Roth conversions are often promoted as a universal solution for federal retirees: pay taxes now, reduce future required minimum distributions (RMDs), and create tax-free income later. For married couples filing jointly, that advice can be sensible.

For federal widows receiving both a FERS survivor pension and Social Security, however, the math changes—often dramatically.

A FERS pension creates a permanent income floor. It cannot be paused, delayed, or reshaped to manage taxes. Social Security, once claimed, adds another layer of largely unavoidable income. Together, these benefits compress tax flexibility while increasing exposure to Medicare’s Income-Related Monthly Adjustment Amount (IRMAA). In this environment, Roth conversions must be evaluated with far greater precision.

The Widow Tax Reality: Guaranteed Income Comes First

After the loss of a spouse, most surviving spouses move from married filing jointly to single filing status. Tax brackets are effectively cut in half, yet income often remains high.

A FERS survivor pension continues as fully taxable ordinary income. Social Security benefits, once claimed, are frequently taxed at the maximum 85% level. Investment income fills in the gaps.

Before a widow takes a single dollar from the TSP or an IRA, her taxable income may already sit near a Medicare premium threshold. Roth conversions therefore do not start from zero—they are layered on top of income sources that cannot be engineered away.

This is why strategies that worked well while married can quietly backfire after widowhood.

Consider a 67-year-old federal widow enrolled in Medicare and receiving Social Security.

She has a $42,000 FERS survivor pension, $24,000 in Social Security benefits, and $6,000 of investment income. With 85% of Social Security taxable, her base MAGI is approximately $68,000 before any Roth conversion.

Under Strategy A, she converts $80,000 in a single year. Her MAGI rises to nearly $150,000, triggering not only a higher marginal tax rate but also IRMAA Part B and Part D surcharges. The estimated combined tax and Medicare premium cost is roughly $30,000 in this scenario.

Paying Now vs. Saving Later

Roth conversions promise long-term tax savings by reducing future RMDs. That benefit is real. But for widows with pension and Social Security income already in place, the upfront costs matter more than most planning models admit.

The lesson is not that Roth conversions fail universally. Rather, when guaranteed income already anchors taxable income for life, large, front-loaded conversions demand extraordinary patience to pay off.

Why Conversion Size Matters More Than Conversion Timing

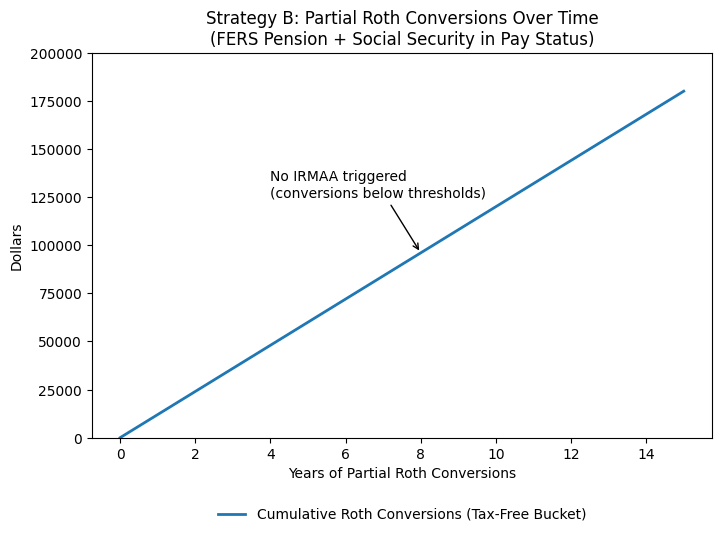

Strategy B explains why a different approach often produces better results.

Under Strategy B, she converts only $12,000 annually. Thus, her MAGI remains within the first IRMAA premium threshold. Her Medicare premiums are unchanged, Social Security taxation does not worsen, and RMD exposure declines gradually over time.

In this example, the widow’s base modified adjusted gross income includes a FERS survivor pension, Social Security benefits, and modest investment income. As long as annual Roth conversions remain modest, total income stays below the first IRMAA threshold. Medicare premiums remain unchanged, even as future RMD exposure is gradually reduced.

This graphic highlights a critical but often misunderstood point: IRMAA is not triggered by Roth conversions themselves—it is triggered by crossing a specific income line. Once that line is crossed, Medicare premiums can jump even if the threshold is exceeded by a small amount.

For widows, this “cliff” effect makes conversion sizing far more important than conversion speed.

When Restraint Quietly Wins

Rather than pursuing a single large conversion, Strategy B uses modest annual conversions deliberately sized to remain below IRMAA thresholds. Over time, meaningful assets are shifted into Roth accounts, creating tax-free flexibility later in retirement. RMD pressure declines gradually, without triggering Medicare premium increases along the way.

Notably, Strategy B does not rely on a dramatic break-even moment. Its advantage comes from avoiding penalties altogether, not from trying to outrun them. For widows with pension and Social Security income already in place, that absence of IRMAA costs is often the most powerful feature of all.

Roth conversions remain a valuable planning tool—but for federal widows receiving a FERS survivor pension and Social Security, they must be used like scalpels, not sledgehammers.

Guaranteed income provides stability, but it also guarantees ongoing tax exposure. In that environment, smaller, deliberate conversions often outperform large, front-loaded strategies. Existing Roth balances become especially valuable, not simply because they reduce RMDs, but because they provide tax-free income without disrupting Medicare premiums.

For many widows, the winning strategy is not eliminating future taxes at all costs. It is balancing lifetime taxes, Medicare affordability, and income stability. With a pension and Social Security already in place, the right answer is rarely “convert everything.” More often, it is “convert just enough—and no more.”

Always consider exploring advice with qualified tax and federal benefits professionals.

© 2026 Francis Xavier (FX) Bergmeister. All rights reserved. This article

may not be reproduced without express written consent from Francis Xavier (FX) Bergmeister.