![]()

$230.70. That’s it.

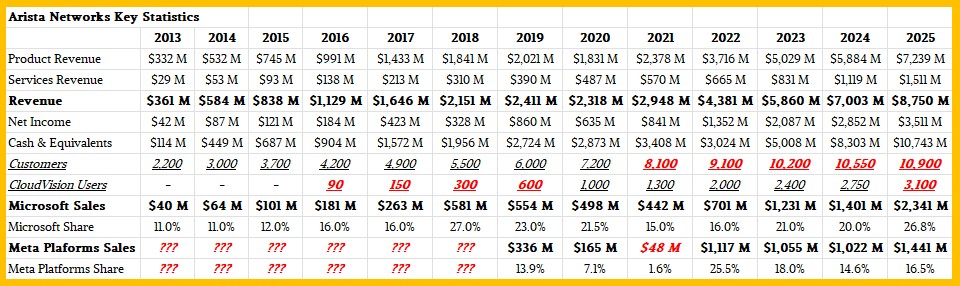

If you take the $34.6 billion that Arista Networks has made in product revenue since it was founded way back in 2004 by Andy Bechtolsheim, David Cheriton, and Kenneth Duda and divide it by the 150 million cumulative ports that it has shipped (with the product ramp really starting in 2010 after the company dropped out of stealth mode in 2009) This is a remarkable number give the fact that Arista has tended to ship very expensive ports that often cost $1,000 or more without services on top of them.

It looks like somebody has been getting some very deep discounts on those ports, and it also looks like the big customers using Arista switches are not paying for the network operating system, which represents more than half the value of the switch back in the old days before we started disaggregating the software from the switch.

And even if you layer on the costs of the $6.4 billion in services that Arista has sold over that time – call it a decade and a half for the bulk of those services sales – then that still only drives it up to $273.60 per port.

And still, when it comes to high speed ports, Arista has been able to eat a lot of the lunch and some of the dinner of Cisco Systems, and it is Arista’s championship of merchant silicon and its willingness to support the network operating systems created by the hyperscalers and cloud builders that has compelled Cisco to launch its Silicon One effort and also to create special whiteboxes (the Cisco 8000 series) that it can sell against Arista switching and routing iron.

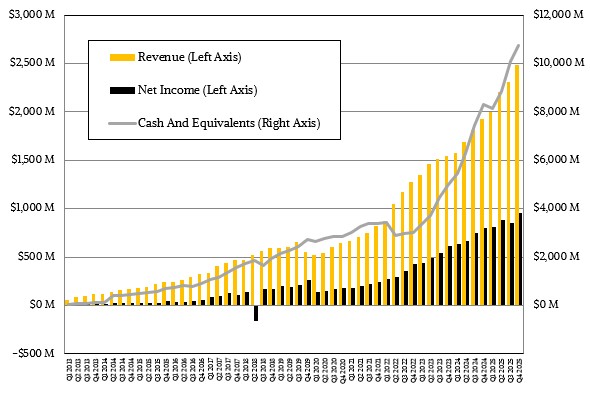

As far as we can tell from the financial report released by Arista this week, the business of this company is accelerating and it will be breaking through $10 billion a year in sales two years early. (Which is what chief executive officer Jayshree Ullal said could happen a few months ago.) Back end and front end networks in AI systems – the former being used to glue together compute engines, the latter being used to feed data from the outside world into those clusters – are driving revenues and perhaps profits.

But Arista’s nascent campus switching business is hitting its targets and its core cloud and hyperscale switching market – the one that the company was founded to take on – is stable over the long view of a few years, its routing business is growing in the double digits, and its edge business is chugging along. And it looks like these trajectories will keep going out into 2026 and beyond.

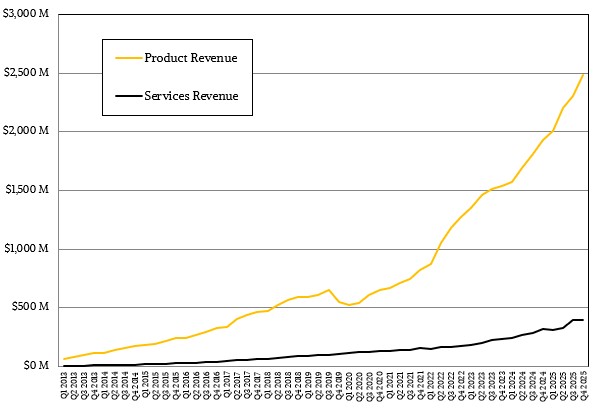

In the quarter ended in December, Arista had a tad under $2.1 billion in product revenues, up 30.3 percent, with services revenues growing at a 21.6 percent clip to hit $392.1 million. Software and services together came to 17.1 percent of revenues, which works out to $425.4 million, up 20.4 percent, and if you back out software subscriptions, you get $33.3 million in the December quarter, up only 7.7 percent.

