①When asked how high crude oil prices would need to climb to make the probability of a recession exceed 50%, economists provided a range of answers from $90 per barrel to $200 per barrel, with an average of $138; ②In terms of the timeline, when asked how long high oil prices would need to persist to trigger a recession, their responses ranged from 4 weeks to 55 weeks, with an average duration of 14 weeks.

Cailian Press, March 20 (Editor: Xiaoxiang) Over the past few weeks, the war between the United States and Israel against Iran has caused record-breaking disruptions in oil supplies, sending crude oil and commodity prices into a ‘runaway’ mode.

This has also brought a ‘ultimate mystery’ to the forefront for market participants and economists: namely, how high must oil prices rise to trigger a global economic recession, especially in the world’s largest economy, the United States?

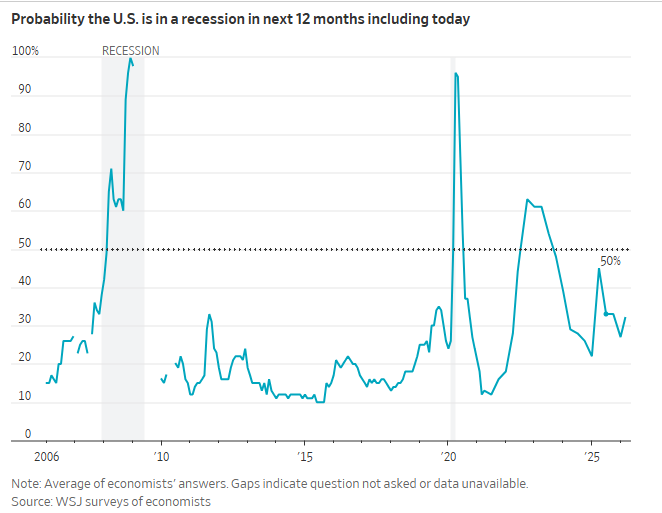

According to a survey conducted this week by media outlets, as the Middle East conflict enters its third week, the probability of a U.S. economic recession over the next 12 months is now estimated at 32%, slightly higher than the 27% forecast in January.

According to a survey conducted this week by media outlets, as the Middle East conflict enters its third week, the probability of a U.S. economic recession over the next 12 months is now estimated at 32%, slightly higher than the 27% forecast in January.

The survey collected responses from 50 economists representing organizations such as Wall Street banks, universities, and small consulting firms, and was conducted from March 16 to 18. Among the timely questions in this survey, two are particularly worth noting:

When asked how high crude oil prices would need to climb to make the probability of a recession exceed 50%, the economists’ responses ranged from $90 per barrel to $200 per barrel, with an average of $138.

In terms of the timeline, when asked how long high oil prices would need to persist to trigger a recession, their responses ranged from 4 weeks to 55 weeks, with an average duration of 14 weeks.

Evidently, against the backdrop of Brent crude oil prices briefly reaching $119 per barrel on Thursday, the average oil price threshold identified by these economists that could trigger a U.S. economic recession — $138 — does not seem too distant. What remains more suspenseful at present, perhaps, is the duration of such extreme high oil prices…

As introduced by Cailian Press earlier today, Saudi officials have provided a baseline forecast indicating that if supply disruptions persist until late April, oil prices could even soar above $180 per barrel.

Based on the timeline provided by Saudi officials, as extra pre-war inventories shipped out of the Gulf are depleted, physical shortages will become more severe next week, pushing prices toward $138 to $140 per barrel. By the second week of April, if supply disruptions are not alleviated and the Strait of Hormuz remains closed, oil prices may reach $150 per barrel, gradually rising to $165 and $180 in the following weeks.

Regardless, the upper limit of oil prices and their duration at high levels will likely depend on the length of the conflict in Iran. Prolonged hostilities will exacerbate economic shocks and further test investors’ resolve. Increasing analysis suggests that while the U.S. and global economies currently remain resilient, the scale and duration of energy disruptions will pose significant risks to economic growth, inflation, and central bank decision-making.

Where do Wall Street firms see the threshold for a U.S. economic recession?

$125

Robert Fry, an economist at Robert Fry Economics, currently believes there is a 40% probability of the U.S. economy falling into a recession. He stated that oil prices remaining at $125 for eight consecutive weeks would be the watershed event determining whether a recession occurs.

“My forecast is based on the premise that the Strait of Hormuz will be fully open to tanker traffic by mid-April,” he said. “If the strait remains closed beyond that point, oil prices will soar even higher, and I will incorporate a recession into my projections.”

$130

Analysts at Wells Fargo Securities wrote that if oil prices persist at $130 per barrel for several months, it would increase the risk of an economic recession, driving gasoline prices high enough to force Americans to cut spending, while businesses may need to ‘adjust staffing.’

