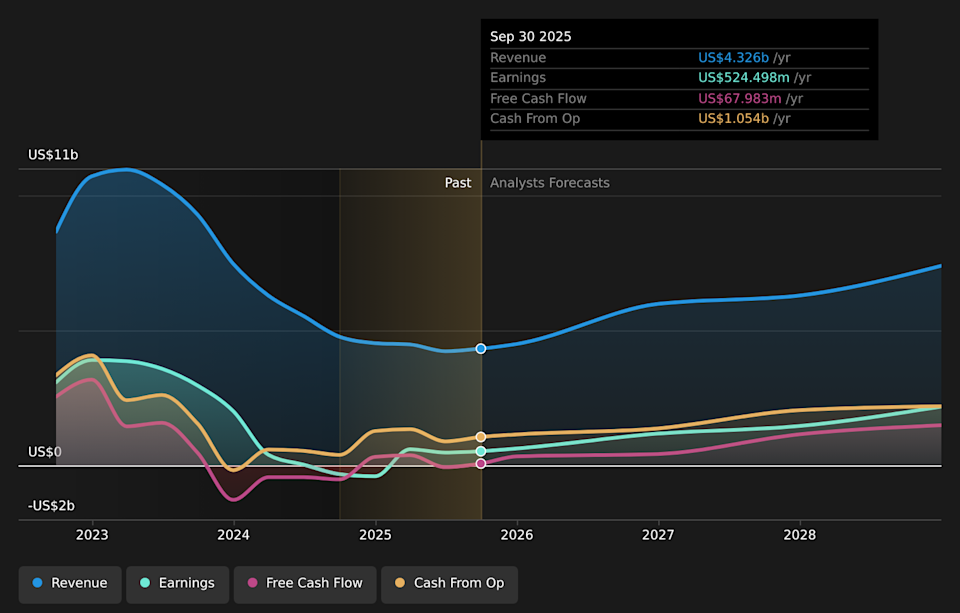

SQM’s return to profit alongside record lithium output under the Codelco partnership gives you a clearer picture of how deal execution is feeding directly into the income statement. Fourth quarter revenue of US$1,323.9 million and net income of US$183.8 million, plus full year profit of US$588.1 million after a prior year loss, are being supported by higher lithium sales volumes and contributions from iodine and plant nutrition. The Nova Andino Litio SpA venture reached 233,000 tons of lithium carbonate equivalent in 2025, above initial targets, while SQM is planning around US$2.7b of capex through 2027 to expand lithium carbonate and hydroxide capacity in Chile and Australia. For you as an investor, the key takeaway is that SQM is tying long dated resource access in the Atacama to volume growth plans at a time when it expects global lithium demand to rise about 25% this year. That potentially strengthens its position against peers such as Albemarle, Ganfeng Lithium and Tianqi Lithium, but also concentrates execution and capital deployment risk around a single partnership that runs to 2060.

The earnings rebound, record lithium volumes and Codelco partnership progress all support the narrative that capacity expansion and low cost brine assets can support revenue and margin resilience as demand for EV and storage batteries grows.

The heavy capex pipeline and reliance on lithium pricing highlight the narrative’s concern that aggressive growth plans and volatile markets could pressure returns if project timelines slip or prices soften.

The higher than expected 2025 output from Nova Andino and new regulatory commitments around Chinese offtake appear more specific than the existing narrative, which may not fully reflect how these operational and policy details shape future cash flows.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Sociedad Química y Minera de Chile to help decide what it’s worth to you.

⚠️ Analysts have highlighted that SQM’s dividend is not well covered by earnings or free cash flow, so higher payouts could compete with funding for the US$2.7b capex plan.

⚠️ Dependence on lithium prices, large scale projects in the Atacama and evolving Chilean regulations, including state involvement through Codelco, could affect margins and the pace of planned volume growth.

🎁 SQM became profitable again in 2025, with US$588.1 million of net income and record lithium sales volumes, which supports the view that its assets can generate earnings even through pricing swings.

🎁 The Codelco partnership securing production rights to 2060, plus expansion in Chile and Australia, positions SQM to compete on scale and costs with global peers if lithium demand increases as management expects.

From here, you may want to watch how quickly incremental capacity from the Atacama partnership and projects like Kwinana is brought online, and whether unit costs stay competitive as volumes ramp. Keep an eye on lithium demand trends versus SQM’s projection of roughly 25% growth, along with any changes in Chilean policy that could alter the economics of the Codelco venture or future projects such as Salar Futuro. The balance between funding the US$2.7b capex program and maintaining dividends and leverage levels will also be important for assessing how sustainable the current earnings recovery is.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Sociedad Química y Minera de Chile, head to the community page for Sociedad Química y Minera de Chile to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SQM.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com