![[GETTY IMAGES BANK]](https://www.newsbeep.com/nz/wp-content/uploads/2026/03/0022cfec-5c43-4fcb-930e-b2470aff0e33.jpg)

[GETTY IMAGES BANK]

[BEHIND THE NUMBERS]

Korea’s Kospi, one of the most volatile markets among major economies this year, has turned into a tug-of-war between foreign and institutional investors versus retail traders, with foreigners trimming positions on profit-taking and bubble concerns while individuals absorb the equities.

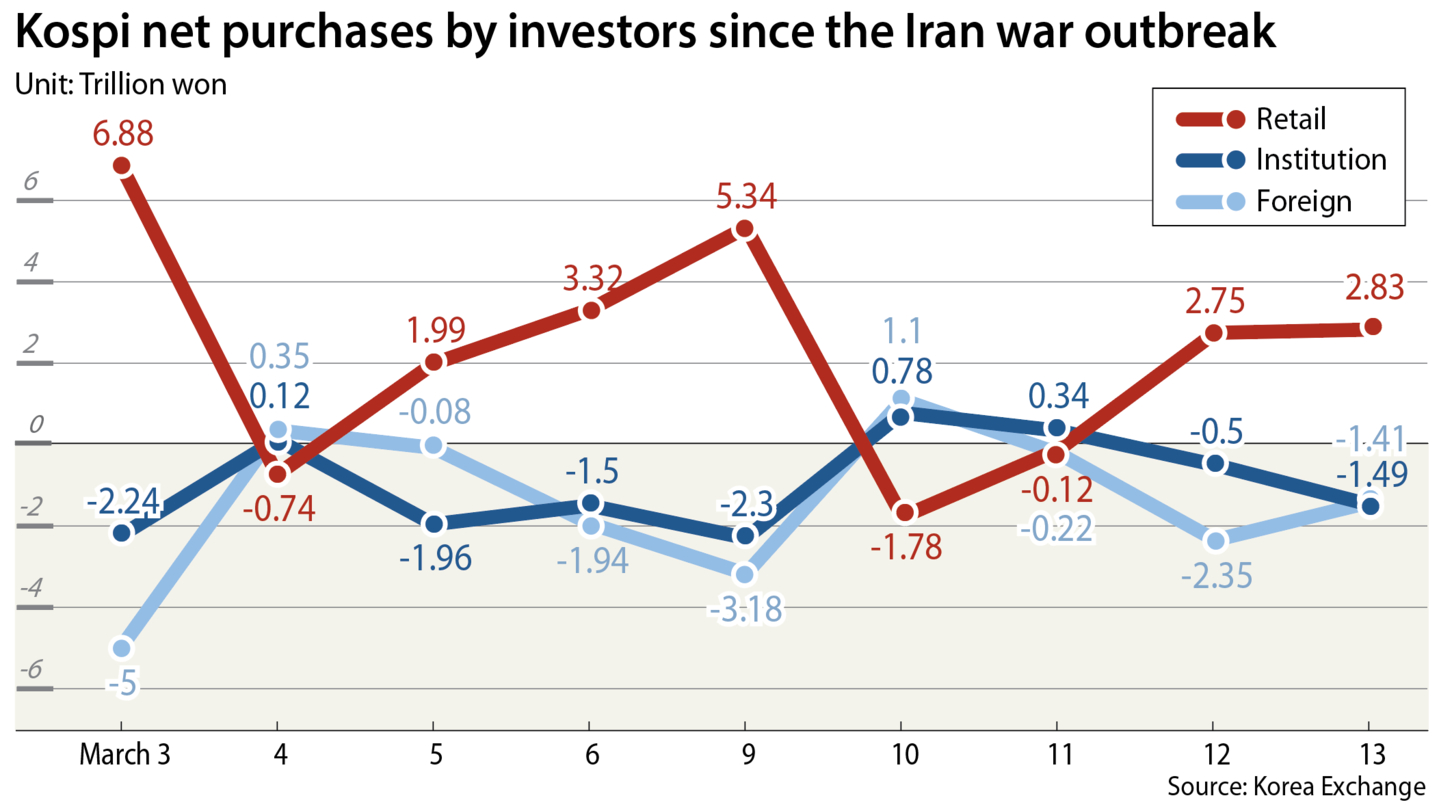

The showdown hit its peak on March 3, the first trading day after the breakout of the Iran war, during which retail buyers scooped up a net 6.88 trillion won ($4.6 billion) worth of stocks on the Korea Exchange, while foreign and institutional investors collectively sold off over 7 trillion won.

This year alone through March 13, retail investors, roughly more than 14 million, net purchased 49 trillion won, while

institutional and foreign investors sold net 23 trillion won and 33 trillion won, respectively, so far this year, fueling what some are calling a second round of the Donghak Ant Movement — a term coined during the 2020 pandemic to describe the wave of mass buying by individual investors. The name draws a metaphor from the Donghak Peasant Movement in late 19th-century, portraying small individual investors — called “ants” in Korean market slang — as ordinary people rising up against powerful elite and foreign influence.