Like we said, the big customers who have spent a fortune on NOS software and telemetry and management tools for their datacenters are not using Arista’s EOS stack, so the subscription revenue is low. But that does not mean that the vast majority of Arista’s more than 10,000 customers (we think it is very close to 11,000 customers) are not using its Extensible Operating System. It is hard to say if it is a majority by customer or not. What does matter is that Arista is agnostic when it comes to NOSes. In fact, it lets customers pick their NOSes. (You know what they say: You can pick your friends, you can pick your NOS, but you can’t pick your friend’s NOS. . . . )

Total revenue for Q4 2025 was $2.49 billion, up 28.9 percent, operating income was $1.03 billion, up 29.2 percent, and net income was $956 million, up 19.3 percent and representing a very healthy 38.4 percent of revenue (a little less than average, frankly).

Of the slightly more than $9 billion in sales that Arista had for 2025, 48 percent of that came from the “cloud titans,” what we call the hyperscalers and cloud builders. That works out to $4.32 billion, up 28.6 percent compared to 2024’s sales to these elite customers. Enterprise & Financial customers represented 32 percent of the Arista pie in 2025, which works out to $2.88 billion, up 17.6 percent year on year. The service providers and neocloud group (which now includes Apple and Oracle), represented $1.8 billion in sales in 2025, up 51.3 percent.

Arista ended the year with $10.74 billion in the bank, an increase of 29.4 percent from a year ago, and has a revenue backlog of $6.8 billion. It doesn’t have to build expensive datacenters or buy GPUs, so it can actually hang onto its cash hoard and make strategic acquisitions as it sees fit, and spend some of that money to prebuy components like flash and main memory as supplies keep tightening.

Here is how the revenues for 2025 for Arista stack up to the prior dozen years for which we have financial data:

Arista went public in 2014, so it is hard to get data that covers 2012 and earlier because it was not in the filing documents for the initial public offering.

What does matter is how the company is growing its revenue per customer and that it has expanded its sales to its key biggest customers, Microsoft and Meta Platforms. It also matters that this year, according to Arista, it may have one or two more customers that comprise more than 10 percent of its revenues, which triggers a reporting requirement due to concentration risk from the US Security and Exchange Commission. Arista was burned when Meta Platforms – then known as Facebook – skipped the 200 Gb/sec Ethernet generation back in 2020 and 2021, as you can see from the numbers in the table above.

Arista only gives the breakdown of sales by customer type and the details for its big customers at the end of every year, so we never know what is going on until it is done. In 2025, Microsoft represented 26 percent of Arista’s sales, or $2.34 billion, which was an increase of 67.2 percent compared to the software and cloud giant’s spending in the prior year. Meta Platforms represented 16 percent of sales for the 2025 year, which works out to $1.44 billion, up 40.9 percent year on year. This is a relatively normal concentration of these two companies over the years since Meta Platforms joined the 10 percent club in 2019. Microsoft has been a 10 percenter for as long as there have been public numbers.

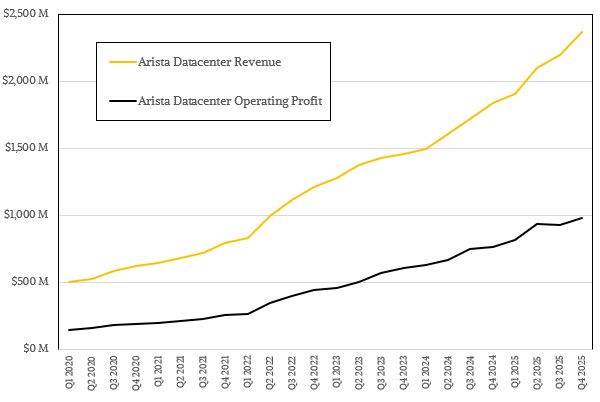

We like to try to figure out the portion of Arista’s revenues and operating income that are derived from datacenter products, and here is how we think that has changed over time:

Including both products and services, we reckon the datacenter drove $2.36 billion in sales in Q4 2025, up 28.9 percent, and operating income was $981 million, up 29.2 percent and representing 41.5 percent of that revenue.

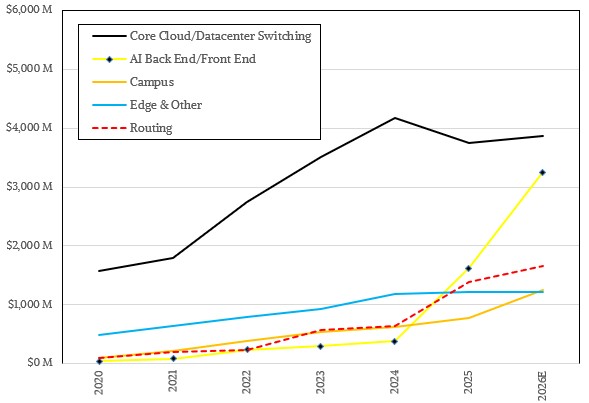

We also like to break Arista’s sales down by product groups and here is what we think has happened over the past several years based on statements that the company has put out:

Arista had set a goal for itself of selling at least $1.5 billion in AI networking and at least $800 million in campus switching in 2025, and Ullal said that both of those goals were exceeded. Considering that Ullal also said that Arista would double its AI-related sales to $3.25 billion in 2026, we can back that out and know that it had around $1.63 billion in AI-related sales in 2025. We think Arista did around $815 million in campus switch sales this past year and the company said point blank that it will do somewhere around $1.25 billion in campus gear in 2026.

