Summary of key points: –

Pick your scenario of how this Middle East war plays out

The Fed’s job just became harder with energy inflation and weak jobs

New Zealand’s economic fundamentals continue to improve

Pick your scenario of how this Middle East war plays out

Unlike economic trends, drivers and data that determine likely exchange rate direction, geo-political risk events such as a war in the Middle East, are impossible to predict in terms of their impact on future currency values. In a financial risk management sense, the only sensible analysis of the war risk to gauge the likely impact on exchange rates, is to paint alternative outcome scenarios and then assign probabilities to each selected scenario. The probability percentages may then be adjusted as more facts are ascertained through the progression of time.

Below is our considered analysis of the potential scenarios of the US/Israel attack on Iran and their resultant impact on foreign exchange market pricing: –

Scenario 1: Rapid Iranian capitulation, surrender and regime change

The missile strikes on Iran that have been pounding their military installations/cities for a week now, ends abruptly in one to two weeks’ time.

The Iranian military surrender and their Government leadership collapses.

Early indications are that oil production and shipments through the Strait of Hormuz can resume within weeks.

Crude oil prices (WTI) peak somewhere between US$90/barrel and US$100/barrel then plummet to below US$70/barrel within a week as the oil supply risk disappears.

Less impact on global growth and inflation than first feared as oil prices drop back as fast as they moved up.

Currency markets quickly unwind long-US Dollar positions as the war risk is suddenly removed. The USD Dixy Index returns to 97.00 (and potentially lower) from the current 98.85 level. The NZD/USD exchange rate is again testing the resistance at 0.6150.

Probability of occurrence = 50%.

Scenario 2: Slower progression to cessation of missile strikes on Iran

It takes the US and Israel much longer to force a surrender from the Iranians (one to two months from now).

Oil supply disruption continues for many weeks, holding the WTI oil prices around US$100/barrel for an extended period.

Under political pressure at home as the opinion polls move against him, President Trump is eventually forced to stop the bombing and seek a diplomatic solution with the Iranians.

Headline inflation is pushed up in the US, Australia and New Zealand by petrol pump price increases. However, the respective central banks “look through” the oil price increases and concentrate on “core” inflation that excludes energy prices. Monetary policy is not loosened any later in the US (interest rate cuts), or tightened harder in Australia (interest rate increases), or tightened earlier in New Zealand (interest rate increases).

The US Dollar remains at around 99.00 for the next six weeks and then slowly depreciates back towards 97.00 as the war risk recedes. The NZD/USD rate remains stable at 0.5900 before climbing back above 0.6000 as the USD eventually weakens on the speculative positioning unwinding.

Probability of occurrence = 40%.

Scenario 3: Vietnam and Afghanistan revisited!

The American intervention, as the self-nominated world’s policeman, is a complete failure and the Israel/US war against Iran turns into a prolonged quagmire.

Russia and China, who have stayed well away from the conflict to date, belatedly decide to come in and support Iran. Global geo-political risk remains elevated for most of the year.

Sporadic missile and drone attacks both ways continue for many months.

Public opposition within the US to the war increases to the point where the Republicans are trounced in the House of Representatives and Senate at the November mid-term elections.

Trump attempts to continue the military strikes on Iran, however, is eventually forced to stop as his political position in the US becomes untenable.

Oil prices remain high for much longer, the Fed is forced to abandon interest rate cuts in 2026, and the USD appreciates to over 100.00. The NZD/USD exchange rate is pushed back to 0.5700 by the stronger USD.

Probability of occurrence = 10%.

The surprising aspect of the whole US/Israel attack on Iran to end Iranian-sponsored terrorism is that no-one knows where/what the “off-ramp” is and how long it will take to get there. Trump is making it up as he goes in terms of end objectives and what success look like, as he does with everything else, he touches.

So far, the US economy is being damaged by his tariffs and interventionist foreign policy. It is difficult to see foreign investors into the US being encouraged to put more money into all the uncertainty/chaos that Trump has a knack of creating.

