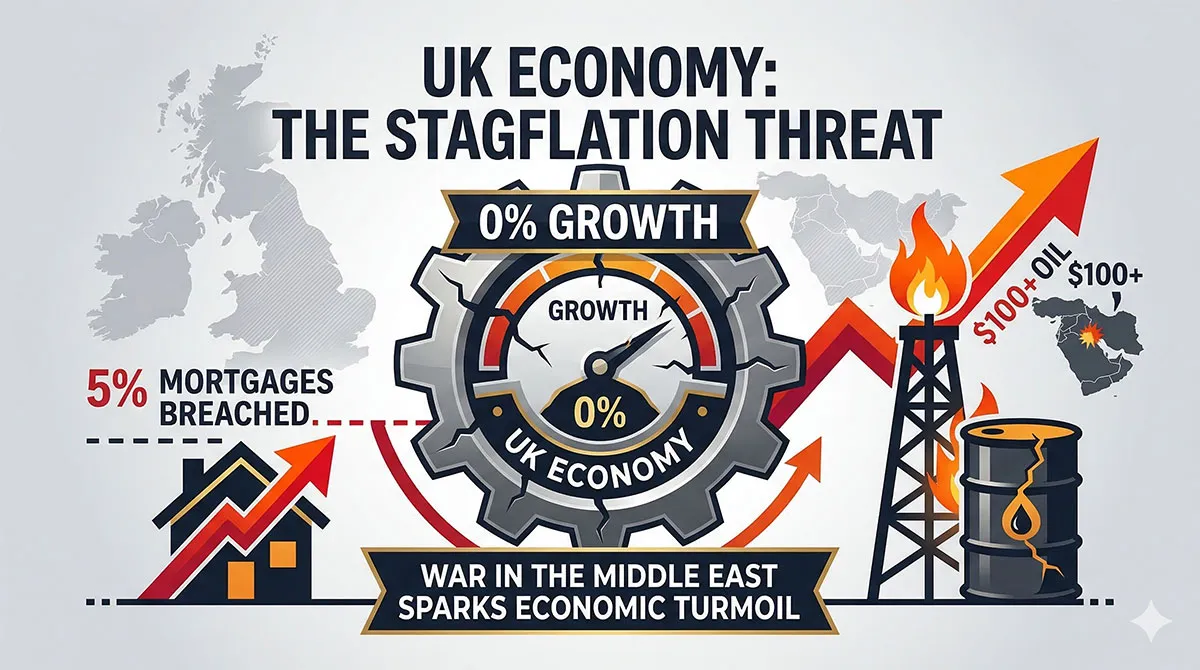

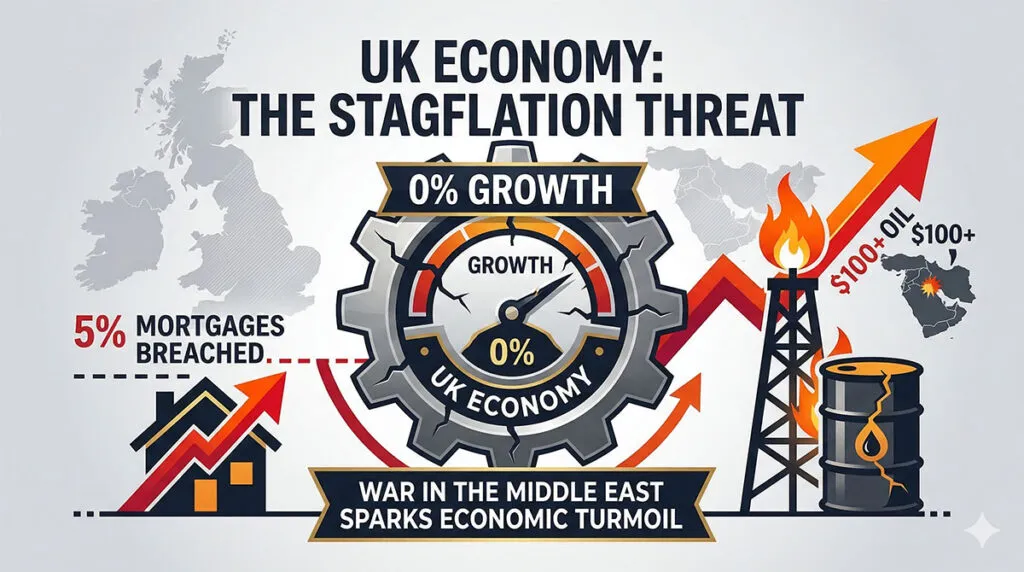

The UK economy failed to grow in January, in a fresh blow to the government’s pro-growth agenda.

