The American and Israeli war against Iran has propelled oil above $119 a barrel this week—prices not seen since Russia’s full-scale war on Ukraine in 2022. Bahrain, Iraq, Kuwait, Saudi Arabia and the United Arab Emirates have all cut production because of damage or logistics constraints that limit their ability to transport crude to international markets. This has removed an estimated 6.2m-6.9m barrels per day of regional supply from the market—around 6-7% of global oil output. Limited oil storage capacity in the region and relatively low oil reserves in the US are exacerbating the issue.

Although the EU does not purchase significant amounts of oil and gas from Middle Eastern countries, its real vulnerability lies in indirect shocks: Asian competition to replace the missing Gulf supplies and resurgent Russian leverage. This crisis, far from derailing diversification of energy sources, demands that the EU double down on it.

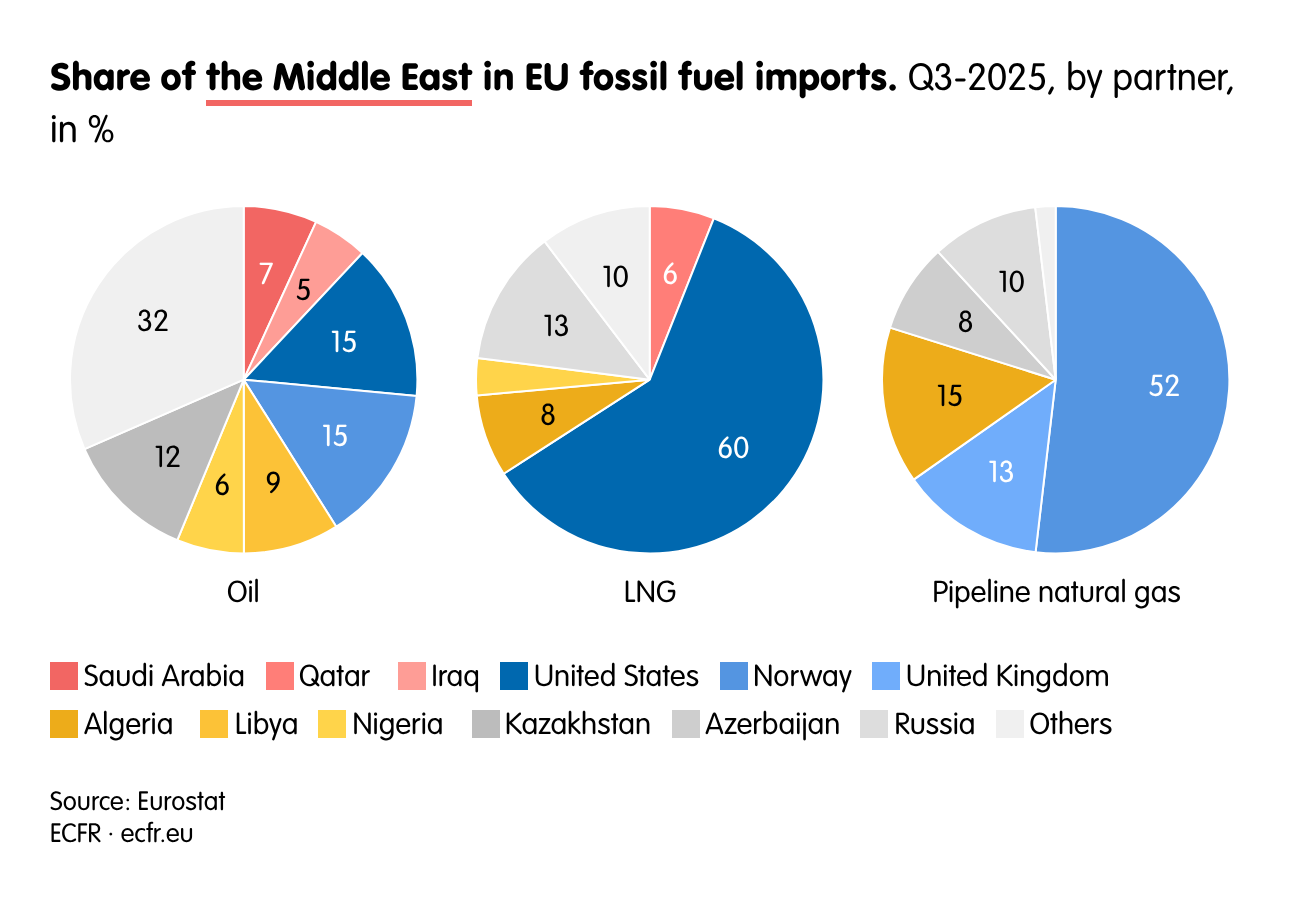

Low direct dependence

The Iran war poses little direct threat to EU fossil fuel supplies. Oil and gas account for 90% of the EU’s energy imports (covering more than half of the bloc’s energy needs), but in 2025, the EU imported only 3.5% of its gas from Qatar, the Middle East’s largest gas exporter. Norway provides most of the EU’s pipeline gas and America nearly 60% of the liquefied natural gas (LNG).

The situation is similar for crude oil. In 2025, EU countries imported a mere 6% of their crude oil from the Middle East—around 25.2 million tons.

Never free

Direct risks aside, indirect ones bite harder. Turbulence in global markets hits the EU via higher prices and Asian competition for supplies. The Middle East region plays an important role in supplying oil and gas to Asian countries; some 60% of Middle Eastern crude goes to Asia, and more than 80% of Qatari LNG goes to Asian buyers.

Restrictions or suspensions of Gulf exports will force Asian countries to seek alternatives, pitting them against European consumers and driving up energy prices. QatarEnergy, one of the world’s top LNG producers, suspended production and exports last week, and the Qatari energy minister warned there could be a complete halt in LNG exports from the Gulf countries, which could exacerbate the crisis not only in Asia but also in the EU. Gas prices in Europe have already climbed to their highest level since 2023, though they are still well below 2022 peaks.