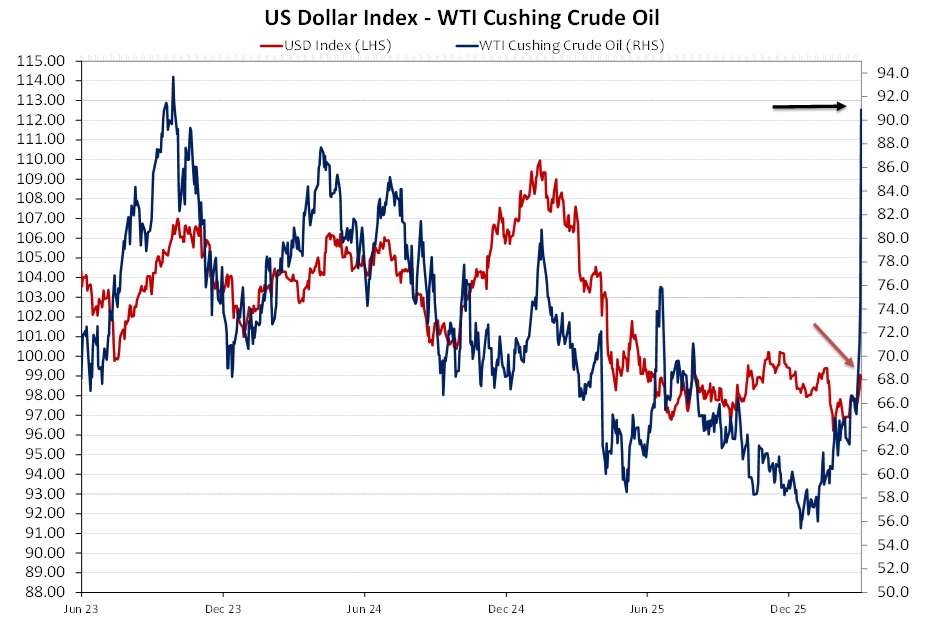

Over recent years the USD Index has tracked oil prices as the US became a net exporter of oil. It is instructive that the USD has not followed the latest spiral in WTI oil prices from US$65.00/barrel to above US$90.00/barrel.

The Fed’s job just became harder with energy inflation and weak jobs

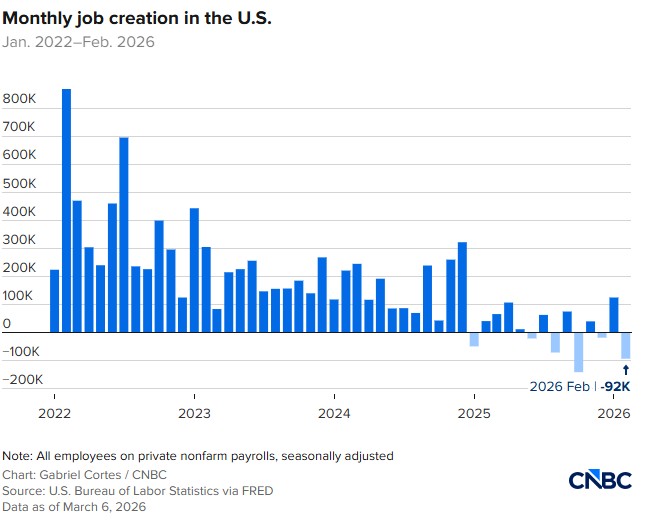

One of the Fed’s voting members this year is Cleveland’s Beth Hammack. Ms Hammack is rated at the extreme end of the spectrum of “hawks” when it comes to setting monetary policy and interest rates. In a speech last week, she stated that interest rates should be kept at current levels for “quite some time” to see whether inflation reduces further and whilst the labour market “stabilises”. The latest data on the US labour market, the monthly Non-Farm Payrolls statistics on jobs for the month of February indicated that employment conditions were a very long way from being described as “stable”. The US economy lost 92,000 jobs in February, a very weak outcome that was much worse than the 50,000 increase that was expected. As the chart below shows, the US economy has lost jobs in three of the last five months. The previously announced 130,000 increase in jobs in January was revised down to +126,000, as we expected it would be. Further downward revisions seem likely for the January numbers. The original 50,000 increase in jobs in December 2025 has now been revised down to a loss of 17,00o jobs. Contributing to the 92,000 decrease in jobs in February was a strike in a healthcare company in California and Hawaii where 30,000 workers were sidelined. Despite that impact, it was still an unexpected weak and deteriorating outcome. You just cannot trust the accuracy of the numbers; however, you have to wonder what numbers Beth Hammack is looking at to state that the labour market is stabilising.

