Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

Michael Burry has taken a significant new position in Adobe (NasdaqGS:ADBE), going against negative sentiment around AI competition.

Hedge funds and other institutional investors have also been active buyers, alongside ongoing insider and institutional trading.

Adobe is pushing AI deeper into its product stack, including its proprietary Firefly model, as part of a broader business transformation.

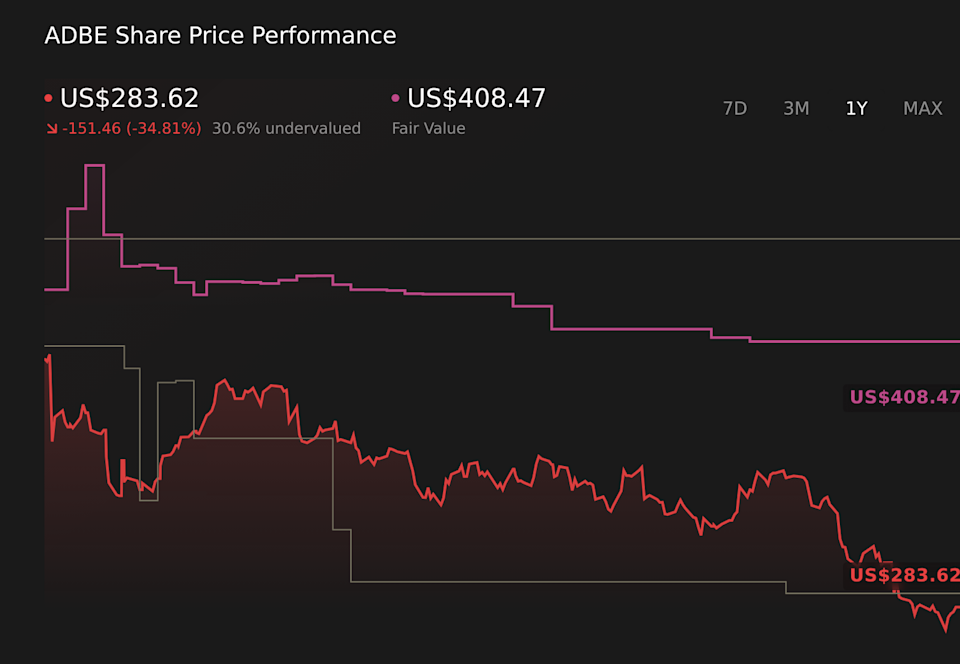

Adobe, which last closed at $283.62, has seen a 36.9% decline over the past year and a 36.2% decline over five years, while the stock is up 8.1% over the past week and 5.7% over the past month. Year to date, the share price is down 14.9%, and the company currently carries a value score of 5, which some investors read as pointing to a potential deep value setup. In that context, Burry’s entry and wider hedge fund interest are drawing attention to Adobe’s fundamentals and the balance between its growth ambitions and valuation.

The key question for you is how Adobe’s AI push, particularly Firefly across its creative and enterprise tools, fits with your view of the long term prospects for paid software versus free AI alternatives. Institutional activity and contrarian buying indicate that some professional investors see opportunity at current prices, but the impact of AI integration and competitive threats remains uncertain and may take time to appear in reported results.

Stay updated on the most important news stories for Adobe by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Adobe.

NasdaqGS:ADBE 1-Year Stock Price Chart

NasdaqGS:ADBE 1-Year Stock Price Chart

See which insiders are buying and buying and selling Adobe following this latest news.

Michael Burry stepping in alongside heavier institutional and options activity tells you that some professional investors see the recent share price reset and AI concerns as an entry point rather than a reason to avoid Adobe. Options flow skewed toward bullish calls and strong ownership by large asset managers suggest there is real capital willing to back the view that Adobe’s transition to AI-powered tools, including Firefly, could support its paid ecosystem even as free models from players like Google and others gain traction. At the same time, multiple banks have cut price targets and highlighted pressure from AI-powered rivals such as Canva, as well as broader software sector weakness, so the buying is happening against a cautious backdrop. For you, this is really about time horizon and conviction. If you think Adobe can keep its creative and document subscribers engaged with higher value AI features and careful pricing, then this sort of contrarian institutional interest may reinforce that thesis. If you think free or cheaper AI tools from competitors like Microsoft and smaller pure-play AI platforms will steadily erode Adobe’s edge, then recent hedge fund buying may not be enough to change your stance.

Burry’s purchase and increased institutional positioning line up with the narrative that AI-powered products like Firefly, Acrobat AI Assistant and Express can deepen user engagement and support revenue growth as Adobe integrates them across its creative and enterprise stack.

Target cuts from firms such as Jefferies, HSBC and Citi, plus concerns about heavy discounting on Creative Cloud Pro, challenge the idea that AI features will automatically support pricing power and margins as Adobe rolls out its One Adobe and cross-cloud strategy.

The spike in options activity and social media focus on near term earnings, Firefly adoption and promotions are very near term in nature and are not explicitly captured in the narrative’s longer term view of partner ecosystems and mobile-first offerings.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Adobe to help decide what it’s worth to you.

⚠️ Rising competition from free and low cost AI-powered creative tools, including from large players like Google and Microsoft as well as Canva, could pressure Adobe’s Creative Cloud growth and pricing over time.

⚠️ Aggressive discounting on products such as Creative Cloud Pro and questions from analysts about revenue quality point to potential margin pressure if Adobe needs promotions to support user growth.

🎁 Strong institutional ownership, recent hedge fund interest and a surge in bullish options activity signal that many professional investors still see a solid business with the potential to benefit from AI features across creative and document workflows.

🎁 Management’s focus on integrating Firefly across flagship apps, plus record cash generation and continued buybacks, suggests Adobe has meaningful resources to invest in AI features while supporting shareholder returns.

From here, keep an eye on three things. First, the upcoming earnings on March 12 and any updates on Firefly usage, AI-influenced annual recurring revenue and conversion from free tools like Adobe Express into paid plans. Second, how pricing and discounting evolve, since that will tell you whether AI features are strong enough for Adobe to sustain or raise effective prices without leaning too heavily on promotions. Third, watch institutional ownership trends, insider transactions and options activity to see whether Burry’s move is an isolated contrarian bet or part of a broader shift in sentiment toward Adobe versus peers such as Salesforce and Oracle in enterprise software.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Adobe, head to the community page for Adobe to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ADBE.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com