Key Points

The Chinese economy has been generally weaker than acknowledged in the 2020s. The most frequently discussed solutions, such as stimulating consumption, cannot generate a sizable, sustained impact for more than a year or so.

Reinflating the property bubble would do so. It cannot be done immediately or easily but could for a multiyear period bring clearly faster economic growth without wrenching dislocation or automatically adding to the debt burden.

In the longer term, even successful property reflation will not matter much. Unwillingness to reform, debt accumulation, and especially demography guarantee a China that essentially stops growing by the late 2030s.

Introduction

The China economy field is full of people repeating the government’s numbers and “analyzing” them. If that’s sufficient, China watchers can just project a gradual fall from 5 percent GDP growth followed by a gradual fall from 4 percent, and the next decade is done. In addition, we should believe that China was pursuing market-oriented changes and rebalancing in 2007,1 property investment genuinely added to GDP in 2017,2 and consumption will be stronger in 2027. Consumption will always be stronger soon.3 Extreme skepticism of official Chinese data and policy claims is frequently warranted, but it’s rarely found.

This forecast is written accordingly. It is not a forecast of official GDP growth, which will continue to smoothly decline. It’s a forecast of reality. To the upside, there is an option for a challenging and temporary but meaningful economic revival in reflation of property. This avoids General Secretary Xi Jinping’s obvious aversion to pro-market reform and would be more cost-effective than undirected fiscal or monetary stimulus. Given some months for implementation, property reflation would make for a strong multiyear period for the economy. For the longer term, weakness is guaranteed due to debt and especially demography. Growth may persist, but barely, and China will not be a truly rich country in 10 years, 20 years, or 30 years.

2020–25: Not Encouraging

COVID and the effects of China’s zero-COVID policy make it difficult to evaluate economic performance in the 2020s to date. Ignoring the brief crash in 2020 and the statistical bounce in 2021 helps, especially since those years are furthest away. In the four years before the pandemic broke out, 2016–19, China’s GDP added a bit over 30 trillion yuan in nominal terms. From 2022 through 2025, despite a larger base, GDP climbed a total of 23 trillion yuan.4 For perspective, nominal American GDP added twice as much in 2022–25 as it did in 2016–19.5 China is poorer and should have the potential to grow faster.

Official per capita disposable income also rose more slowly in absolute terms from a larger base in 2022–25 than it did in 2016–19. Disposable income stood at $6,200 in 2025. This is arguably the most important figure, certainly more so than GDP per capita. GDP per capita is an accounting result of no use to individuals or households, and for the People’s Republic of China (PRC), it overstates disposable income by a factor of more than two.6 Relatedly, adjusting GDP per capita for purchasing power makes little sense, since purchasing power parity is said to be motivated by real-world prices and GDP per capita is artificial.7

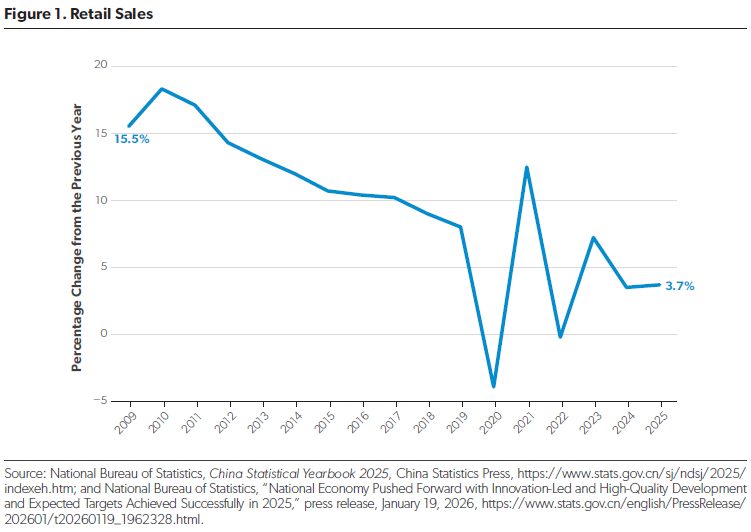

One reason for deterioration is falling prices, with the consumer price index below its 2021 level in 2025 after climbing a bit in 2016–19. The proper components of GDP are not published in comparable fashion to other data, leaving the long-standing substitutes of fixed investment, retail sales, and net goods exports. Retail sales added only 6 trillion yuan in 2022–25 combined versus nearly 10 trillion yuan in 2016– 19. (See Figure 1.) Net goods exports outperformed in the 2020s, as they actually shrank in 2019 versus 2016, while they more than doubled from 2022 to 2025. Export dependence was fairly minor as the 2010s wore on, but it has returned with a vengeance this decade.8