If you want to see our model’s numbers, shown in the chart above, here they are:

What this means is that the non-AI part of the Arista business will grow by 12.3 percent to $8 billion in 2026 if the company hits its $11.25 billion guidance, and if you back out the campus switching business, then the remainder – cloud switching, routing, edge and branch – will only grow by 7 percent to $6.75 billion. We wonder how much of this is about switching components away from enterprises and towards the AI systems, with memory and flash getting harder and harder to come by. Arista has to keep those accounts to get its volumes, and given that the price increases for components are out of its costs, presumably it can make the hyperscalers and cloud builders make up the difference. Probably not more than that, though.

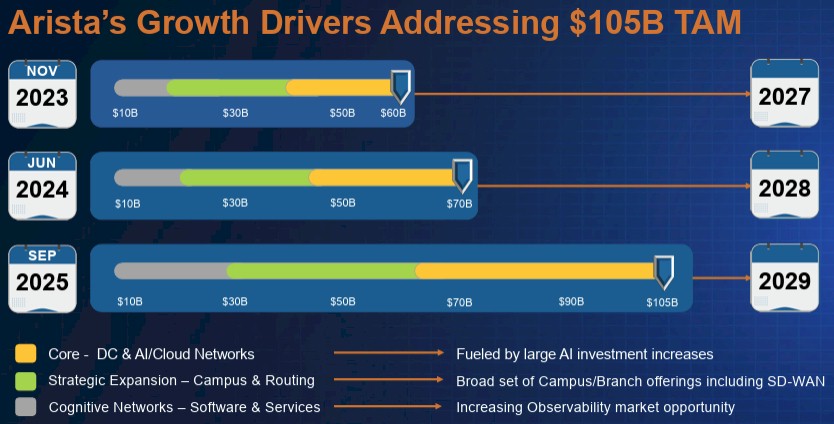

If you take a longer view, as Ullal & Co do, the total addressable market for Arista just keeps getting bigger as its reaches out into campus, branch, and edge and adds on AI networking as a new category. The company is now chasing a TAM of $105 billion by 2029, which is a hell of a lot bigger than the $60 billion TAM was looking at a little more than two years ago.

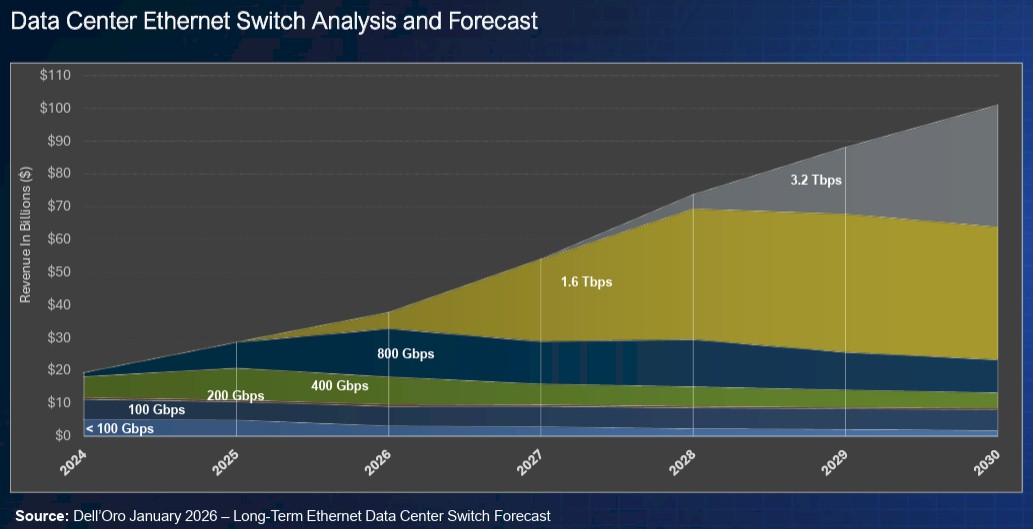

The AI networking opportunity is enormous, as seen in the forecast for revenues by port speed for Ethernet switching from Dell’Oro Group:

The 1.6 TB/sec Ethernet wave is a tsunami that was a little wave, which will grow considerably this year and be a wall of water as tall as skyscrapers in 2027 and 2028. And The 3.2 Tb/sec wave will start in 2027 and be its own wall on top of 1.6 Tb/sec Ethernet switching gear from 2028 and beyond.

The amazing thing in this forecast is how 100 Gb/sec, 400 Gb/sec, and 800 Gb/sec devices will persist in the revenue stream out to the end of the decade, even as most of the money – being spent by hyperscalers, cloud builders, and model builders – goes towards switches with much faster ports.

Sign up to our Newsletter

Featuring highlights, analysis, and stories from the week directly from us to your inbox with nothing in between.

Subscribe now

Related Articles