ONS data showed no economic growth, the latest disappointing news for the UK economy, which saw growth of just 0.1 per cent in Q3 and Q4 of 2025.

The data reveals that the UK is now in a recession on a per capita basis, and, following the outbreak of the Iran war, could be headed for a full-blown recession later this year.

Economists fear that the economy, already on wobbly footing, could be knocked off its feet by fallout from the war, which has already resulted in higher prices at the pumps.

But the oil price spiral won’t only be felt at filling stations – if oil remains above $100 a barrel, the inflationary pass-through could be significant.

Markets are now increasingly pricing in the chance of the Bank of England hiking rates, rather than cutting them this year, as the spectre of inflation looms large.

Put together, higher prices, costlier borrowing, and miserable growth could see the UK economy shrink this year.

What is a Recession?

What is a Recession?

A recession is defined by two quarters of successive negative GDP growth. GDP, or gross domestic product, is the value of all goods and services produced by the economy, and is the primary metric by which we measure its size.

In January, the UK economy grew by 0 per cent, or in other words, failed to grow at all. In the three months from October to December 2025, Q4, the economy grew by just 0.1 per cent, as it did in Q3.

That means while the economy grew in absolute terms, it shrunk per capita, or per person, on account of the growing population.

So while the UK is not in the midst of a technical recession, Britons are becoming poorer on average, as the economy fails to grow commensurate with the population.

GDP per capita has been described as the “best measure of overall living standards”, and its decline means “we are now formally in a GDP per capita recession”, according to the Growth Commission.

What’s Next For the UK Economy in 2026?

In H2 2025, the UK economy posted meagre growth, and it ground to a halt altogether in the first month of this year.

The poor economic performance came before the outbreak of the US-Israel Iran war, which many fear could rebound on the global economy by sparking a new wave of inflation.

Markets had previously expected that March would bring a rate cut, expectations which have since been dashed, on account of the inflation threat.

The effects of this repricing have already been felt in the bond markets, with yields spiking and some mortgages rising past 5 per cent.

Some traders are even beginning to price in the possibility of an interest rate hike – still an outside chance – but one which becomes ever more likely the longer the conflict in the Middle East rumbles on.

Analysts at ING believe the Bank’s decision could hinge on oil prices; if they return to the $70s by April, a cut is on the cards, if prices remain stubborn, the chance is diminished:

“If by the time of the April meeting, energy prices have fallen back – say to 70-75 USD/bbl on oil and 35 EUR/MWh on gas – then we think there’s a chance the Bank could still cut rates at that point.

“Such a scenario would point to headline inflation staying below 3 per cent, which officials would be minded to ‘look through”

“In a scenario where the disruption lasts longer, risking inflation closer to 4 per cent, then the Bank will likely be more cautious.

“We suspect it would wait and see how firms react in surveys through the summer, on questions like wage growth expectations. That would point to a prolonged pause, but we think we could still see further easing later in the Autumn/into winter.”

In a scenario in which disruption is long-lasting, UK inflation could climb as high as 5 per cent by year-end, according to the chief UK economist at Oxford Economics, Andrew Goodwin.

Speaking to the Guardian, Goodwin said in a “worst-case” scenario, inflation could spike, the BoE may be forced to hike rates, and the UK could be plunged into a “mild recession.”

Also speaking to the outlet, Sanjay Raja, chief UK economist at Deutsche Bank, said the war could hit people’s wallets, growth, and the jobs market:

“With the Iran conflict bubbling in the background, further headwinds will drag UK growth lower.

“With energy prices rapidly rising, higher oil and gas prices will squeeze real disposable incomes, constraining spending and investment. Hiring plans will probably be shelved, too. And higher uncertainty will dampen animal spirits.”

Will There Be a Recession This Year?

Many economists have warned that the UK could be acutely vulnerable to the fallout of the Iran war. Before its outbreak, the economy was failing to grow, productivity was stagnant, and unemployment was on the rise.

What optimism there was rested in part on the assumption that the Bank of England would be cutting interest rates, an assumption which has now been thrown into doubt on account of the inflation threat.

Tomasz Wieladek, a macroeconomist at T. Rowe Price, warned that “stagflation is just around the corner” and described a recession as now “likely.”:

“The war in the Middle East and the consequent oil price rise will raise inflation and reduce consumer spending. The associated tightening in financial conditions we have seen in the bond market will exacerbate these effects. There will be significant demand destruction going forward.

“The UK has been one of the weakest advanced economies in terms of recent growth performance. Therefore, the current oil price shock will most likely not just lead to inflation, but also push the UK economy into recession, raising unemployment and reducing GDP. Stagflation is just around the corner.”