That’s the official picture; the true situation could be worse. There are many issues with official statistics,9 but fixed asset investment (FAI) revisions are the most important quantitatively. FAI volume in 2017 was originally put at 64.1 trillion yuan. In 2025, FAI for 2017 was put at 39.1 trillion yuan,10 a 39 percent revision down and the equivalent of $3.6 trillion “lost” at the 2017 exchange rate. One can certainly argue that the lost volume was nearly entirely fake and should have no impact on other economic indicators. And the government’s statistics show no impact. But then the indictment of data quality is so damning that it seems absurd to trust other published numbers. Stark revisions continue—fixed investment in scientific research and technical services was said to drop 15 percent in 2025.11

The other possibility is investment occurred but fared poorly over time, achieving returns far below those originally reported. Resources were wasted in enormous quantities. With mis-investment substantially financed by loans, net financial assets would be hardest hit. A financial system in worse shape than the government admits may partly explain Beijing’s unwillingness to ramp up leverage, despite being encouraged to by foreigners. Here, official GDP could be overreported back to 2003, the first year FAI was revised downward and when the economy started to become unbalanced in favor of investment. GDP overstatement is likely, though the extent of overstatement could be small if most fixed investment was empty from the start.

2026: Little Policy Change

The setting for 2026 is therefore an economy continuing to gradually fade. Excessive reliance on investment has been swapped for a return to reliance on exports,12 but partners will eventually not permit PRC production to account for a larger share of their consumption. The government’s record of data manipulation and repression clouds the picture, but it’s unlikely the data are massaged to make them look poorer.13 That leaves the situation no better than at 4 percent nominal GDP growth for 2025, slowing, and with little reason to anticipate improvement.

Popping the property bubble may have been socially or politically necessary, but the extended weakness in wealth accumulation14 naturally weakens consumption, leaving growth at the mercy of supply. The ensuing oversupply is deflationary, and the duration of deflationary effects already seen means they cannot be thrown off quickly. The same slowness applies to a cyclical property recovery. Parts of the property market have stabilized in important respects, but this is far short of an actual rebound.15 While less fear of wealth loss serves to put a floor under sentiment, it cannot by itself empower more robust spending.

There has been a great deal of talk about attempts to boost consumption directly. It first began after the 2003 investment surge failed to dissipate,16 and nearly two decades of disappointment has not dissuaded some from believing decisive action must be right around the corner. But Xi seems especially hostile to reliance on (domestic) consumption. In 2012, the last year before Xi took office, industrial production grew 10 percent while retail sales climbed more than 14 percent. In 2025, the gains were 5.9 percent and 3.7 percent, respectively.17

No policy pivot is pending. In November 2025, the government announced demand would be encouraged . . . by improving supply.18 Policies to boost consumption are typically paired with policies to boost investment,19 though the two are less complementary than competitive. High-level pronouncements praise “new productive forces” and still more output to enhance China’s role in global supply chains.20 For Xi to now shift toward consumption leadership of the economy would be abrupt and odd. An alternative might be to prioritize manufacturing but encourage modestly higher consumption through government spending such as direct transfers or larger pensions. Even if attempted, this is unlikely to succeed, due to the nature of national debt.

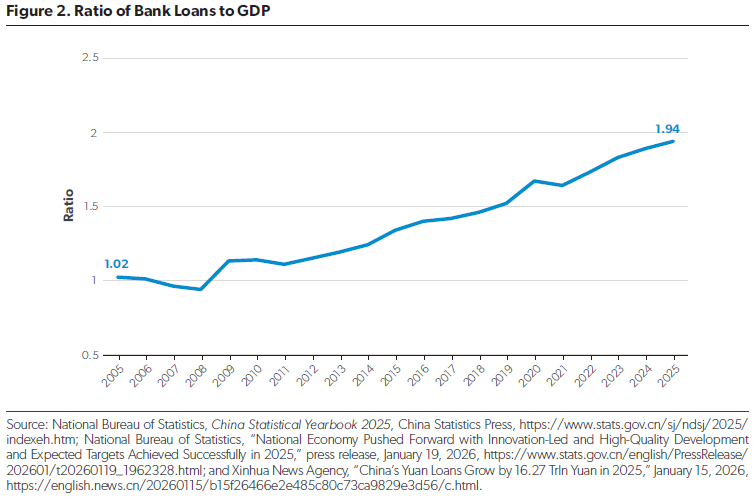

The Bank for International Settlements (BIS) put credit to the nonfinancial sector—a leveraging measure— at 133 percent of GDP at the end of 2008 and 286 percent at the end of 2024. Over this period, the same indicator for the US rose 8 percentage points.21 The PRC is a large net external creditor even as it runs up this debt; it’s been borrowing and wasting its own money. (See Figure 2.) Could Beijing thus tap still more of the huge stock of domestic savings? Yes, but this would effectively be taking from those who did not initially want to spend, giving it back to them in a new guise, and hoping they would now spend money they saved before. It’s not a sensible foundation for important policies. Unless you’re desperate.

