American Airlines Group, NasdaqGS:AAL, has publicly rejected the idea of a merger with United Airlines. The company cited antitrust and competition concerns, emphasizing potential impacts on consumers. Management reiterated a focus on pursuing its own independent plans rather than large scale airline consolidation.

For investors tracking NasdaqGS:AAL, this announcement comes with the share price around $12.78 and a value score of 1. Over the past week the stock return is 12.9%, and over the past month it is 22.5%, while the year to date return shows a 17.4% decline. Over longer periods, the stock return is 35.1% over 1 year, a 4.6% decline over 3 years, and a 39.5% decline over 5 years.

This clear rejection of a merger indicates that American Airlines Group intends to pursue its own path rather than large scale consolidation with a major peer. For investors, the update helps frame expectations around potential future M&A activity and where leadership attention is likely to stay focused. It also adds another data point to how large carriers present their views on competition and regulation.

Stay updated on the most important news stories for American Airlines Group by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on American Airlines Group.

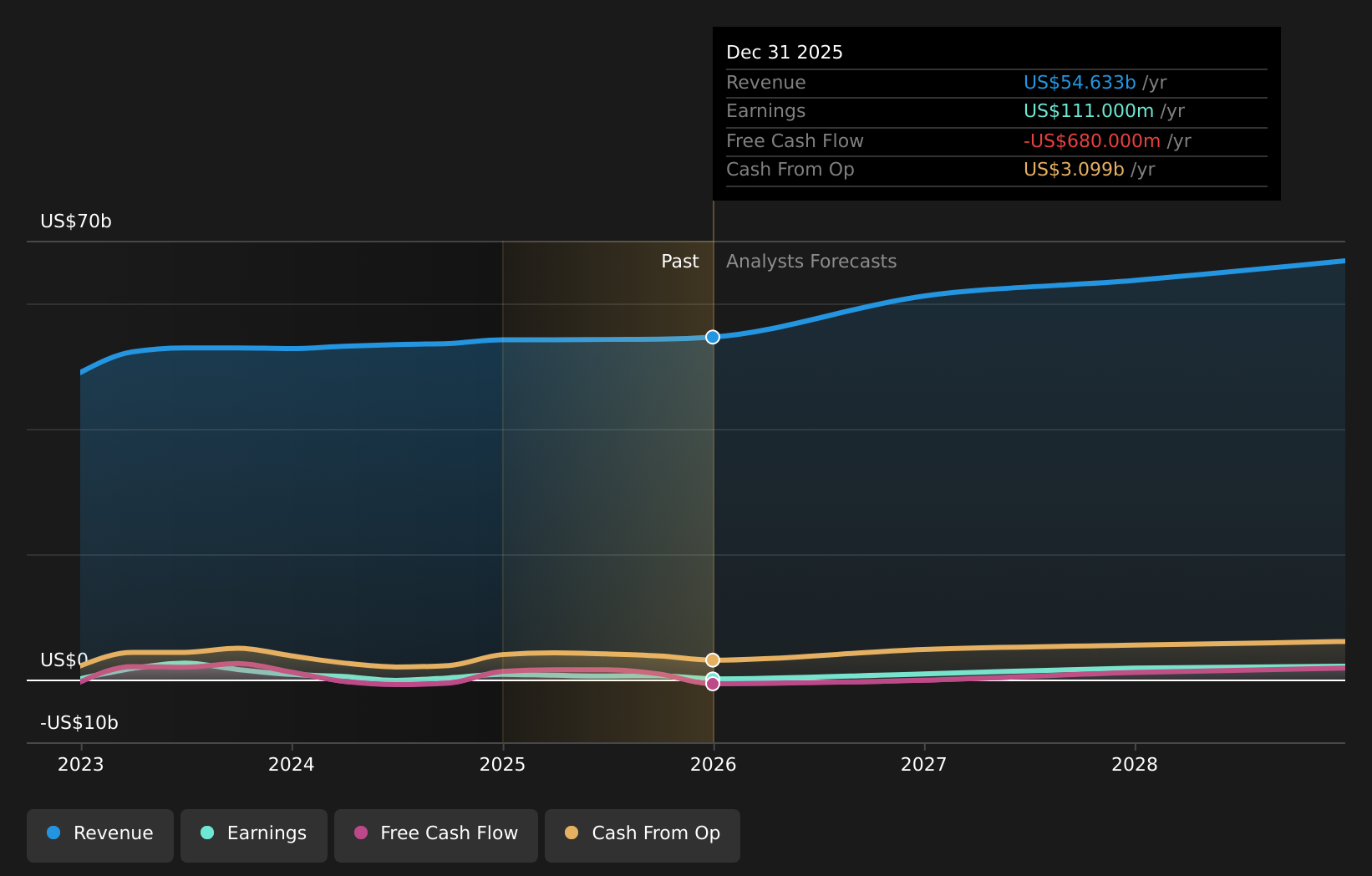

NasdaqGS:AAL Earnings & Revenue Growth as at Apr 2026

NasdaqGS:AAL Earnings & Revenue Growth as at Apr 2026

We’ve flagged 4 risks for American Airlines Group. See which could impact your investment.

American’s firm rejection of a merger with United puts a clear marker down on how it wants to compete. Rather than pursuing scale for its own sake, management is signaling confidence in the current business model, including the AAdvantage ecosystem, corporate travel relationships and initiatives such as sustainable aviation fuel and private-jet partnerships. For you as an investor, this narrows the range of potential outcomes: instead of a complex, high risk integration with United, the focus stays on execution, debt management and improving returns from the existing network. It also reduces near term regulatory uncertainty that a tie up of two mega carriers would likely create, while still keeping American directly exposed to competitive pressure from United, Delta Air Lines and Southwest Airlines as separate rivals.

