Market_Recon_TSP1_KL

Market_Recon_TSP1_KL

Enter Sandman

Sleep with one eye open

Gripping your pillow tight

Exit light

Enter night

Take my hand

We’re off to never-never land

– Hetfield, Ulrich, Hammett (Metallica), 1991

Not as Planned?

That depends on who expected what. Off to never-never land. Markets had priced in a victory speech, which is sort of what they got. Sort of. Markets expected to hear that the end of the war in Iran was imminent. Crude oil prices had eased. Equity prices had rallied. That was not what they got.

Oh, the president of the United States did convey to listeners that this war would end soon enough, but he added that there would be an increase in the pace of kinetic activity first. Markets had not anticipated this. Crude oil is trading much higher on Thursday morning. Treasury yields are higher. Gold and Bitcoin are trading lower. Oh, and equity index futures are being slapped around as well.

President Trump told Americans that the war in Iran would last another two to three weeks, He stated, “We are going to finish the job, and we’re going to finish it very fast.” The president also said, “Over the next two to three weeks, we’re going to bring them back to the stone ages where they belong.” Tell us how you really feel. Some folks like this president. Many folks do not. You never really have to wonder for too long what exactly is on his mind. He’ll tell you and he’ll be blunt.

The Nitty Gritty

The entire speech lasted only 19 minutes. Perhaps what financial markets, especially commodity markets liked the least was the lack of clarity concerning the re-opening of the Strait of Hormuz. We have definitely seen some cargo moving through that narrow and vital stretch in recent days and it does appear that Iran’s offensive capabilities are waning. That said, the president challenged America’s traditional allies to “take the lead” in clearing that waterway.

Regarding the Strait, which supplies the world with oil, but not the U.S. so much, the president commented, “The countries of the world that do receive oil through the Hormuz strait must take care of that passage. They must cherish it. We will be helpful, but they should take the lead in protecting the oil that they so desperately depend on.” Pres. Trump added that the U.S. campaign had decimated Iran’s defenses to the point that “it should be easy” for allies to re-open the strait.

President Trump also renewed his aggressive tone in threatening to take out Iran’s ability to generate electric power in the coming days should leadership in that county fail to agree to an acceptable deal. The president stated that the U.S. military would strike “each and every one of their electric-generating plants very hard and probably simultaneously,” while hinting that oil industry-related facilities might be taken out as well.

Related: Investors Sell the News as Uncertainty Roars Back After Trump’s Speech

Paint it Black

I see a red door

And I want to paint it black

no colors anymore

I want them to turn black

Jagger, Richards (The Rolling Stones), 1966

Bottom Line

While the president did tell Americans that the war was close to an end, and there is evidence in the field that supports that, the speech was more than escalatory in nature. The president sounded angry. Angry with Iran. Angry with America’s traditional allies. For markets, the bottom line is this: The war will go on for “at least” another two to three weeks and traversing the Strait of Hormuz will remain risky. That is why oil prices are soaring this morning and that is why equity index futures and risk asset prices in general, are trading sharply lower.

On Economics

There was some solid news on the economic front released on Tuesday. This was welcome as the pace of growth in economic activity slowed in late 2025. First up was the ADP Employment Report on private sector job creation for March, which matters because the broader Bureau of Labor Statistics survey data for March will be released on Friday with financial markets closed. The ADP Report showed an increase of 62,000 private sector jobs across the nation for the month, easily beating expectations for something down around 40,000. February private sector jobs were also revised slightly higher.

Next up was the retail sales report for the month of February, released by the Census Bureau. For that month, headline-level retail sales grew 0.6% on a month-over-month basis, beating expectations for growth of 0.4% and up from a nasty -0.1% print for January. Excluding autos and auto parts, retail sales were up 0.5%. What was hot? Health and personal care products, as well as clothing and apparel, which is a little odd for the dead of winter. Grocery sales contracted. I thought that odd as well as those are non-discretionary items.

Perhaps most encouragingly, the line-item that I refer to as the “fun index” was hot. Now, the fun index includes things like sporting goods, hobbies, music and books. These are things that folks do not purchase when they are broke. This category ran up 1.3% for February at a time that the economic data was supposedly weakening. These conditions cannot co-exist. Understand?

Either the economy is tough and folks are not increasing their purchases of discretionary items or the economy is acting well and they are. You don’t spend money on your hobbies at the opportunity cost of feeding your family less, which is what happened in February, unless you are confident in the economy and in your role in it.

ISM: Good and Not-So-Good News

The Institute of Supply Management’s March Survey of Manufacturing Sector Purchasing Managers saw almost every key category improved from February: new orders, production, deliveries and backlog of orders. Two problems, however, were manufacturing-based employment contracted for a 30th consecutive month while prices (inflation) accelerated to the upside, outpacing the gains made in all of the positive categories.

On that note, the Cleveland Fed updated its forecasts this week for March and April consumer-level inflation. Cleveland now sees March consumer price index at month-over-month growth of 0.8% at the headline and 0.2% at the core. On a year-over-year basis, Cleveland sees March CPI growth at 3.25% (headline) and 3.6% (core). April is seen spiking to 3.71% at the headline but holding at 2.56% at the core.

Quote of the Day

“There are not enough Indians in the world to defeat the Seventh Cavalry.”