2027–29: Property to the Rescue?

The 2027 Communist Party Congress may test whether Xi is desperate. He will be seeking years 15–20 as party general secretary, which he will almost certainly get if healthy. But it’s past time to name a successor, which Xi has refused to do. His political hand would be stronger if the macroeconomy appeared to be waxing in 2027 or at least genuinely stable, as compared with the waning seen under his rule to this point.

Xi in early 2026 seems comfortable with stressing production and technology over consumption and prosperity, so he may feel little pressure for an economic track switch by 2027. In this case, the PRC will continue toward outright macroeconomic stagnation in the 2030s (discussed below), along with further strategic success in embedding itself in global supply chains. If party leadership at some point decides action is necessary, there are three principal options: (1) reform to turn somewhat away from state direction and excess output; (2) more intense stimulus via leveraging, aimed at sentiment rather than a crisis response as seen in 2008–09; and (3) reflation of property.

Authentic pro-market reform would constitute a profound reversal for Xi, and the initial impact would include contraction at state-owned enterprises in oversupplied sectors—a political risk. Meaningful pro-market reform can be dismissed (and should have been dismissed no later than 2015).

Foreigners incessantly discuss more Chinese borrowing and spending.22 This is partly due to their disinterest in long-run costs, as seen after the 2009 monetary bonanza,23 which stabilized the economy during the global financial crisis but permanently lowered the PRC’s growth trajectory versus pre-2008 projections.24 Even the short-term benefit of such stimulus is likely to be minor, which helps explain why Beijing has ignored the chorus. As noted, China further tapping domestic savings runs into the problem of transfer recipients likely not making choices the state wants.

Japan has faced a somewhat similar situation. From 1998 to mid-2012, credit from all sectors to the Japanese government rose $8.7 trillion. From mid-2012 through 2024, it fell $4 trillion. Japan’s GDP growth was basically indistinguishable in the two periods.25 China’s long-term bond yields are now comparable to Japan’s.26 A desperate Xi could spend a lot in 2027, but Japan’s experience and the limits of Keynesian stimulus in conditions of high debt, high saving, and demographic contraction argue strongly against any important gains.

The sizable multiplier for state intervention lies in property. The central government can act directly and, more importantly, encourage local governments to act. There is a large variety of financial incentives to offer, as well as prime land owned by various government bodies. It will not be quick or easy, and announcing victory in rectifying the market would have long-term risks. But there is a quite attractive multiyear payoff: no politically wrenching reform, no explosion in low-return leveraging, and two-plus years of a property boom.

The 2028 National People’s Congress will cement the results of the 2027 Party Congress. To safely extend the boom through early 2028, property reflation could not have started in 2025—and it did not. Politically, the best timing is to attempt to reflate starting in the second half of 2026.

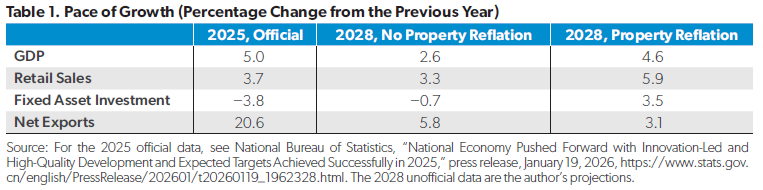

What could the result look like? The most recent year in which neither government action nor COVID hurt property was 2017. GDP growth then was in the 7 percent range. Wealth data also show a far faster rise in 2017 than, say, 2023.27 It’s quite possible property reflation would provide a sharper boost in 2027 than 2017, initially, due to the low base of activity. The wealth gains would then spur consumption, likely pushing retail sales gains temporarily toward 7 percent. (See Table 1.)

Loud crowing that “China’s back” might ensue, but the good old days would still not reach the 2030s. While politically valuable and economically notable, property reflation is unavoidably transient everywhere, and more so with a shrinking population.

2030 and Beyond: Slide to Zero

For the long term, while Xi sees technology development as primarily strategic, it could still considerably boost living standards. Research and development spending was officially put near $550 billion in 2025, on a pace to approach $800 billion in 2029. American research and development spending was $940 billion in 2023 (the latest year for which data are available),28 and China has been catching up technologically while spending less. Innovation has changed the PRC and will continue to do so.

A narrow economic assessment, however, is less encouraging. Transformative change in less than two years is a high bar, and innovation is not likely to be economically transformative in the PRC before the 2027 Party Congress. The AI industry might seem like a possible route for such change, but Chinese AI spending is less intense than American, and China trails in advanced computing.29 Rapid change also cuts against the grain of Xi’s version of the Communist Party.

