We look at how wholesale money markets are reacting to the current geopolitical crises, and what is in store for fixed home loan rates

Followers of wholesale swap rates will know they have been on the rise recently.

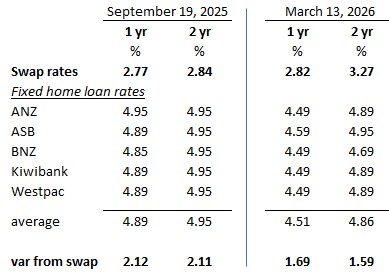

In fact, the one year swap rate is back to mid September 2025 levels. And two year swap rates are now more than +40 basis points (bps) higher than those September 2025 levels.

So it is timely to ask now how that might affect fixed mortgage rates.

Swap rates are a good indication of the banks cost of money. But they aren’t the only factor that goes into retail rate settings. However, they are an important factor and set a base from where banks assess their pricing.

But first, why does mid-September 2025 have relevance in this assessment? Well, it was the last time there were Middle East tensions large enough to disrupt international trade, and affect the global cost of money. The entrance to the Red Sea was under threat from forces in Yemen with a proxy war playing out between Iran and Saudi Arabia. And of course the Gaza tragedy was just getting started with its own explosions.

Financial markets shifted to risk-off modes and benchmark interest rates fell on the assumption that sovereign debt was safe and that equity returns were under threat.

Now of course we have another and arguably larger geopolitical crisis. But this time sovereign debt, especially US Treasuries, are no longer looking as safe under the Trump Administration mismanagement. These benchmark rates are now rising, and risk premiums are flowing outward. In fact, there are also liquidity issues now. Fewer international investors are prepared to come to the New Zealand swap market transactions. A shortfall like that inevitably drives up interest rates.

After the moves this week, bank margins have been compressed. Whatever you may think about their levels, they are now -40 bps to -50 bps lower than our reference period. Bank treasurers will be feeling the compression.

If these pressures play out as they usually do, we could see +50 bps rises in one and two year carded fixed home loan rates, and fairly soon. And they will come even though financial markets are not pricing in any Official Cash Rate (OCR) rate hikes until at least July, and probably September 2026. Certainly none at the April 9 or May 27 OCR reviews.

Select chart tabs

1 year %

2 years %

3 years %

4 years %

5 years %

7 years %

10 years %

Then there is the question: Will savers get the same boost if home loan rates do in fact rise?