$140

Economists at Oxford Economics warned that global oil prices averaging around $140 per barrel for two consecutive months, coupled with tightening financial conditions (such as rising interest rates), would be sufficient to push parts of the global economy into a ‘mild’ recession.

$150

Analysts at Vanguard Group are currently among the most optimistic. In a recent research report, the firm noted that for a U.S. economic recession to occur, oil prices would need to stabilize at $150 per barrel for the remainder of the year—higher than the historical peak of $147 per barrel reached in 2008. Other preconditions include rising interest rates and weakening asset prices.

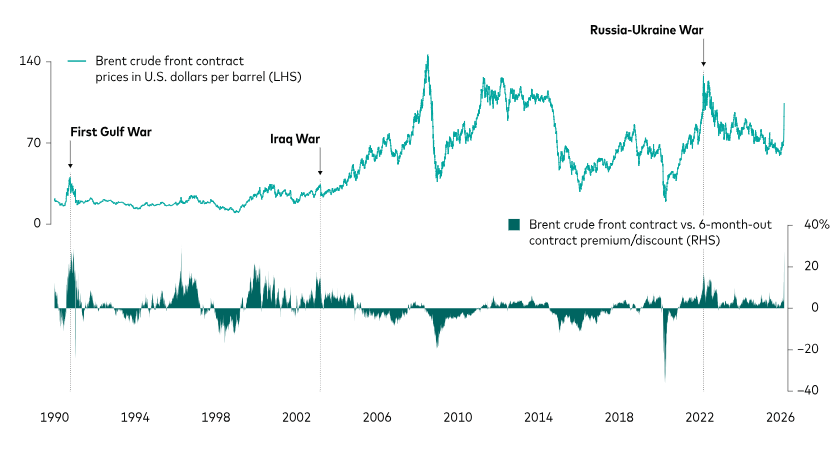

Fei Xu, Portfolio Manager of Vanguard Commodity Strategy Fund, pointed out that the surge in oil prices and market-based geopolitical risk premiums has rapidly approached levels seen during the First Gulf War in 1990 and the Russia-Ukraine conflict in 2022. At those times, oil prices and risk premiums skyrocketed and remained high for months until supply conditions stabilized and gradually receded.

If disruptions in crude oil and natural gas supplies and their associated uncertainties persist—similar to the situations in 1990 or 2022—the macroeconomic spillover effects will intensify ‘stagflation.’ Persistent energy price shocks could drive up inflation, tighten financial conditions, and complicate policy trade-offs.

Are other economies potentially more vulnerable than the United States?

Of course, considering that the U.S. has long become a net energy exporter, its threshold for enduring high oil prices may be significantly higher than that of other economies, especially countries reliant on energy imports…

Economists at California Lutheran University stated, ‘Since 2018, the United States has been the world’s largest oil producer… From an overall economic perspective, oil prices between $80 and $100 per barrel are not entirely negative for the U.S. In today’s dollar value, WTI crude oil prices once reached $200 per barrel in 2008.’

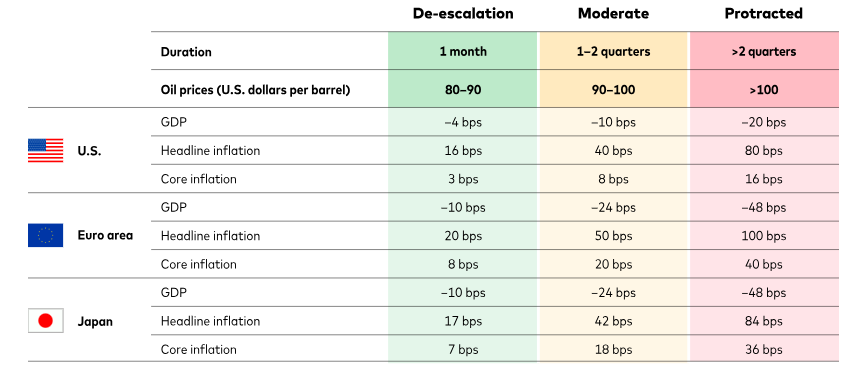

In Vanguard’s view, the cost of prolonged high oil prices may primarily affect non-U.S. economies such as the Eurozone and Japan. An analysis by the firm shows that if oil prices remain at $125 per barrel and natural gas prices stay at €150 per megawatt-hour until the end of the year, Eurozone real GDP could decline by one percentage point, pushing the economy into recession.

‘A sharp rise in energy prices could bring stagflationary shocks to the European economy,’ said Shane Retterath, Senior Economist at Vanguard Group.

(Compared with the United States, Europe and Japan are more vulnerable to the impact of prolonged high oil prices.)How could high oil prices trigger an economic recession?

(Compared with the United States, Europe and Japan are more vulnerable to the impact of prolonged high oil prices.)How could high oil prices trigger an economic recession?