How This Fits Into The American Airlines Group Narrative The decision to stay independent lines up with the existing narrative that leans on domestic strength, premium service investments and loyalty growth as key drivers, rather than transformational M&A. Scott Kirby’s scale argument challenges that thesis by suggesting cost pressures and global competition could favor a larger combined carrier. This raises questions over how far American’s current plan can offset fuel, labor and debt headwinds. The public antitrust focus in American’s statement, and potential legal pushback from state attorneys general, is not explicitly integrated into the earlier narrative, which concentrates more on demand, costs and capital structure.

Knowing what a company is worth starts with understanding its story.

Check out one of the top narratives in the Simply Wall St Community for American Airlines Group to help decide what it’s worth to you.

The Risks and Rewards Investors Should Consider ⚠️ American already carries sizeable debt and has negative shareholders’ equity, so staying independent keeps full responsibility for financing future aircraft, fuel and product investments without the potential balance sheet support of a partner. ⚠️ Analysts have flagged 4 key risks for American, including interest payments that are not well covered by earnings, which could matter more if competitive pressure from United, Delta and Southwest limits pricing power. 🎁 Keeping the United proposal at arm’s length avoids the execution, cultural and systems risks that come with integrating two large network carriers, as well as the possibility of restrictive antitrust remedies. 🎁 Management’s emphasis on loyalty partnerships, premium products and sustainable aviation fuel arrangements suggests a consistent plan to grow higher margin revenue streams within the existing network structure. What To Watch Going Forward

From here, watch how clearly American reiterates this position on future calls or in filings and whether any board level commentary leaves the door open to other forms of consolidation, such as joint ventures. Pay attention to how United, Delta and Southwest respond through their own capacity, pricing and partnership actions, as that will frame the competitive pressure American faces without a merger. It is also worth tracking progress on AAdvantage partnerships, sustainable aviation fuel projects and debt metrics, because these factors will influence how investors judge the credibility of American’s stand alone plan.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for American Airlines Group, head to the

community page for American Airlines Group to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com