The total amount of equities individual investors purchased in less than three months into the year is comparable to the 54 trillion won that retail investors net purchased in an entire year in 2020 during the first round of the Donghak Ant Movement.

Some argue that a market driven by individual investors is often hard to sustain. Stocks typically soar during rallies and plunge just as quickly during downturns, reflecting how fickle these investors can be compared to foreign or institutional investors, who trade according to portfolio allocations.

But economists say the current market is unfolding differently, as retail investors are encouraged to hold onto stocks long-term.

“We are seeing a major shift in Korean household portfolios,” said Kim Doo-un, senior analyst at Hana Securities, citing the government’s efforts to lay the groundwork for long-term capital to flow into the stock market rather than into real estate, a traditional favorite of investors.

At the root of the long-held belief that real estate was unbeatable was the idea that holding property for longer brought tax benefits, such as lower capital gains tax, depending on the holding period. But now many believe — based on the government’s current policy stance — that property holding taxes could rise.

In contrast, while stocks previously offered little incentive to hold them long-term, new tax benefits are being introduced that increase the longer the stocks are held, including a separate, lower tax rate on dividend income rather than subjecting it to comprehensive income taxation.

“Such market-friendly policies are serving as a catalyst encouraging individual investors to adopt long-term investment strategies,” Kim added.

Specifically, policies that could boost stock prices as well as solid corporate earnings are driving retail funds into equities.

“The key forces that are currently drawing individual funds into the stock market are strong corporate earnings, particularly in semiconductors — along with rising prospects in shipbuilding, defense and humanoid robotics — and market-friendly policies aimed at channeling money from real estate into equities,” said Park Seok-hyun, an economist at Woori Bank.

The government has introduced market-friendly measures, including mandatory cancellations of treasury shares within a year and plans to launch exchange-traded funds [ETFs] that track twice the performance of a single stock, like Samsung Electronics and SK hynix. But it has simultaneously imposed strict real estate policies to curb home purchases, such as significantly tightening mortgage lending and announcing plans to increase transfer income tax on owners of multiple homes when they sell their units.

As the market environment changed, retail investors saw the recent plunge in equities as an opportunity to invest in Korean chipmakers.

“I bet all the money in my account on the Kospi after the index nose-dived following the recent geopolitical tensions,” said an office worker who wished to remain anonymous. “I sold my U.S. stocks to buy Korean shares — especially chipmakers — during the latest bout of market volatility, adding more whenever the index fell. I was nervous, but confident they would bounce back on market-friendly policies, such as the planned introduction of leveraged ETFs tracking individual stocks.”

Another investor bought the dip in Korean stocks.

“My heart sank after the index plunged following the outbreak of the war,” said an office worker surnamed Park. She had bought Korean Air before the war and recently bought Samsung SDI, believing that demand for secondary batteries would soar as electric vehicles became more widely commercialized. “I ended up buying more Korean stocks, viewing the drop as a temporary setback and an opportunity to buy before the market rebounds.”

Such unwavering confidence in the Korean stock market — fueled by a 76 percent surge in the Kospi last year and an additional 45 percent rise in the first two months of this year, with a bullish outlook toward 8,000 points — has even prompted individual investors to borrow funds to invest.

According to the Korea Financial Investment Association, outstanding credit balances hit a record 33.7 trillion won on March 5, up nearly 3 percent since the start of the month, while forced liquidations relative to unsettled margin trades totaled 77.7 billion won on the same day — the highest in two years and five months.

![Customers wait for brokerage services at a local branch in Seoul on Jan. 26. [YONHAP]](https://www.newsbeep.com/nz/wp-content/uploads/2026/03/a17de4ca-aed0-4610-ac35-2ebfeb4b6895.jpg)

Customers wait for brokerage services at a local branch in Seoul on Jan. 26. [YONHAP]

Despite these market-friendly moves toward the stock market, foreign investors continue to have limited interest in Korean equities.

“A large portion of foreign capital is passive money that tracks market-cap weights. Given the Kospi’s sharp surge this year, that structure could lead them to trim holdings rather than add more in a rising market. This suggests it will be individual, not foreign, investors driving the Kospi’s recovery or any push beyond the 7,000-point mark,” Park from Woori Bank added.

Beyond portfolio constraints, the won’s recent swings against the dollar are also deterring foreign investors from entering the Korean market, according to Won Jai-hwan, a finance professor at Sogang Business School. “To attract foreign investors, exchange rate volatility must be stabilized, as fluctuations can undermine the returns they earn from stocks,” Won said.

The won traded at 1,499.2 against the dollar on Monday, sliding to its weakest level in 17 years since March 12, 2009, when the currency stood at 1,496.5 per greenback during the global financial crisis.

BY JIN MIN-JI [[email protected]]