Will Mortgage Rates Go Up This Year?

There is already evidence some mortgages have gone up after expectations of a March interest rate cut were upended.

Last week, the average two-year fixed rate deal surpassed 5 per cent, according to Moneyfacts, the highest level since August 2025.

The Iran war has unwound assumptions about the Bank of England’s rate-cutting plans, with an oil price spike preparing to pass through onto the price of goods and services.

That potentially means higher inflation, and a central bank reluctant to ease monetary policy for the time being.

Commenting on the rise, Adam French, head of customer finance at Moneyfacts, said borrowers were now a hostage to events in the Middle East:

“It’s unwelcome news for borrowers, as the prospect of falling mortgage rates has quickly given way to rate rises. How far they could go is now heavily dependent on how global markets and inflation expectations evolve as conflict in the Middle East unfolds.”

The war was said to have thrown the UK mortgage market into turmoil, with UK banks reported to have pulled the most mortgage products from the market in three years.

Reuters reports that on March 9, lenders withdrew 308 residential products, the most since former Prime Minister Liz Truss’ infamous mini-budget.

There may be continued volatility ahead, with many commentators suggesting the White House’s war aims lack a clear focus and risk degenerating into a prolonged and destabilising conflict.

However, this instability may subside by the end of the conflict, according to Knight Frank’s global head of research, Liam Bailey.

Speaking to Mortgage Strategy, Bailey said that product removals would prove temporary, and that his analysis did not count a rate hike as likely:

“This is a defensive move by the banks, and it should correct as rate expectations stabilise.

“Nevertheless, that could take time, and rates are unlikely to return to previous lows while the volatility in energy prices continues.”

“Additional increases in oil prices could lead to a more prolonged pause. However, considering the policy rate is still in restrictive territory, the MPC is unlikely to hike unless inflation expectations rise significantly.”

In short, we have already seen some mortgage prices rise, with the Iran war triggering inflation fears, in turn reducing the chance of interest rate cuts, and pushing up borrowing costs.

Analysts say that the impact could be lasting in the event of a prolonged conflict in the Middle East, which sees oil stuck above $100 per barrel.

Why the Economy is Set to Get Worse Before it Gets Better

The latest data revealed Britain’s economy has come to a standstill. ONS figures report 0 per cent GDP growth in January 2026 and only 0.1 per cent in each of the final two quarters of 2025.

Real GDP per head actually fell 0.1 per cent in Q4, the second consecutive quarterly decline, meaning living standards are now falling.

The Labour market remains weak, with unemployment of around 5.2 per cent, the highest level in more than a decade. At the same time, wage growth is slowing, and inflation remains stubbornly above the Bank of England’s 2 per cent target rate.

The OECD and IMF had forecast UK CPI easing to about 2.5 to 3 per cent in 2026, but the oil price spike is already being felt on the petrol forecourts and on the shop shelves, and it may yet become more acute if the Iran war continues to drag on.

That potentially means higher inflation, fewer rate cuts, or even, according to some analysts, a potential interest rate hike this year.

The UK economy was already struggling before the outbreak of the war, but now faces being plunged into a recession as a result of it.

In a best-case scenario, hostilities quickly subside before oil returns to the $70s, helping to ease inflation and support growth.

In a recent client note, Oxford Economics said that if oil returns to ~$70–75 by spring, headline inflation could drop below 3 per cent and the Bank of England might resume rate cuts by late Q2 2026.

But a protracted war that keeps oil above $100 will exacerbate inflation and kick rate cuts into the long grass. Chief economist Andrew Goodwin of Oxford Economics calculates that if oil averages $100–140, UK CPI could spike above 5% by late 2026, forcing further BoE tightening and tipping the economy into recession.

Similarly, T. Rowe Price’s Tomasz Wieladek warns a lasting oil shock “will most likely…push the UK economy into recession, raising unemployment”, and that “stagflation is just around the corner”.

Before the war, markets had fully priced a March 2026 rate cut, but those bets evaporated once oil spiked. Some borrowers are already feeling the pain, with some UK two-year fixed mortgages climbing above 5 per cent.

A reversal of inflation expectations has also been felt in the gilt markets. Asone trader put it, “the market had become complacent about inflation, and that has now been abruptly reversed”. More money spent on debt interest means less available for productive areas of government spending, further depressing growth potential.

The UK economy was already on wobbly legs, but the Iran war threatens to knock it off them. If the conflict drags on with oil above $100, inflation looks to stay high, the BoE may hold or even tighten policy, and the risk of recession and higher unemployment will grow substantially.