If we did not have war in the Middle East at this time that has sent oil prices skyrocketing, the Fed would be almost compelled to cut interest rates this month on the rapid deterioration in employment. With the worst of the tariff impact on inflation behind us and inflation trending back to 2.00%, the employment side of their dual mandate would require them to cut rates. However, the current situation is much more complicated with the soaring oil prices. The Fed’s target for inflation is “core” inflation, which excludes volatile food and energy prices so as to assess the underlying long-term trend of inflation. The Fed will only be holding off on cutting interest rates if they believe there is a risk of second round increases in prices from the gasoline price going up. The Fed’s commentary on both the current inflation and employment trends will be the centre of focus at the next meeting in 10 days’ time on 18 March.

The interest rate and currency markets seem unsure how to price the conflicting forces of a substantially weaker US labour market and soaring oil prices. Depending on developments in Iran, the oil price spike may be much more short-lived than what most expect. US two-year and 10-year Treasury Bond yields at 3.55% and 4.13% respectively, are trading at similar levels to a month ago. The USD Dixy Index jumped up from 98.50 to 99.50 when the war started a week ago, however it has remained within that range since. US equity markets have dropped as investors are not only worried about escalated geo-political risks, but also the risk of a weaker US economy. Herein lies the political problem for Donald Trump who always points to rising share markets as an endorsement on the success of his economic policies. Which, of course, is not true at all as the share market gains are largely due to the AI revolution and related chip makers.

Trump appears to be already under enormous and growing political pressure at home to end the Iran war quickly. For this reason alone, it is a reasonable risk/reward equation to conclude that the Fed will not be delaying interest rate cuts this year due to spike in oil prices as it will prove to be short-lived in nature. The failure of the US dollar to push to higher levels than 99.50 through this last week also suggests that USD buyers do not want to be caught on the wrong side of the market should the war end abruptly. Even though the US dollar has not really followed oil prices higher, a rapid plunge in the oil price would be negative for the USD as market positions are reversed.

The Saudi’s are reported to be reaching out to the Iranian regime to bring a quick end to the conflict. The involvement of the Saudi’s is highly unusual, as they are Sunni Muslim and the Iranians are Shiite Muslim – the two Muslim sects are typically very distrustful of each other. It seems the Americans are using the Saudis as a backchannel to negotiate an early end. The off-ramp may be closer than what most commentators think!

New Zealand’s economic fundamentals continue to improve

In our FX report three weeks ago on 15 February, we provided a table on New Zealand economic data releases from 26 November, which confirmed that 17 out of 20 measures of the economy had been stronger than prior consensus forecasts. Since 15 February the “stronger than expected” trend has continued with higher dairy commodity prices, higher retail sales and a significantly higher Terms of Trade Index (export prices over import prices) for the December quarter. The Terms of Trade Index increasing by 3.70%, well above the prior forecasts of a small decline. Export prices outside of dairy are still climbing, providing a serious boost to the New Zealand economy. Business and consumer confidence surveys have levelled off at their higher points achieved in previous months.

We will receive a confirmation as to the speed and strength of the export-led economic recovery on 19 March with the release of the GDP growth rate for the December 2025 quarter. Forecasts are for a 0.50% increase following the 1.10% expansion in the September quarter. Subdued construction industry activity will be pulling the GDP growth numbers back a touch, however it would be no surprise to see a higher quarterly growth number than the +0.50% expected. Over coming weeks, we expect to see further data on the NZ economy that confirms growth is stronger and inflation higher than RBNZ forecasts for both.

It will take some time for the RBNZ to realise that they are behind the 8-ball with their stated view that the economy is only in the formative stages of an economic recovery. The FX markets will, however, start to price-in well in advance a pivot by the RBNZ in May of June. We are likely to see some interest to buy the Kiwi dollar before the actual interest rate differentials to the US close up. We may also see some NZD buying from foreign nationals coming to NZ under the golden visa scheme. That foreign interest in NZ can only increase with the current Middle East war.

Select chart tabs

US$

AU$

TWI-5

¥en

¥uan

€uro

GBP

Bitcoin

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.