Fresh analysis from Fidelity International reveals how grandparents can strategically merge inheritance tax (IHT) gifting rules with Junior ISAs to support younger family members whilst simultaneously managing their estate’s potential tax liability.

The research demonstrates that channelling the £3,000 annual IHT exemption into a JISA each year enables families to accumulate a significant sum for grandchildren over time, all while transferring wealth in a tax-efficient manner.

This approach allows grandparents to gradually reduce the overall value of their estate for inheritance tax purposes, as gifts made using the annual exemption are not added back to the estate’s value.

The strategy proves particularly relevant as the tax year end approaches, prompting families to consider how best to utilise their available allowances. The current JISA allowance permits contributions of up to £9,000 annually.

Grandparents are being urged to consider an inheritance tax hack

|

GETTY

Once a parent or guardian establishes the account, grandparents, other relatives, and family friends are all able to pay in.

Money held within these accounts grows entirely free from UK income tax and capital gains tax (CGT), with the child gaining access to the funds upon reaching 18.

The £3,000 annual IHT exemption operates separately, allowing individuals to gift this amount each tax year without it counting towards their estate’s value.

Should the previous year’s allowance remain unused, it can be carried forward once, enabling a gift of up to £6,000.

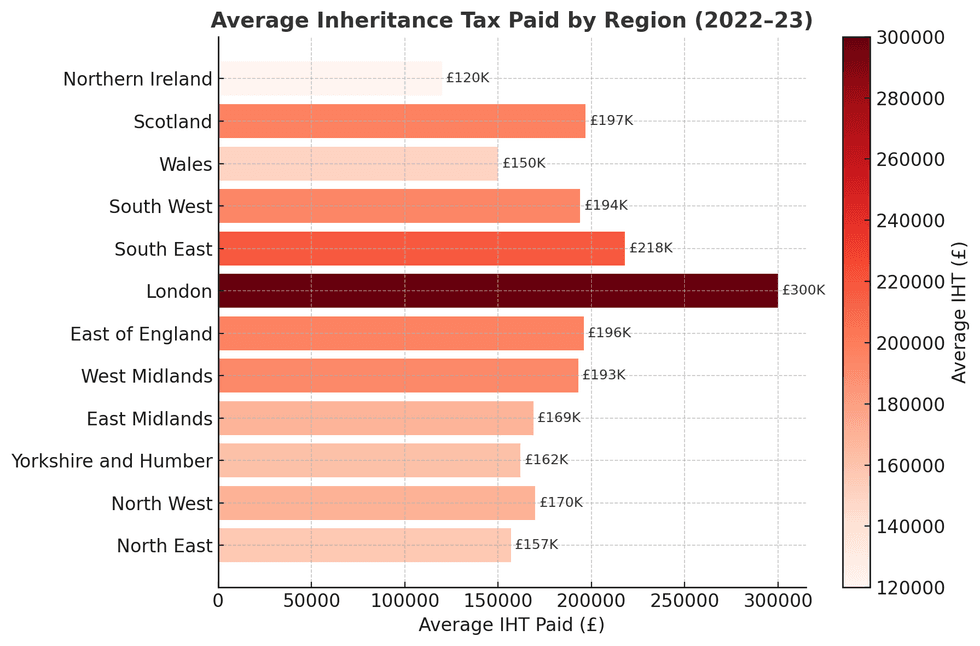

Average Inheritance tax paid by region | CHATGPT/ONS

Average Inheritance tax paid by region | CHATGPT/ONS Some gifts and property are exempt from Inheritance Tax, such as some wedding gifts and charitable donations | GETTY

Some gifts and property are exempt from Inheritance Tax, such as some wedding gifts and charitable donations | GETTY

Fidelity’s calculations show that investing £3,000 annually for 18 years, totalling £54,000 in contributions, could potentially grow to approximately £112,000 by the child’s 18th birthday, assuming eight per cent yearly growth after fees.

Jemma Slingo, pensions and investment specialist at Fidelity International, shared: “For grandparents who are worried about inheritance tax but also want to make a meaningful difference to their grandchildren’s future, this can be a very effective combination.

“Using the £3,000 annual exemption to fund a Junior ISA allows families to gradually move money out of their estate while giving it the potential to grow tax-efficiently over the long term.”

She added: “It’s a practical example of how estate planning doesn’t have to be complicated. By making use of allowances that are already available each tax year, families can steadily build up a substantial pot for the next generation while also reducing the value of their estate for IHT purposes.”

Parents are being urged to take advantage of Junior ISA products

| GETTY

Upon turning 18, a JISA automatically transitions into an adult ISA, with the young person assuming complete control of the account.

Under a medium growth scenario of five per cent, an £80,000 pot at 18 could expand to nearly £130,000 by age 30.

With higher growth assumptions of eight per cent, the £112,000 accumulated at 18 could potentially reach £250,000 by the same age. For grandparents unable to commit to regular contributions, even a single £3,000 gift at birth can make a meaningful impact.

Fidelity’s projections indicate such a one-off investment could grow to over £6,000 under medium growth assumptions, or exceed £10,500 with higher growth, by the child’s 18th birthday.