At the Barclays 23rd Annual Global Financial Services Conference, Wells Fargo & Company WFC provided a strategic overview of its performance and future direction.

Wells Fargo’s Growth Outlook

WFC’s chief financial officer, Mike Santomassimo, noted that the bank expects to post 2025 net interest income (NII) in line with 2024’s $47.7 billion. He also noted that the current efficiency ratio of 63-64% should improve as profitability increases. The company’s outlook is underpinned by stable deposit trends, healthy consumer activity, continued loan growth, and the ability to pursue growth opportunities aggressively, thanks to the recent removal of a long-standing asset cap barrier that had previously restricted expansion.

Wells Fargo’s peers, Bank of America BAC and Citigroup C, expect their NII to rise. BAC expects NII (FTE basis) to grow sequentially to $15.5-$15.7 billion in the fourth quarter of 2025. Hence, NII is projected to rise 6-7% in 2025. Then again, C projects NII (excluding Markets) to rise 4% on a year-over-year basis in 2025.

WFC’s Strategic Overview

A central theme of the update was the Federal Reserve’s asset cap, which restricted growth for seven years. Management emphasized a pivot from regulatory remediation to growth, particularly across commercial banking, corporate and investment banking, and wealth management. The bank has already streamlined operations by exiting 13 businesses and generating $12 billion in cost savings, which are being reinvested into core operations.

With the Federal Reserve’s asset cap now lifted, management emphasized a strategic shift from regulatory remediation to organic growth, particularly in commercial, corporate investment banking, and wealth management spaces.

The bank is focusing on expanding market share in both consumer and commercial lending, making it more competitive and agile in adapting to evolving market demands.

The company signaled a “high bar” for acquisitions and will prioritize organic growth, with increased marketing spend aimed at growing both consumer and commercial deposits.

Capital management remains central to the bank’s strategy. Santomassimo confirmed that Wells Fargo will continue to return capital through share repurchases, balancing buybacks with reinvestment opportunities and disciplined risk assessment.

Final Words on Wells Fargo

With the asset cap lifted, WFC has shifted from a period of regulatory constraint to one of active expansion. Supported by stable net interest income, improving efficiency, and disciplined capital management, the bank is positioned to strengthen its competitive standing and enhance shareholder returns. Management’s focus on organic growth, cost discipline, and targeted reinvestment provides a clear path to sustainable performance in 2025 and beyond.

WFC’s Price Performance & Zacks Rank

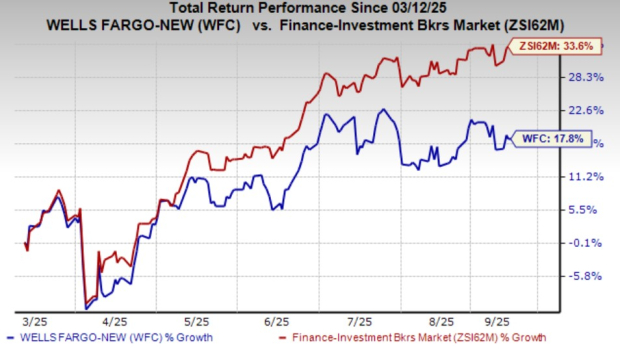

Shares of Wells Fargo have gained 17.8% in the past six months compared with the industry’s rise of 33.6%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Currently, WFC carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers “Most Likely for Early Price Pops.”

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.5% per year. So be sure to give these hand picked 7 your immediate attention.

Bank of America Corporation (BAC) : Free Stock Analysis Report

Wells Fargo & Company (WFC) : Free Stock Analysis Report

Citigroup Inc. (C) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.