Find winning stocks in any market cycle. Join 7 million investors using Simply Wall St’s investing ideas for FREE.

Google released its TurboQuant AI memory compression algorithm, which is designed to reduce the memory requirements of large AI models.

The announcement has raised new questions about long term AI memory demand for suppliers such as Micron Technology (NasdaqGS:MU).

Memory stocks, including Micron, sold off as investors reassessed whether memory will remain the main bottleneck for AI workloads.

At the same time, SK Hynix is preparing a U.S. ADR listing and expanding capacity, signaling more direct competition in AI focused memory.

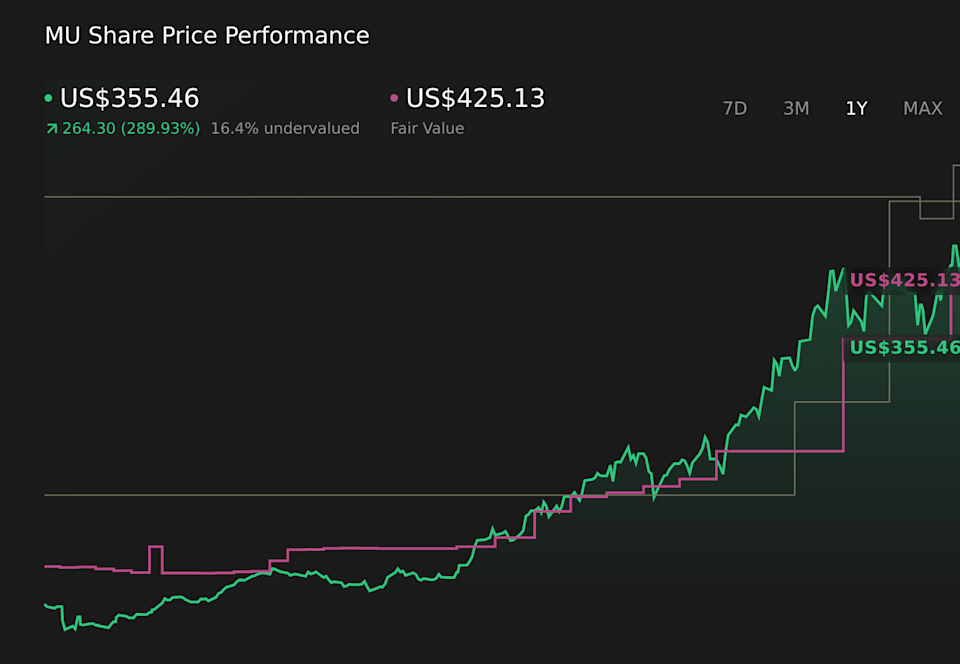

Micron Technology enters this news cycle after what has been described as exceptional quarterly growth tied to AI demand, with shares at $355.46 and very large 1 year and 3 year share price gains. Even with that strength, the stock is currently down 15.9% over the past week and 17.1% over the past month, and still up 12.7% year to date. That mix of sharp recent declines and very strong multi year gains puts Micron in the spotlight as investors reassess expectations for AI related memory demand.

For readers following NasdaqGS:MU, the key question is how much algorithms like TurboQuant could change the balance between AI compute and memory needs over the medium term. SK Hynix’s planned U.S. listing and capacity build out adds another layer, as it could influence pricing power and market share across high bandwidth and AI centric memory. How these factors evolve is likely to shape sentiment around Micron and its peers well beyond the next earnings print.

Stay updated on the most important news stories for Micron Technology by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Micron Technology.

NasdaqGS:MU 1-Year Stock Price Chart

NasdaqGS:MU 1-Year Stock Price Chart

Micron’s decision to launch cash tender offers for up to US$5.4b of senior notes sits in the background of the TurboQuant shock and SK Hynix’s planned U.S. listing. On one hand, retiring 5.3% to 6.05% coupon debt maturing between 2031 and 2035 can lower future interest expense and simplify the balance sheet, which matters as Micron lifts capital expenditure to more than US$25b in fiscal 2026. On the other hand, funding both aggressive HBM and fab build outs and a large debt repurchase requires strong and consistent cash generation. For you as an investor, the key question is whether it makes sense for Micron to commit cash to debt reduction at the same time AI memory demand is being questioned by compression techniques like TurboQuant and new capital access for SK Hynix. If memory pricing or volumes soften, Micron could have less balance sheet flexibility to respond. If cash flows stay robust, the company could exit this investment cycle with lower debt and a larger high bandwidth and data center footprint, but the path depends heavily on how AI memory demand and competitive intensity from Samsung, SK Hynix and others develop from here.

The tender offers align with the narrative that Micron wants to keep a strong balance sheet while investing heavily in HBM and advanced nodes, helping it stay a key supplier to AI data centers.

Heavy capex combined with significant cash outlay for debt repurchases could strain free cash flow, which the narrative already flags as a risk in a high-investment phase.

The narrative focuses on AI-driven demand and competition from Samsung and SK Hynix, but it does not fully factor in how new algorithms like TurboQuant might alter long term memory intensity for AI workloads.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Micron Technology to help decide what it’s worth to you.

⚠️ Analysts have highlighted a high level of non cash earnings, which can make it harder for you to judge how much of Micron’s recent profitability is translating into sustainable cash flow that can support debt reduction and capex.

⚠️ TurboQuant and SK Hynix’s capacity expansion could pressure AI memory pricing over time, which may weigh on margins if Micron’s spending plans and debt profile are built around very strong demand assumptions.

🎁 Earnings grew very strongly over the past year and are forecast to grow further, giving Micron more room to fund both capex and debt tenders if current conditions hold.

🎁 The P/E of 16.6x is below the broader U.S. market at 18.4x, and analysts see the company as offering good relative value compared to peers, which may appeal to investors who accept the sector’s cyclicality.

From here, keep an eye on three things. First, how much of the US$5.4b in notes Micron actually repurchases and what that does to interest expense and net debt. Second, any updates to capex plans if AI memory demand expectations change in response to TurboQuant or GPU vendor roadmaps from Nvidia, AMD and others. Third, commentary on long term customer contracts and pricing for HBM and data center DRAM, especially as SK Hynix pursues a U.S. listing and more funding. Together, these data points will show whether Micron is maintaining enough financial flexibility while funding its AI build out.

To stay informed on how the latest news impacts the investment narrative for Micron Technology, head to the community page for Micron Technology to follow the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include MU.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com