– George Armstrong Custer

Tuesday

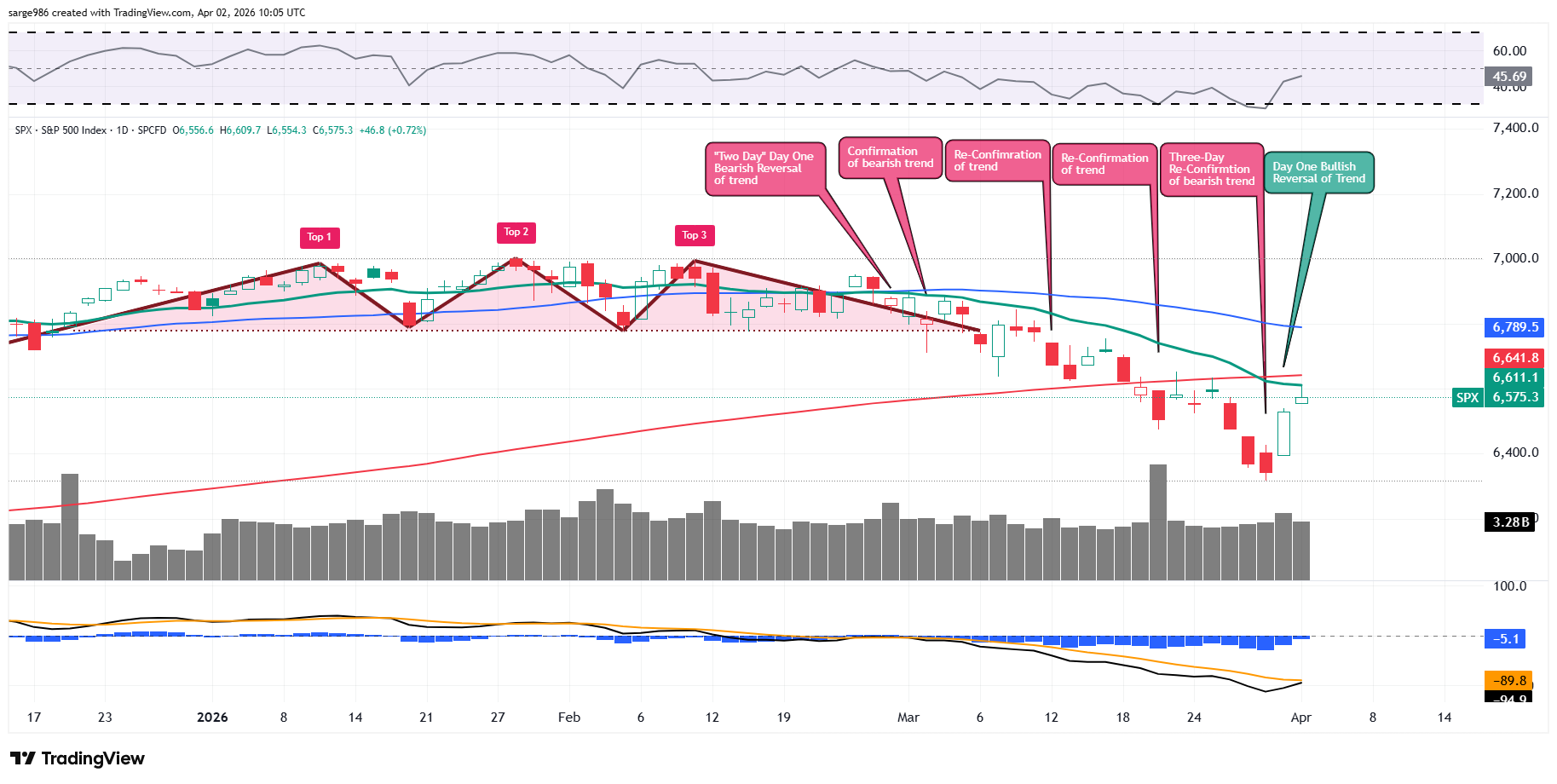

Readers will see that on Tuesday, the S&P 500, while posting a second consecutive day of strength, was rejected at its 21-day exponential moving av. This implies that swing trades took a pass on joining in on the day’s fun. Trading volumes also tailed off ahead of the president’s address, suggesting a lack of confidence late in the day. Note also that within the daily moving average convergence divergence, the 12-day exponential moving average never did reach the 26-day EMA.

That crossover had been imperative for the index to make a run at its all-important 200-day simple moving average, which is where portfolio managers will be forced to choose sides. The game is all about headline risk right now and headlines can change rapidly. That said, it looks like the S&P 500 is going to get its “pause” on Thursday. At a minimum. If trading volumes remain light, the attempted bullish reversal might live to resume the fight next week. Guess we’ll know which way the wind blows later on today. Happy Easter. Happy Passover. God bless.

Economics

(All Times Eastern)

08:30 – Initial Jobless Claims (Weekly): Expecting 214K, Last 210K.

08:30 – Continuing Claims (Weekly): Last 1.819M.

08:30 – Balance of Trade (Feb): Last $-54.5B.

10:30 – Natural Gas Inventories (Weekly): Last -54B cf.

The Fed

(All Times Eastern)

11:00 – Speaker: Dallas Fed Pres. Lorie Logan.

Today’s Earnings Highlights

(Consensus EPS Expectations)

Before the Open: (AYI) (4.06)

At the time of publication, Guilfoyle was had no position in any security mentioned.