Attention turns to a packed central bank calendar: the Bank of Canada (BoC) and the Federal Reserve (Fed) on Wednesday, followed by the Bank of Japan (BoJ), Swiss National Bank (SNB), Riksbank, Bank of England (BoE) and European Central Bank (ECB) on Thursday. How will they respond to the energy shock triggered by the Iran crisis, and is there a risk of currency intervention?

Over the next two sessions, a series of monetary policy decisions will take place as central banks confront a potential rebound in inflation driven by the current energy shock.

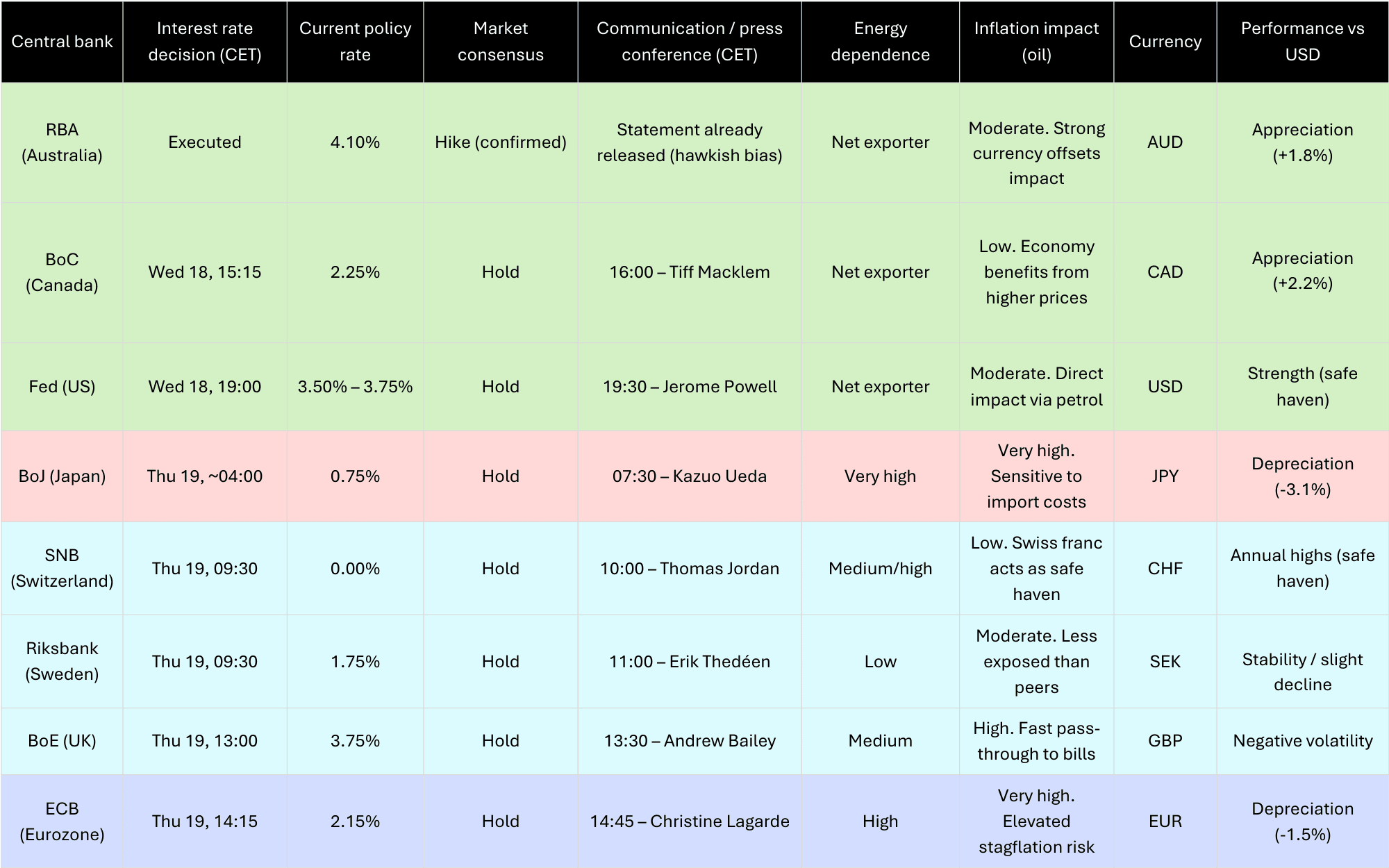

Below is a detailed calendar of upcoming monetary policy decisions, alongside each region’s energy dependence, the potential impact on inflation and currency performance since the start of the hostilities.

Methodological note: Table generated using artificial intelligence (AI). Consensus data sourced from Trading Economics; energy dependence data from the World Energy Balances of the International Energy Agency (IEA) and Eurostat.

Upcoming monetary policy decisions and energy vulnerability

Market consensus points to broadly unchanged rates, which should not be mistaken for indecision. Following the rise in oil prices, rate curves have already priced in a geopolitical risk premium, and reactive overtightening by central banks could prove counterproductive by overreacting to a supply-side shock.

The focus is not on the nominal rate decision, but on forward guidance. The Reserve Bank of Australia (RBA) has set the tone: after delivering its hike, it anchored swap expectations by conditioning future action on Brent not consolidating above $110 per barrel. Markets are now looking for a similar “tolerance threshold” from other policymakers.

A key divergence lies in each economy’s net energy position. The decisions from the Fed and BoC on Wednesday appear more manageable; as net exporters, they benefit from favourable terms of trade that support their currencies and help offset imported inflation.

At the other end of the spectrum, the ECB and BoJ, both meeting on Thursday, face greater technical challenges. Their economies are structurally dependent on energy imports, and rising oil prices feed quickly into industrial costs and consumer prices, putting pressure on long-term inflation expectations.

The vulnerability of the eurozone and Japan is compounded by currency dynamics. With starting rates still low in real terms relative to the US dollar, the yield gap puts downward pressure on both the euro (EUR) and Japanese yen (JPY).

In a rising oil environment, this depreciation amplifies the energy shock, as oil becomes more expensive both in dollar terms and due to weaker domestic purchasing power.

For the BoJ, the situation is particularly acute. Following a -3.1% depreciation since the start of the conflict, markets are not only focused on Thursday’s policy statement but are also watching for potential direct foreign exchange (FX) intervention, as the yen retests historic lows against the US dollar (USD).

Bank of England – restrictive policy for longer

The Bank of England sits in a middle ground, but the challenge remains significant. Despite domestic production in the North Sea, the UK remains a net energy importer and is sensitive to rising energy prices.

With interest rates at 3.75%, Andrew Bailey has limited room for manoeuvre. The risk is that already elevated services inflation becomes entrenched. The BoE may therefore be forced to maintain a restrictive stance for longer, which could weigh on growth. This week, UK gilt yields have already moved above 4.80%.

Unlike others, these two central banks operate under dynamics shaped by safe-haven flows and structural resilience.

Swiss National Bank (SNB): Although Switzerland is an oil importer, the Swiss franc (CHF) acts as a primary safe-haven currency. Its appreciation partially offsets the rise in oil prices, allowing the SNB to keep rates at 0.00% with relative flexibility. However, excessive strength in the CHF could undermine external competitiveness, raising the possibility of intervention to limit further appreciation.

Riksbank (Sweden): The Riksbank operates in a hybrid environment. Sweden benefits from one of the lowest levels of energy dependence in Europe due to its nuclear and hydroelectric mix, providing partial insulation from the oil shock. However, the Swedish krona (SEK) is not a safe-haven currency. The Riksbank may need to adopt a more hawkish stance if currency weakness begins to import inflation and offset its structural advantage.