Renowned economist and former PIMCO Chief Investment Officer Mohamed El-Erian pointed out that he believes the likelihood of the United States falling into a recession has now increased from about 25% to 35%. He stated that this increase is primarily driven by the spillover effects of the U.S.-Iran conflict, but he added that another factor is also influencing his outlook.

① Rising oil prices have led to a spiraling increase in inflation, causing a demand shock. The Middle East conflict has already pushed up oil prices, with Brent crude hovering around $100 per barrel for more than a week. El-Erian noted that rising oil prices could make inflation a structural issue for the U.S. economy, referring to the widespread use of oil across industries and broader supply chain disruptions caused by the war.

El-Erian elaborated on his pessimistic forecast, stating, ‘The first phase of the shock is high inflation, which will erode people’s purchasing power and increase costs for businesses. The second phase will be slower economic growth and rising unemployment.’ He then added that he considers this scenario to be the greatest risk facing the economy.

② The risk of a ‘financial accident’ is rising. El-Erian noted that intensifying inflation may interact with various ‘vulnerabilities’ in financial markets, such as the recent surge in redemption requests in private credit sectors, weak global demand for government bonds, and overvalued stock markets.

‘In the event of a significant financial accident, the financial environment would tighten, and people would lose access to credit. Ultimately, this would lead to a demand shock,’ he said.

El-Erian stated that as long as the war continues, the risk of an economic recession will keep escalating. He pointed out that if supply disruptions in the Middle East persist, oil prices might rise further, posing additional risks of stagflation.

Why is this round of oil price shocks potentially more severe?

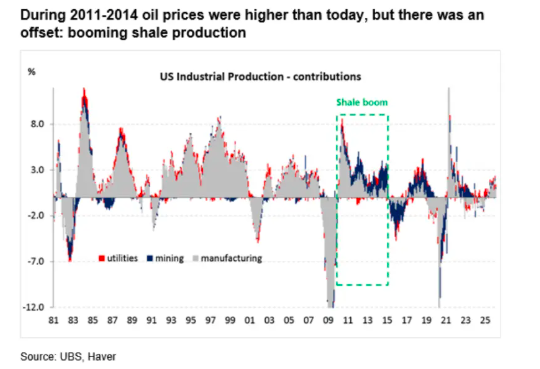

Arend Kapteyn, Head of Global Economic and Strategy Research and Chief Economist at UBS Group, highlighted in his latest research report that the current energy shock triggered by the Middle East conflict ‘differs from the period between 2011 and 2014.’ A key reason is that the U.S. shale industry is no longer capable of responding on a similar scale, meaning consumers are more likely to bear the brunt of the impact.

Kapteyn wrote that, after adjusting for inflation, oil prices during 2011-2014 were actually higher than they are now. However, the U.S. economy absorbed that shock at the time because the shale oil boom provided a boost to the industrial base. The surging WTI crude prices back then incentivized oil and gas companies to ramp up drilling activities, production growth, and investment in the energy sector. This created a tailwind for the U.S. manufacturing base and offset some of the drag caused by high fuel costs.

However, this is precisely where some arguments optimistic about the U.S. economy are beginning to appear less convincing. As Kapteyn noted, ‘The U.S. oil sector is currently far less responsive to price changes than it was a decade ago.’

Kapteyn noted that there are significant differences in the U.S. economy and oil industry compared to that period: today’s labor market is weaker, households face greater liquidity constraints, and inflationary pressures are sharper, reflecting a much faster pace of oil price increases (the year-over-year increase in oil prices between 2011-2014 never exceeded about 55%, whereas if current prices persist, the increase will approach 100%). However, the key difference—and the focal point here—is shale oil.

At the beginning of 2010, the U.S. mining sector (primarily the oil and gas industry) accounted for approximately 14% of industrial production. By 2012-2013, it contributed more than half of the total growth in U.S. industrial production, and there were even short periods when mining essentially drove all of the growth. Following the collapse of oil prices in 2015-2016, output in the U.S. mining sector mechanically rebounded from a low base, but shale oil did not return to the levels of investment or rig intensity seen prior to 2014. Oil production still responds at the margin to price changes, but the elasticity of investment has significantly diminished. In other words, if current oil prices are perceived as temporary, the U.S. is unlikely to witness any supply response akin to the shale-driven surge of 2011-2014 that could offset potential erosion of consumer net income.

UBS Group believes that the latest developments this week, including retaliatory attacks by Israel and Iran on upstream energy infrastructure in the Gulf region, as well as Qatar’s warning that an attack by Iran on its LNG complex could result in capacity being offline for months or even years, further reinforce the view that global energy markets are tightening further. The current risk lies in gasoline price shocks, which, if energy market volatility persists, may begin to weigh on market confidence in the coming weeks. Meanwhile, signs of stress have emerged in credit markets, further exacerbating concerns about a potential deterioration in the overall economic outlook.

Editor/Rocky