Most of the news around housing affordability revolves around first home buyers, but an often overlooked group are the so-called second rung buyers. These are people who bought their first home several years ago and are now ready to buy their next home, moving onto the second rung of the property ladder.

The latest data suggests they would’ve received a helping hand. That’s because prices at the more affordable end of the market favoured by first home buyers have increased more quickly than prices in the middle of the market, which is where the second rung cohort are likely to be buying their next home.

That would have helped these second rung buyers build up equity in their first home, giving them a bigger deposit to buy into the middle of the market several years down the track.

The currently low interest rates would then help with ongoing mortgage payments.

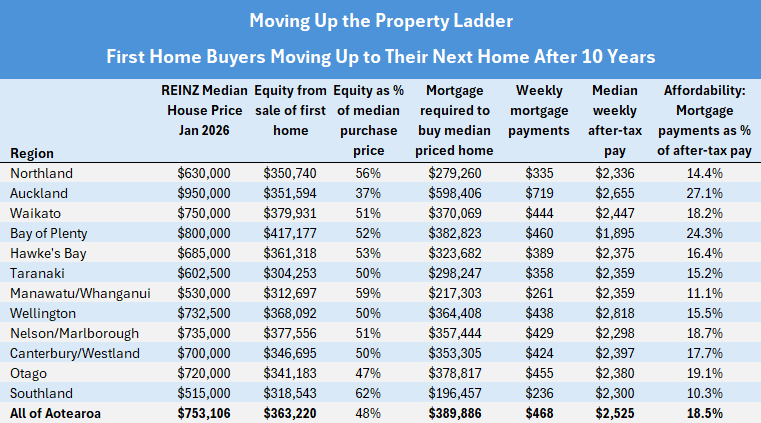

Let’s assume a couple bought their first home 10 years ago for $302,500, which was the Real Estate Institute of New Zealand’s national lower quartile selling price at the time.

Ten years later and they are ready to move up to something a bit better, so sell their home at the REINZ’ s January 2026 lower quartile price of $580,000, up 92% on their original purchase price.

Assuming they had originally purchased that house with a 20% deposit, interest.co.nz estimates they would be left with equity of $363,220 once they repaid what was owning on the mortgage and selling expenses such as agent’s commission.

That would give them a 48% deposit on a home purchased at the REINZ’s January 2026 median price of $753,106.

That’s a pretty good deposit, but of course they would need a mortgage of $389,886 to complete the purchase. Interest.co.nz estimates repayments on a mortgage of that size would be around $468 a week, at 4.74% with a 30 year term.

If the couple were both working full time and earning the median pay rates for 35-39 year olds, they’d be taking home around $2525 a week between them, after tax.

So at current interest rates, the mortgage payments of $468 would eat up just 18.5% of their after-tax pay, putting it well within affordable limits.

Even when allowing for regional differences, moving up to the second rung of the property ladder should be an affordable exercise for people who have owned their first home for a reasonable amount of time.

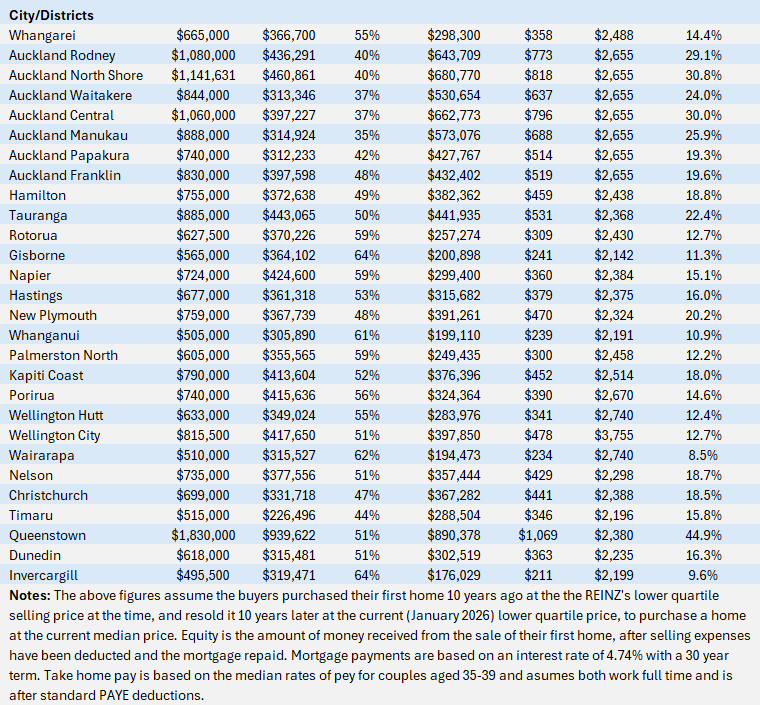

At the regional level, the amount the sale of a first home would provide towards a home purchased at the current median price ranges from 37% in Auckland to 62% in Southland, based on the formula above. See the chart below for the full regional and district figures.

And the amount of after-tax income the payments on the mortgage would eat up would range from 10.3% in Southland to 27.1% in Auckland.

This suggests moving up the property ladder should not only be achievable for most first home owners after they’ve owned their property for a reasonable amount of time, it should also leave them with some flexibility to manage their finances according to their changing circumstances.

The tables below show the main affordability measures for first home owners looking to move up to their next home after 10 years.