The intensifying crisis could revive calls in some European capitals to pause the EU’s push to end fossil-fuel imports from Russia. The EU finally enacted a regulation in January banning Russian LNG imports from January 2027 and pipeline gas by autumn 2027; an oil ban proposal is due to follow in April. Russian leaders, for their part, have threatened over the past week to cut gas supplies to the EU before the bloc’s deadline to end Russian imports. Russia may well decide to reduce or suspend LNG supplies to Europe in the coming months, which could tighten the energy squeeze further.

Within the EU’s hands

The EU has few quick fixes, but there are a couple of things it can do. It should back moves to curb American and Israeli military action and initiatives to restore safe passage for fossil fuel exports through the Strait of Hormuz. Diplomatic outreach should be directed not only towards the US, but also towards India, China and countries in the Middle East, whose greater dependence on fossil fuels from the region will motivate them to act, either to end the conflict or mitigate the impact of high prices. An important immediate step is the G7 consultation on releasing oil reserves, which could slow the global price surge driven by the shortages.

The EU should stick to its plan to phase out fossil fuel imports from Russia

At the same time, the EU should stick to its plan to phase out fossil fuel imports from Russia. The European Commission must press member states to end gas imports fully and meet the timetable for banning Russian oil. Far from derailing this course, the current crisis strengthens the case for ditching unreliable suppliers. Vladimir Putin is already trying to stop Europeans from pressing ahead with it by both threatening to divert the remaining LNG supplies away from Europe and enticing Europeans with increased energy exports if they show willingness to resume long-term cooperation.

In the long term, the EU and its member states should press ahead with transitioning away from oil and gas. And should use the Iran conflict to frame the energy transition as a pragmatic choice: one that curbs dependence on fossil fuels and, with it, the political and economic costs of market turbulence.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.