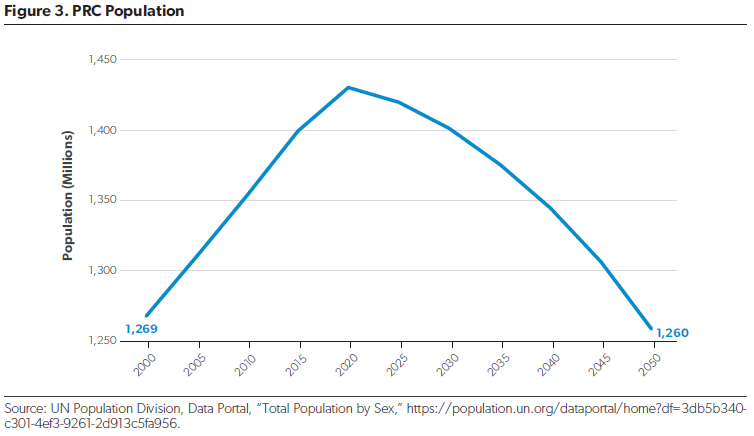

When the Party Congress recedes into the rearview mirror, the investment in broad technology would ideally pay off in elevated, sustained growth. Technological progress has already been impressive for decades, including, among many programs, Made in China 2025.30 Yet GDP and income growth have slowed over the past 15 years, earlier in the development process than for Japan and Korea.31 Eventually, technological upgrade will also slow, as the labor and capital inputs fade. (See Figure 3.) Forecast increases in median age accelerate in the 2030s, with a six-year rise over the decade to reach Japan’s 2021 level.32 Aged societies are less innovative.

The capital side is also telling. Overall fixed investment is now contracting, in part due to debt accumulation. Economically worthwhile innovation should stabilize indicators such as debt to GDP over time, as any associated borrowing brings medium-term returns. This has not happened. BIS data show credit as a share of GDP jumping from 219 percent of GDP in the second quarter of 2015 to 294 percent in the second quarter of 2025 and worsening in 2022–25—so it’s not a COVID effect.33 Innovation may accomplish many things; it has not spurred Chinese income gains and seems unlikely to do so.

Those are the fundamentals. What about new policies? If Xi departs at the 2032 Party Congress or is known to be out of power by then, Beijing could again make growth the top priority. The earlier the PRC chooses pro-growth reform, the better. But deteriorating fundamentals, especially labor in the second half of the 2030s and beyond, will limit benefits. It’s almost certain the 2030s will see notably slower growth than the 2020s, unless there are improbable and radical policy shifts such as privatizing rural land. Alternately, post-Xi policy changes little, with the state continuing to sacrifice potential growth for other priorities. Then China’s enviable strategic position survives the early phase of demographic decline, but the macroeconomic forecast is grim.

Beijing’s targets imply 4.2 percent annualized real GDP growth out to 2035.34 It’s difficult to imagine the Communist Party acknowledging sustained growth under 4 percent in the near future, since that would end the PRC’s period of exceptionalism far below rich country levels of personal income. Barring policy change, however, 4.2 percent is impossibly optimistic. Deceleration has been ongoing for 15 years now, and fourth quarter 2025 official growth was already down to 4.5 percent despite a giant trade surplus. Even (genuinely) averaging 3.2 percent out to 2035 is far from a sure thing.35

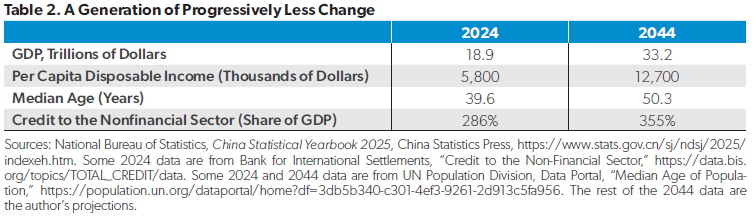

Of course, the desired figures can always be manufactured. That aside, the late 2020s could also be bolstered by property reflation, raising the decade average. When that effect wanes, and barring a radical reorientation, the 2030s will see authentic growth slowing toward frictional, ultimately approaching 1 percent annually. (See Table 2.) This will last indefinitely. Japan did not lose a decade; it has lost three decades and counting.36 China is all but guaranteed a similar outcome by its debt and, especially, demographic trajectory.37 Property reflation could help for a time, but using the present level of directly measured income and powerful reasons for poor growth, the “Chinese century” is very unlikely to ever see a rich China.

About the Author

Derek Scissors is a senior fellow at the American Enterprise Institute, where he focuses on the Chinese and Indian

economies and US economic relations with Asia. He is concurrently the chief economist of the China Beige Book.