In recent trading, Westpac Banking came under pressure as investors reacted cautiously to upcoming Australian December‑quarter inflation data and the Reserve Bank of Australia’s pending policy decision. This macro focus matters for Westpac because inflation and rate outcomes directly influence its net interest margins, funding costs and credit growth outlook. We’ll now examine how this inflation‑driven focus on future RBA decisions could shape Westpac’s investment narrative for shareholders.

Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

What Is Westpac Banking’s Investment Narrative?

To own Westpac today, you really need to believe in the durability of its core Australian banking franchise, its ability to translate modest revenue and earnings growth into consistent dividends, and the discipline behind ongoing buybacks that have already reduced the share count by roughly 2.5%. The recent share price dip around the December‑quarter CPI release and the RBA’s upcoming decision feels more like a sentiment reset than a change in fundamentals, but it does put short term catalysts such as net interest margin trends and the February trading update under a brighter spotlight. A hotter or cooler inflation print could shift expectations for funding costs and credit growth, which matters for a bank already priced above some cash flow estimates and with a relatively new board and management team still proving themselves.

However, investors should be aware of how low bad loan coverage could amplify any credit cycle turn.

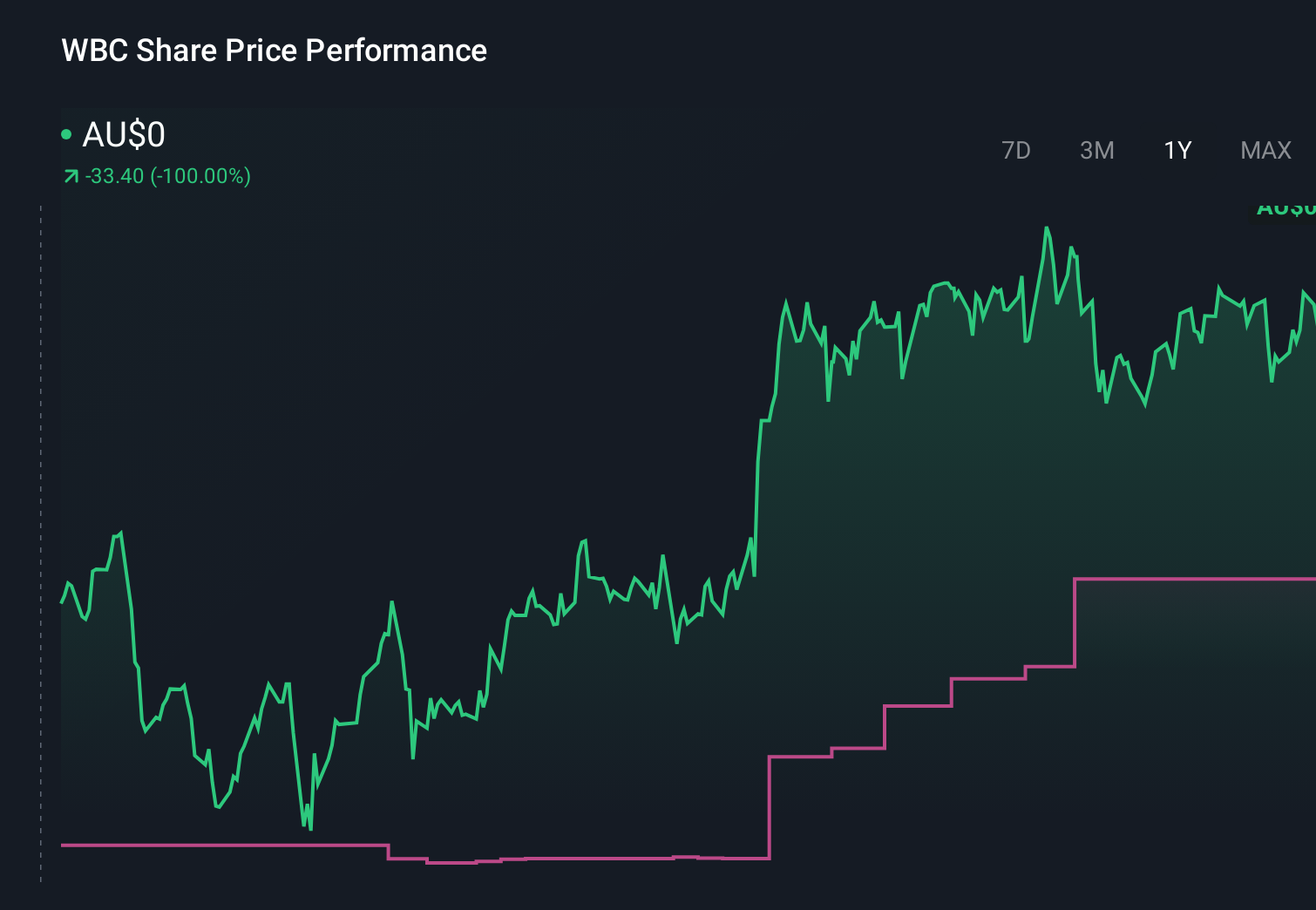

Westpac Banking’s shares are on the way up, but they could be overextended by 18%. Uncover the fair value now.Exploring Other Perspectives ASX:WBC 1-Year Stock Price Chart Simply Wall St Community members put Westpac’s fair value between A$27.95 and A$36.45 across 9 views, underscoring how far opinions can diverge. Set those against today’s macro driven focus on margins and credit quality, and it becomes even more important to weigh several perspectives on how inflation and RBA policy might influence the bank’s next phase.

ASX:WBC 1-Year Stock Price Chart Simply Wall St Community members put Westpac’s fair value between A$27.95 and A$36.45 across 9 views, underscoring how far opinions can diverge. Set those against today’s macro driven focus on margins and credit quality, and it becomes even more important to weigh several perspectives on how inflation and RBA policy might influence the bank’s next phase.

Explore 9 other fair value estimates on Westpac Banking – why the stock might be worth as much as A$36.45!

Build Your Own Westpac Banking Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don’t miss this chance:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Westpac Banking might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com